Definition & Purpose of Form 1042-T Instructions

Form 1042-T is primarily used by withholding agents to transmit paper copies of Forms 1042-S to the IRS. These forms report U.S. source income paid to foreign persons and are subject to withholding. Understanding the instructions for this form is crucial for compliance and accurate reporting of withheld taxes. The form provides guidelines on filing requirements and necessary documentation, ensuring that foreign income is appropriately reported and taxed according to U.S. laws.

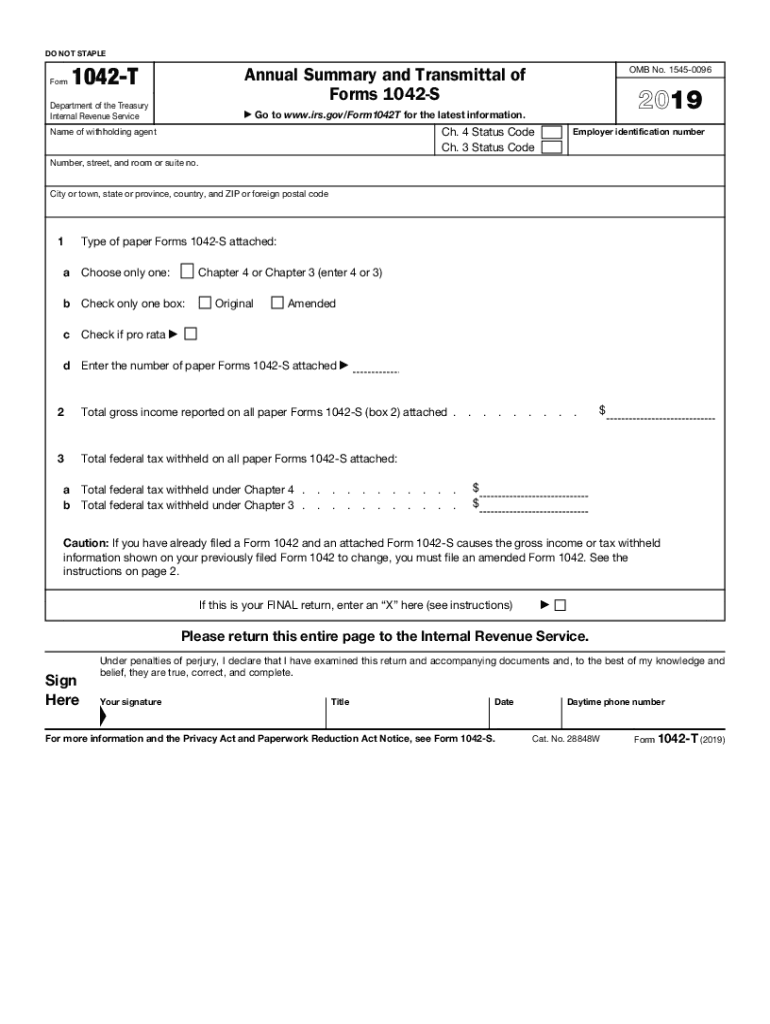

Steps to Complete Form 1042-T

-

Gather Required Information:

- Collect all relevant details from Forms 1042-S, including details about the withholding agent and recipient.

- Ensure all taxpayer identification numbers are correct and that amounts are properly calculated.

-

Complete Part I - Identification:

- Fill in the withholding agent’s name, address, and EIN.

- Provide information about the number of Forms 1042-S attached.

-

Complete Part II - Transmittal:

- Include the total amount of federal tax withheld as reported on Forms 1042-S.

-

Verify for Accuracy:

- Check all entries for accuracy and confirm that figures match those on the Forms 1042-S attached.

-

Submission:

- Mail the completed Form 1042-T along with original Forms 1042-S to the specified IRS address.

Who Typically Uses the Form 1042-T Instructions

Withholding agents, such as banks, financial institutions, or any entity that makes payments of U.S. source income to foreign persons, are the primary users. These instructions ensure proper completion and submission of tax information to the IRS. The form is particularly relevant for those who distribute income sourced within the U.S., ensuring taxes are withheld and reported appropriately.

Important Terms Related to Form 1042-T

- Withholding Agent: Any person or entity responsible for withholding and reporting U.S. source income paid to a foreign individual or corporation.

- Recipient: The foreign person or corporation receiving U.S. source income, subject to withholding tax.

- 1042-S: A form used to report income and withholding instances to the IRS and the recipient when U.S. source income is paid to a foreign entity.

Legal Use of Form 1042-T

Form 1042-T serves as a legal document for accountability and compliance with IRS regulations. It ensures that withholding agents report taxes accurately and maintain transparency regarding the distribution of U.S. source income. Misuse or failure to file can result in significant penalties, emphasizing the need for adherence to the instructions.

Filing Deadlines and Important Dates

The form must be filed annually, with the deadline being March 16, 2020, for the tax year 2019. This date may vary slightly from year to year, especially if it falls on a weekend or public holiday. It is critical to adhere to this deadline to avoid penalties.

Required Documents for Filing

- Forms 1042-S: Each form details specific transactions regarding U.S. source incomes paid and tax withheld.

- Withholding Agent Identification: Documentation that verifies the withholding agent's identity and tax information.

Examples of Using Form 1042-T Instructions

For instance, a bank distributing interest to a foreign investor would utilize the 1042-T instructions to ensure that the appropriate forms are completed and correctly submitted to the IRS. Similarly, multinational corporations distributing dividends to foreign shareholders must provide detailed and accurate income and withholding information. Proper use of these instructions helps avoid compliance issues and potential penalties.

IRS Guidelines for Form 1042-T

- The IRS provides specific instructions for the preparation and submission of Form 1042-T.

- Foreign income transactions must be reported accurately to reflect proper withholding.

- Adherence to detailed IRS guidelines ensures the avoidance of legal complications or penalties associated with non-compliance.

Penalties for Non-Compliance

Failure to file Form 1042-T accurately and on time can result in significant penalties. The IRS may impose fines on withholding agents who fail to report or underreport income. These penalties underscore the importance of comprehending the form's instructions and ensuring precise adherence to submission requirements.

Submission Methods (Mail/Online)

Currently, Form 1042-T must be submitted via mail along with physical copies of 1042-S forms. The IRS provides addresses for submission depending on agent location and nature of filing. Understanding various aspects of submission methods helps ensure correct and timely delivery to appropriate IRS offices.