Definition & Purpose of Schedule M-3 (Form 1120S)

Schedule M-3 (Form 1120S) is a crucial tax form designed for S Corporations with total assets of $10 million or more. Its primary function is to reconcile the differences between the financial accounting net income or loss and the taxable income or loss reported on the tax return. By detailing these discrepancies, the form helps maintain transparency and accuracy in tax reporting for large corporations. The form includes various sections that require detailed reporting of income, expenses, and adjustments for both U.S. and foreign entities.

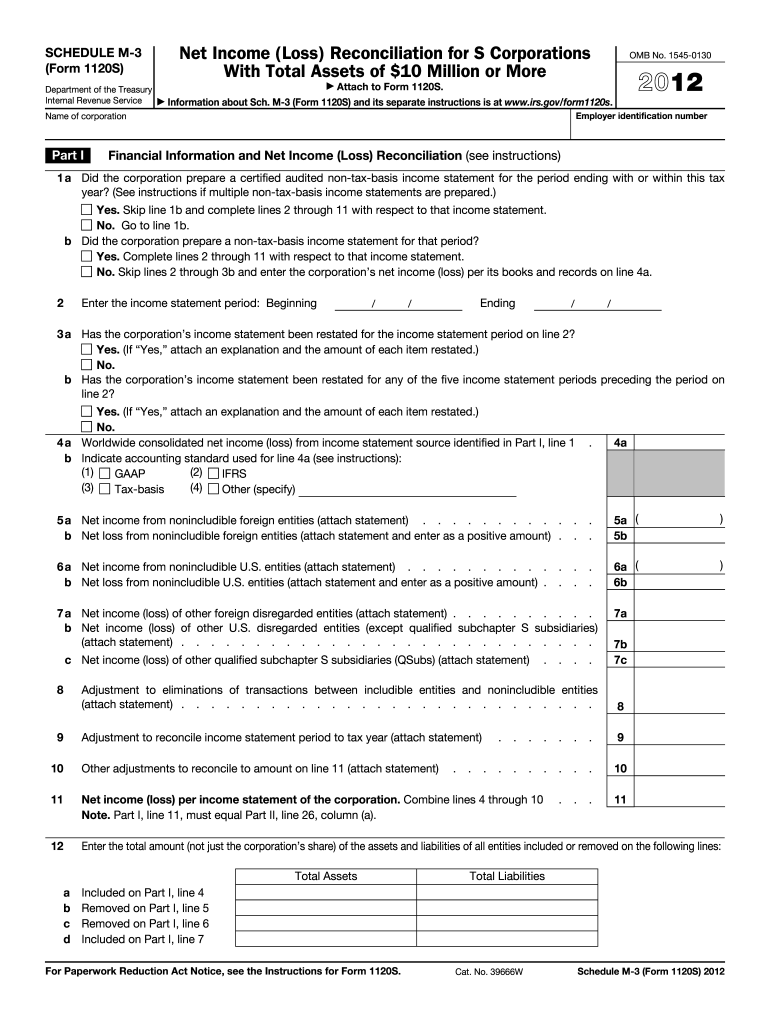

How to Use the 2012 Schedule M-3 (Form 1120S)

Using this form involves a detailed process of documenting and explaining financial discrepancies. S Corporations must:

- Gather accurate and comprehensive financial statements.

- Identify all differences between the book income and taxable income.

- Enter these discrepancies in the detailed sections that categorize various income and expense items.

- Provide explanations and supporting documentation for each adjustment, ensuring that they align with IRS requirements and standards.

It is critical to follow the instructions for each line item meticulously to avoid errors.

Steps to Complete the 2012 Schedule M-3 (Form 1120S)

Completing the Schedule M-3 (Form 1120S) requires meticulous attention to detail. Below is a step-by-step process:

- Collect Financial Data: Assemble all necessary financial statements, including the balance sheet, income statement, and cash flow statement.

- Analyze Income and Expenses: Break down revenues and expenditures into categories recognized by the IRS.

- Identify Adjustments: Pinpoint items that differ between book and tax accounting.

- Complete Part I: Provide company information and summarize financial data.

- Complete Part II: Detail income and expense items and describe any adjustments required.

- Complete Part III: Reconcile net income or loss with financial statements, providing thorough explanation and documentation for significant adjustments.

- Review for Accuracy: Verify all entries and calculations, ensuring document compliance and completeness before submission.

IRS Guidelines and Legal Use

The IRS outlines strict guidelines on the completion and submission of Schedule M-3 (Form 1120S). Corporations are required to accurately report discrepancies and provide sufficient documentation. Following these guidelines is essential to maintaining legal compliance and mitigating the risk of audits or penalties. The form must be filed alongside Form 1120S by the set deadlines, and any intentional misreporting can lead to significant legal consequences.

Key Elements of the 2012 Schedule M-3

The form is systematically divided into important sections that facilitate detailed reporting:

- Part I: Financial Information and Summary: Captures basic financial details and provides a summary.

- Part II: Reconciliation of Income (Loss): Allows for adjustments between book and tax income.

- Part III: Detailed Income and Expense Reconciliation: Requires a thorough reconciliation of specific items and tax positions.

Each section requires extensive documentation and precise calculations to ensure transparency and accuracy.

Filing Deadlines & Important Dates

S Corporations must adhere to specific filing deadlines for Schedule M-3 (Form 1120S). Generally, it is due by March 15th for calendar-year filers, along with Form 1120S. Extensions are available if requested by the due date, granting additional time to file—typically six months—but not to pay any due taxes.

Who Typically Uses the 2012 Schedule M-3 (Form 1120S)?

The 2012 Schedule M-3 is primarily utilized by large S Corporations with assets of $10 million or more. These corporations often experience complexities in reconciling their financial and tax reports due to numerous transactions and diverse operations potentially across multiple jurisdictions. This form allows them to clarify financial positions to the IRS, ensuring compliance and simplifying the audit process.

Penalties for Non-Compliance

Failure to comply with the requirements of Schedule M-3 (Form 1120S) can result in significant penalties. Underreporting or misreporting financial data may lead to fines, increased scrutiny, or audits by the IRS. Corporations are encouraged to seek professional assistance if needed to ensure all details are accurately reported, thereby avoiding potential legal ramifications. Regular audits and reviews of financial processes can further mitigate non-compliance risks.