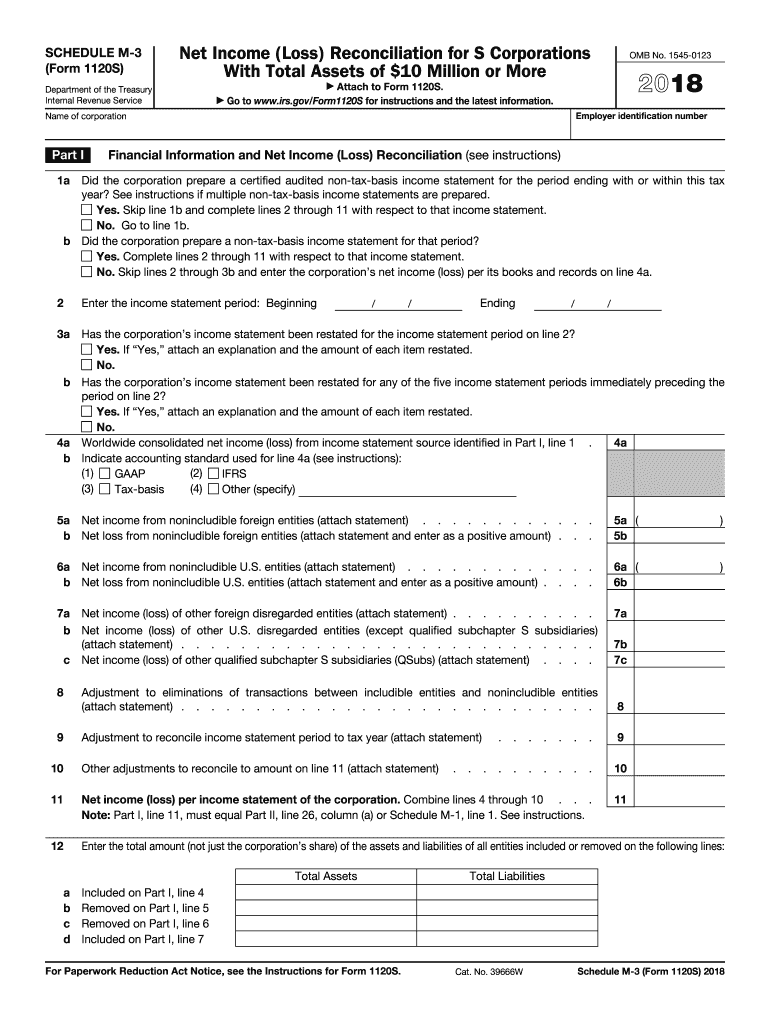

Definition and Purpose of Schedule M-3 (Form 1120)

Schedule M-3 (Form 1120) is specifically designed for S Corporations with total assets of $10 million or more. Its primary purpose is to reconcile the net income or loss reported in financial statements with the income or loss reported on federal tax returns. The form ensures compliance with IRS regulations by systematically detailing discrepancies between book and tax reporting. It includes sections dedicated to financial data, adjustments for foreign and U.S. entities, and reconciliation of various income and expense items.

How to Use Schedule M-3 (Form 1120)

To effectively use Schedule M-3, familiarize yourself with its layout and the specific details required. The schedule is divided into different parts that address various aspects of financial reconciliation:

- Part I: Financial Information and Net Income: This section requires you to input the financial statement net income and details about filing entities..

- Part II: Reconciliation of Net Income: This part focuses on differences between income or loss per financial statement and per tax return.

- Part III: Reconciliation of Expense Items: Here, you reconcile expense amounts reported in financial records with those on tax returns.

Ensure each part is completed accurately to avoid discrepancies and potential audits by the IRS.

Steps to Complete Schedule M-3 (Form 1120)

- Gather Necessary Documents: Collect all relevant financial statements and prior-year tax returns.

- Fill Out Financial Information: Begin with Part I, providing comprehensive financial statement details.

- Reconcile Income: In Part II, compare the net income from financial statements with tax return figures, noting disparities.

- Detail Expense Differences: Use Part III to explain differences in expense reporting.

- Review and Double-Check Entries: Ensure all figures are correct and supported by documentation.

- Submit with Form 1120S: Attach the completed Schedule M-3 with your 1120S return when filing.

Reasons to Use Schedule M-3 (Form 1120)

Schedule M-3 provides several significant advantages for taxpayers:

- Compliance: Ensures adherence to IRS regulations on financial and tax reporting discrepancies.

- Transparency: Offers a clear view of variances between book and tax income, aiding in accurate tax reporting.

- Audit Deterrence: A detailed reconciliation can minimize the chance of audits.

Who Typically Uses Schedule M-3 (Form 1120)

Schedule M-3 is generally utilized by S Corporations in the U.S. with:

- Total Assets Greater Than $10 Million: This threshold necessitates its completion and submission.

- Complex Financial Structures: Entities with varying income sources and international operations benefit from detailed reconciliation.

Key Elements of Schedule M-3 (Form 1120)

Key components within the form you need to address include:

- Part I: Financial information detailing entities' book income and total assets.

- Part II: Sections that reconcile book income with tax income, including special-mode calculations for tax-specific adjustments.

- Part III: Expense reconciliations, detailing differences and categorizing adjustments.

IRS Guidelines and Compliance Requirements

Adhere strictly to the IRS laydown requirements for preparation and submission:

- Annual Submission: Typically due at the same time as the Form 1120S filing.

- Accurate Representations: Ensure figures precisely reflect financial and tax statements.

- Supporting Documentation: Maintain thorough records in case of IRS inquiries.

Penalties for Non-Compliance

Failure to file or errors in reconciling can lead to penalties. It's critical to:

- Accurate Filing: Avoid mistakes by thoroughly reviewing financial inputs.

- Timely Submission: Meet deadlines to prevent late filing fees.

Inadequate compliance could result in audits, financial penalties, and legal scrutiny.