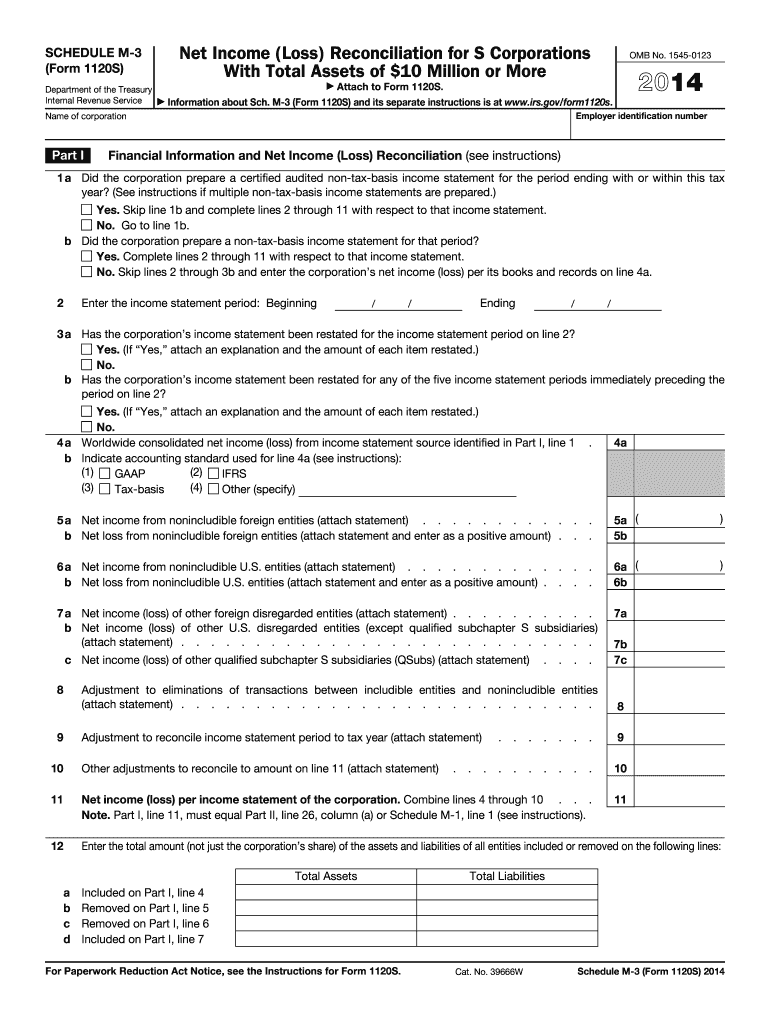

Definition and Purpose of the 2014 Form M-3

The 2014 Form M-3 is used by certain S corporations to reconcile financial statement net income with the income reported on their tax return. This reconciliation is crucial for ensuring that all income and expense items are appropriately categorized and reported to the Internal Revenue Service (IRS). The form plays a significant role in maintaining accuracy in tax filings for businesses with substantial assets.

The form consists of several parts, each dedicated to specific reconciliation tasks. It provides sections for financial information of U.S. and foreign entities, with adjustments to align the financial data with U.S. tax laws. Ensuring compliance with IRS regulations, the 2014 Form M-3 aids transparency and reduces discrepancies that could arise from differences between book and tax accounting methods.

How to Use the 2014 Form M-3

-

Gather Financial Documents: Before starting, collect all relevant financial statements and business records from the fiscal year. These documents will provide the necessary information to complete the form accurately.

-

Complete Part I: This section requires general financial information about the business, including balance sheet details. Ensure consistency with the company's consolidated financial statements for accuracy.

-

Address Income and Expense Reconciliation: Parts II and III delve into reconciling various income and expense items. Use these parts to adjust for differences between book and tax income, such as depreciation methods and interest deductions.

-

Foreign Adjustments: If applicable, account for adjustments related to income from international operations. These adjustments align foreign-based income and expense reporting with U.S. tax obligations.

-

Review and Correct Errors: Once filled, review the form thoroughly to identify and correct any discrepancies. Attention to detail is crucial to avoid penalties.

How to Obtain the 2014 Form M-3

To secure the 2014 Form M-3, businesses can download it directly from the IRS website. Ensure you have the appropriate software to view and fill PDF forms, as this form requires precision during completion. The IRS website provides instructions and additional resources to guide businesses through the document.

Alternatively, contact a tax professional who can provide the form and offer assistance in understanding the filing requirements. Tax professionals are especially useful for businesses that deal with complex financial structures or multinational income sources.

Steps to Complete the 2014 Form M-3

-

Start with Basic Identification: Enter the business name and Employer Identification Number (EIN) at the top of the document. Verify these details against official IRS records.

-

Analyze Financial Statements: Use financial statements for compiling book income figures. These should be consistent with audited financial statements if available.

-

Adjust Book Income: Make necessary adjustments between book income and tax income. Consider differences due to depreciation methods, tax credits, and charitable contributions.

-

Review Part III for U.S. Adjustments: Report any items specifically influenced by U.S. tax legislation, including domestic manufacturing incentives and Section 179 deductions.

-

Complete Foreign Reconciliations: For businesses with international dealings, fill in foreign adjustments under the designated sections.

-

Attach Additional Documentation: If required, attach supporting documents that justify your entries, such as depreciation schedules or foreign tax credit forms.

-

Finalize and Submit: Double-check completed fields for errors, sign the form where indicated, and append any necessary attachments before submission.

Who Typically Uses the 2014 Form M-3

The 2014 Form M-3 is primarily used by S corporations with total assets of $10 million or more, reflecting high financial activity and complexity. It serves businesses that require detailed income reconciliation due to differences in book and tax accounting.

Additionally, multinational corporations, or businesses with subsidiaries, often utilize this form to reconcile income derived from both foreign and domestic operations.

Important Terms Related to the 2014 Form M-3

- Net Income Reconciliation: The core purpose of the form, comparing net income figures from financial statements to those reported for tax purposes.

- Book-Tax Differences: Refers to disparities arising from different accounting methods for financial statements and tax purposes.

- Adjustment Items: Specific financial entries that need modification to align with tax legislation, such as depreciation or interest expenses.

- Foreign Income Adjustments: Reconciliations required to bring international earnings into compliance with U.S. tax law.

Key Elements of the 2014 Form M-3

- Part I: Financial Information and Reporting: Collects general financial data and context for adjustments.

- Part II: Reconciliation of Net Income (Loss): Aligns book income with tax income.

- Part III: Analysis of Income and Expense Items: Examines specific income and expense categories for accuracy.

These elements structure the reconciliation process, ensuring consistent and thorough tax filings.

IRS Guidelines for the 2014 Form M-3

The IRS guidelines for completing Form M-3 are comprehensive, reflecting the detail necessary for accurate reconciliation. The form must be filled precisely, adhering to prescribed methods for reporting income and expenses.

- Reconciling items should be backed by documentation.

- Updates or changes in tax laws should be considered during completion.

- Errors in execution can result in audits or penalties, underscoring the importance of compliance.

By following IRS guidelines, businesses ensure their financial reporting aligns with federal tax obligations.