Definition & Meaning

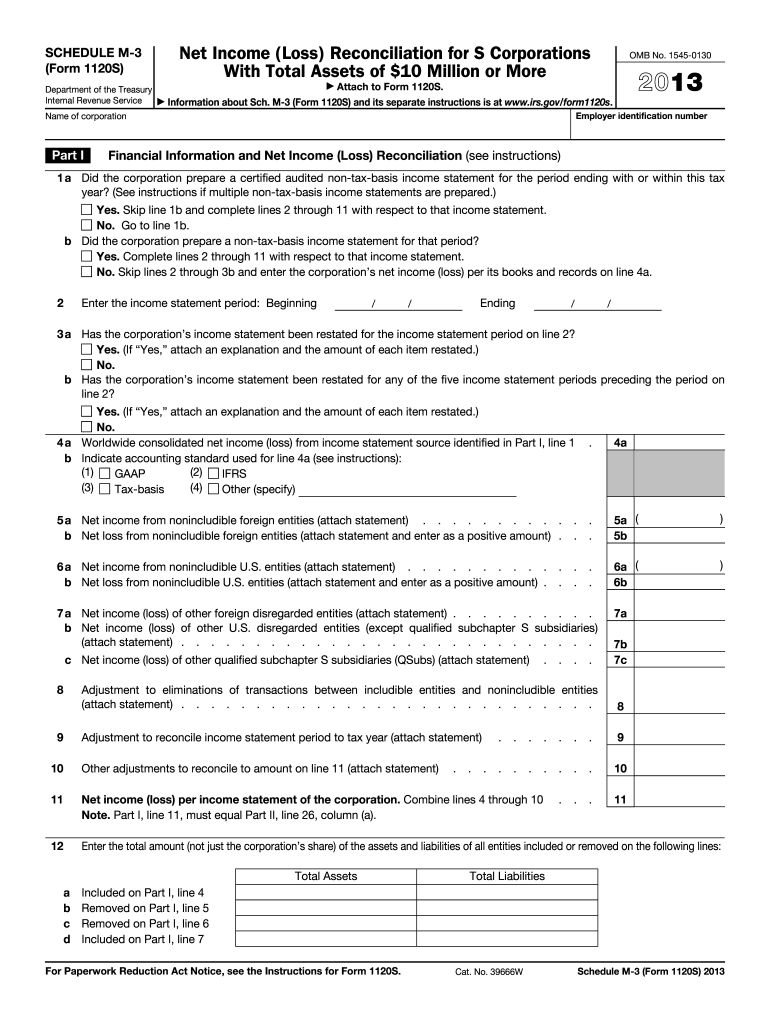

The 2013 Form 1120 S Schedule M-3 is a critical tax document for S Corporations with total assets of $10 million or more. It serves the purpose of reconciling net income (or loss) as reported in financial statements with the tax return figures. This form is designed to enhance transparency in financial reporting and ensure that discrepancies between book income and taxable income are explicitly addressed.

Key Elements of the 2013 Form 1120 S Schedule M-3

Understanding the main components of Schedule M-3 is crucial for proper completion and compliance:

- Part I: Contains financial information details about the S Corporation, including income statement information.

- Part II: Deals with reconciliation adjustments for different adjustments between book and tax, including temporary differences.

- Part III: Focuses on expense items, reconciling specific line items such as deductions claimed for federal tax purposes against what is reported on financial statements.

Steps to Complete the 2013 Form 1120 S Schedule M-3

- Gather Financial Statements: Collect the S Corporation's financial statements, ensuring all income and expenses are accurately recorded.

- Fill Part I - Financial Information: Begin by detailing general financial information, including summary lines from the company’s income statement.

- Complete Part II - Reconciliation of Net Income (Loss): Enter all reconciliation adjustments necessary to align financial accounting income with tax accounting principles.

- Fill Part III - Income and Expense Reconciliation: Provide detailed explanations for differences in expenses and income reported on financial statements versus tax returns.

Who Typically Uses the 2013 Form 1120 S Schedule M-3

The form is primarily used by large S Corporations based in the United States. These corporations are characterized by having assets of at least $10 million, requiring them to provide detailed reconciliations between financial statement income and tax return income for IRS scrutiny.

Filing Deadlines / Important Dates

- Regular Filing Deadline: The 2013 Form 1120 S Schedule M-3 must be filed along with the S Corporation's tax return, typically due March 15 following the end of the tax year.

- Extension Date: If an extension is filed, the deadline typically moves to September 15. Ensure timely submission to avoid penalties.

Required Documents

When preparing the Schedule M-3, gather the following documents:

- Income statement and balance sheet for the relevant fiscal year.

- Detailed records of all financial transactions, including supporting documentation that substantiates any discrepancies between book and tax figures.

IRS Guidelines

According to the IRS guidelines, the Schedule M-3 provides a detailed framework for disclosure of book-tax differences. Corporations are required to identify and explain significant items that lead to these differences, ensuring accuracy and consistency in tax reporting.

Penalties for Non-Compliance

Failure to accurately file the 2013 Form 1120 S Schedule M-3 can result in substantial penalties:

- Monetary Fines: These may be imposed for inaccurate reporting or failure to file.

- Increased Scrutiny: Can lead to audits and additional oversight by IRS officials.

- Delay in Tax Return Processing: Non-compliance may result in delayed processing and subsequent penalties for late payments.

Digital vs. Paper Version

The 2013 Form 1120 S Schedule M-3 can be completed digitally or on paper:

- Digital Filing: Allows for easier submission and faster IRS processing, often through commercial tax preparation software that complies with IRS e-file specifications.

- Paper Filing: Requires manual entry and postal submission, potentially leading to longer processing times and higher chances of human error.