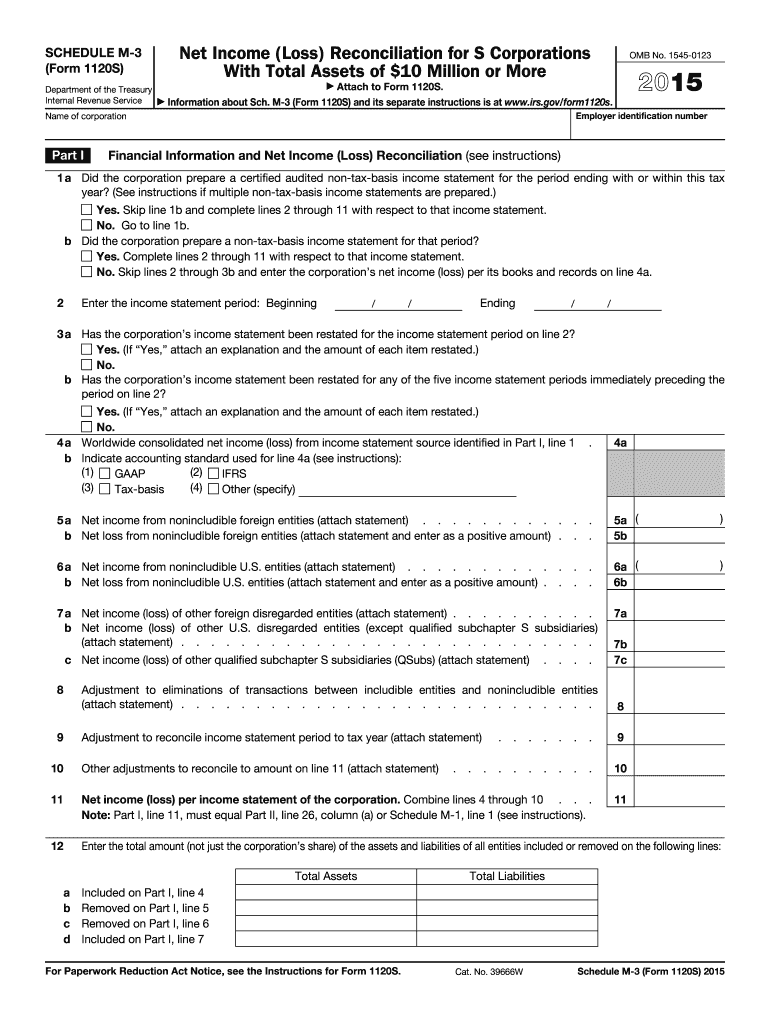

Definition and Meaning of 2015 Form M-3

The 2015 Form M-3, specifically Schedule M-3 (Form 1120S), is a tax form used by S corporations to reconcile their financial statement net income (loss) with the income (loss) reported on U.S. tax returns. This reconciliation ensures compliance with Internal Revenue Service (IRS) requirements. The form is essential for corporations with total assets of $10 million or more, requiring detailed disclosures about income, expense adjustments, and other financial data.

How to Use the 2015 Form M-3

To properly use the 2015 Form M-3, S corporations must follow several steps:

- Gather Financial Statements: Collect comprehensive financial statements for the tax year, including profit and loss statements and balance sheets.

- Identify Discrepancies: Review these financial documents to identify discrepancies between book income and tax income.

- Complete Sections: Fill out each section, detailing adjustments for differences, such as depreciation and expense allocations.

- Reconcile Entries: Ensure all income and deduction items are reconciled as required by the form's instructions.

- Review Compliance: Ensure the form is complete and compliant with IRS regulations before submission.

Steps to Complete the 2015 Form M-3

Completing the 2015 Form M-3 involves several stages:

- Part I - Financial Information: Provide basic financial details, including book income and total assets.

- Part II - Reconciliation of Income (Loss): Detail each difference between financial books and tax reporting under various adjustment categories.

- Part III - Expense Reconciliation: Record expenses reported in financial statements and reconcile them with tax deductions.

- Attach Necessary Documents: Include relevant schedules and worksheets that support the entries on the form.

- Cross-verify for Accuracy: Double-check all figures and entries for precision and agreement with the corporation's general ledger.

Who Typically Uses the 2015 Form M-3

The 2015 Form M-3 is typically used by:

- S Corporations: Specifically those with assets of $10 million or more.

- Tax Professionals: CPAs and tax advisors who manage the books of eligible S corporations.

- Corporate Financial Officers: Individuals responsible for ensuring accurate financial reporting and compliance.

Key Elements of the 2015 Form M-3

Important components of the form include:

- Book Consistency: Maintaining and reporting consistent financial records.

- Tax-to-Book Adjustments: Accurately reflecting adjustments necessary for reconciling book and tax figures.

- Disclosures of Foreign and Domestic Details: Including disclosures necessary for compliance with international business transactions.

IRS Guidelines for the 2015 Form M-3

The IRS provides specific guidelines, including:

- Filing Requirements: Eligibility based on asset thresholds and corporation type.

- Instructions for Completing Sections: Detailed instructions for accurately filling out each part of the form.

- Compliance: Adhering to IRS publication standards to avoid misreporting or audit issues.

Penalties for Non-Compliance

Non-compliance with the 2015 Form M-3 can result in:

- Fines and Penalties: Monetary penalties for failure to file or inaccuracies.

- Audit Risks: Increased likelihood of an audit due to insufficient or incorrect reporting.

- Legal Repercussions: Potential legal challenges if discrepancies lead to significant underreporting of tax liabilities.

Software Compatibility

S corporations can use various software to aid in filing the 2015 Form M-3 efficiently:

- TurboTax and QuickBooks: Supports the completion and e-filing of tax forms, including M-3.

- Accounting Software: Enables extract and reconciliation of financial data necessary for the form.

- Electronic Filing Options: Facilitate direct IRS submission to streamline the filing process.