Definition & Meaning

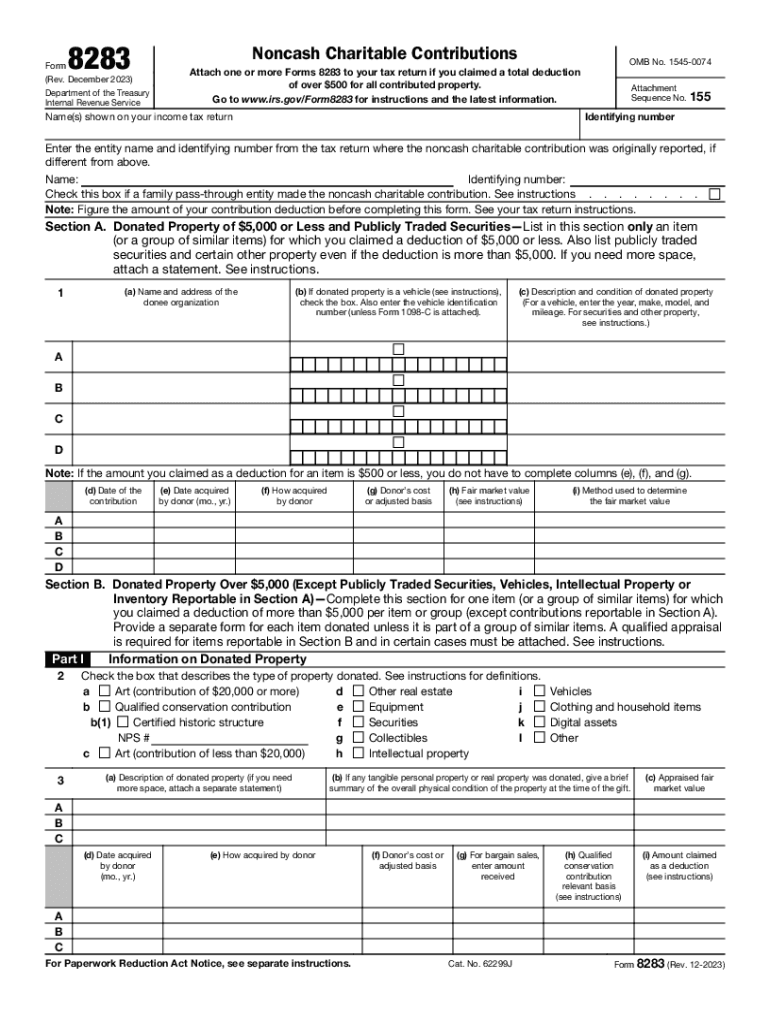

Form 8283 (Rev December 2023) Noncash Charitable Contributions, is a document utilized by U.S. taxpayers to report noncash charitable donations to claim tax deductions. Noncash donations can include goods such as clothing, furniture, or real estate. The form must be attached to a taxpayer's annual federal income tax return if noncash contributions exceed $500. It contains crucial sections for detailing the type and fair market value of the donated property, and it requires details from appraisers when the donation's value surpasses $5,000. This form not only facilitates the proper documentation needed for claiming deductions but also assists the IRS in maintaining the transparency of charitable contributions.

How to use the Form 8283 (Rev December 2023) Noncash Charitable Contributions

Using Form 8283 involves recording specific details about each donated item. Taxpayers need to provide descriptions, including the fair market value, acquisition date, and condition of the items. For donations with a value over $5,000, a qualified appraiser must assess the property, and their declaration should be included in the form. The purpose of this detailed information is to ensure accurate valuation and prevent discrepancies during the IRS review process. By appropriately documenting these donations, taxpayers can substantiate their claims, which is crucial in case of an audit.

Steps to complete the Form 8283 (Rev December 2023) Noncash Charitable Contributions

-

Fill in Part I: Enter the information regarding noncash contributions valued at $5,000 or less. Include the name of the charitable organization, details of the property, acquisition date, a brief description, and fair market value.

-

Complete Part II, if applicable: This section is for items valued over $5,000. It requires a qualified appraisal from a professional appraiser. Attach the appraisal to the form.

-

Provide Donor and Appraiser Declarations: The donor needs to affirm the credibility of the provided information, and the appraiser must assert the accuracy of the valuation.

-

File the Form with Tax Return: Form 8283 must accompany the federal tax return for the year in which the donations were made. Retain a copy for personal records.

-

Review for Accuracy: Ensure all sections are completed and that the attached documents are correct. Errors or omissions can delay the processing of returns.

Key elements of the Form 8283 (Rev December 2023) Noncash Charitable Contributions

- Part I: For items valued at $5,000 or less, includes basic information of the property and its fair market value.

- Part II: Dedicated to items exceeding $5,000 in value, requiring appraisals and extensive description.

- Donor and Appraiser Declarations: Both signatures are needed to fortify the document's authenticity.

- Attachments: Include appraisals and any additional documentation that supports the valuation.

IRS Guidelines

The IRS provides detailed guidelines for Form 8283 to ensure taxpayer compliance. Specific emphasis is placed on the accuracy of property descriptions and valuations. The form should reflect true market values to prevent tax fraud. These regulations also outline the required documentation, such as receipts and appraisals needed to substantiate claims. Understanding these guidelines helps prevent common errors and ensures that taxpayers remain compliant with federal tax laws.

Filing Deadlines / Important Dates

Form 8283 should be filed alongside the taxpayer's federal income tax return. The typical deadline for filing is April 15 of the year following the tax year; however, this can change if the date falls on a weekend or holiday. It's imperative to verify current deadlines with the IRS or a tax professional to avoid late filing penalties.

Required Documents

Taxpayers need several documents to support their Form 8283 submission:

- Receipts: From charitable organizations for each noncash donation.

- Qualified Appraisal: For items valued over $5,000.

- Photographs: Optional but recommended, especially for high-value items.

- Acquisition Documentation: Evidence of ownership and original purchase price.

Examples of using the Form 8283 (Rev December 2023) Noncash Charitable Contributions

- Example 1: An individual donates a used car to a qualifying charity and receives an appraisal indicating a fair market value of $6,500. The taxpayer completes Part II and attaches the appraisal.

- Example 2: A taxpayer donates household items to a thrift store with an estimated total value of $750. The taxpayer fills out Part I, providing item descriptions and values.

Taxpayer Scenarios

- Self-Employed Individuals: These taxpayers can claim deductions for donations that benefit community programs or resource centers.

- Retirees: They may donate personal items like antiques or collectibles.

- Students: Primarily contribute items such as books or clothing, which can collectively exceed $500.

Penalties for Non-Compliance

Failure to accurately complete and submit Form 8283 can result in various penalties, such as:

- Disallowance of Deductions: Incorrect or incomplete forms can lead to the rejection of claimed deductions.

- Fines: The IRS may levy fines for fraudulent claims.

- Audits: Non-compliance increases the likelihood of a tax audit, potentially leading to further scrutiny of the taxpayer’s finances.

Understanding these consequences emphasizes the importance of meticulous documentation and filing.