Definition & Meaning

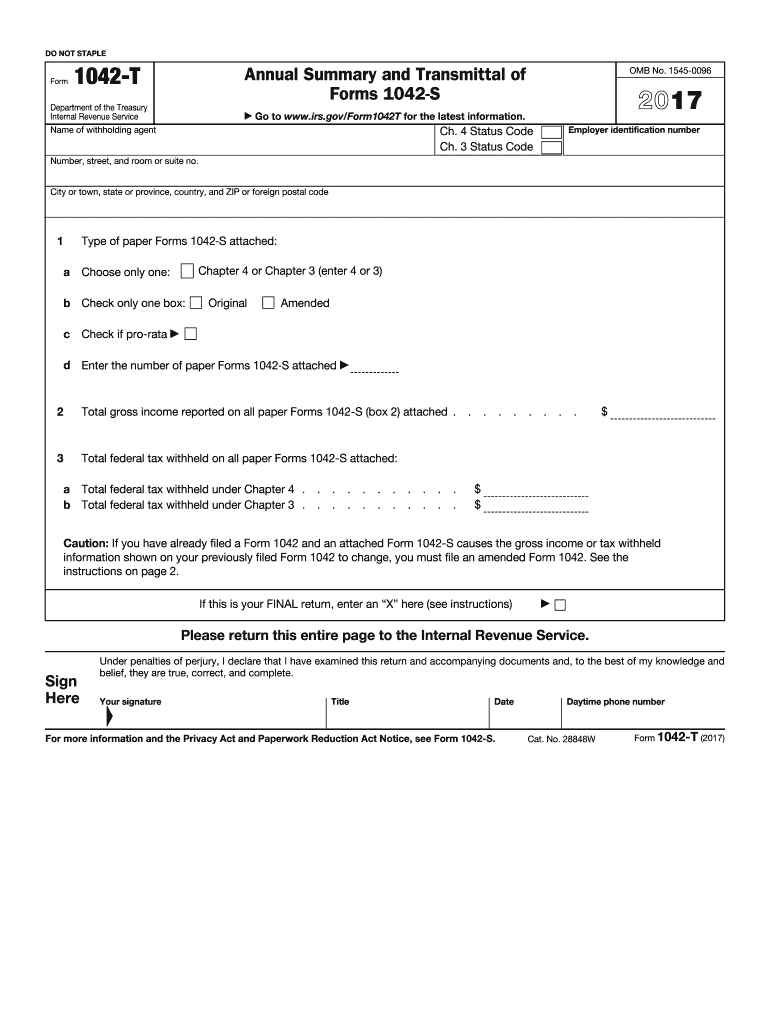

The 2017 Form 1042-T Annual Summary and Transmittal of Forms 1042-S is a critical document used by withholding agents in the United States to transmit paper Forms 1042-S to the Internal Revenue Service (IRS). These forms report income paid to foreign persons (including non-resident aliens) that is subject to income tax withholding. The Form 1042-T serves as a summary of all the Forms 1042-S submitted for the year and ensures accurate reporting of the total gross income and tax withheld.

How to Use the 2017 Form 1042-T

When utilizing the 2017 Form 1042-T, withholding agents must compile all Forms 1042-S issued for the year. This summary form acts as a cover sheet for the submission of the paper forms to the IRS. The process involves collecting each Form 1042-S, completing the 1042-T with the total amount of income, and federal tax withheld as indicated on the individual reports. The form is then sent with the Forms 1042-S to ensure they are correctly processed by the IRS.

Steps to Complete the 2017 Form 1042-T

-

Collect Required Information:

- Aggregate all Forms 1042-S for the reporting year.

- Determine total gross income and federal tax withheld.

-

Fill Out Form 1042-T Sections:

- Complete identifying information for the withholding agent, including name, address, and EIN.

- Input totals from the individual Forms 1042-S.

-

Submission:

- Attach the completed 1042-T to the top of the stack of Forms 1042-S.

- Submit the package to the IRS by the specified deadline.

-

Verification and Record Keeping:

- Double-check totals and information for accuracy.

- Keep copies of all submitted forms for your records.

Filing Deadlines / Important Dates

The deadline for submitting the 2017 Form 1042-T, along with its accompanying Forms 1042-S, is March 15, 2018. It is crucial for withholding agents to adhere to this deadline to avoid potential penalties. The timely submission ensures compliance with IRS requirements and facilitates the accurate processing of tax withholdings.

Legal Use of the 2017 Form 1042-T

The legal framework surrounding the 2017 Form 1042-T entails compliance with US tax regulations for withholding on income paid to foreign persons. The form's primary legal use involves summarizing annual tax data that impacts both the US and foreign jurisdictions. By accurately completing and submitting the form, withholding agents meet their legal obligations to report income and tax withholding for non-resident tax situations.

IRS Guidelines

The IRS provides specific instructions on completing the Form 1042-T to guide withholding agents. These guidelines include identifying the withholding agent, ensuring accuracy in summary totals, and clarifying submission requirements. Additionally, the IRS outlines procedures for electronically filing when the number of forms exceeds the paper submission threshold, although electronic submission requires different forms.

Penalties for Non-Compliance

Failure to file the Form 1042-T, or submitting it inaccurately or late, can result in penalties levied by the IRS. These can include fines based on the severity and duration of non-compliance. Errors in reported amounts or missing deadlines can incur additional costs, reinforcing the importance of precision and prompt filing.

Software Compatibility

Tax preparation software like TurboTax and QuickBooks can assist in managing the data necessary for the Form 1042-T, although submission of the form itself often requires checking compatibility with specific electronic filing systems. The form may need to be printed and mailed, depending on IRS specifications and the software used to compile and prepare the information.

Required Documents

Submission of the 2017 Form 1042-T requires the following documents:

- Completed Form 1042-T

- All associated Forms 1042-S for the tax year

- Withholding agent's identification such as name, address, and EIN

Ensuring all these documents are properly prepared prevents errors in submission and helps demonstrate due diligence in meeting federal withholding requirements.

Business Entity Types

The 2017 Form 1042-T is pertinent to a variety of business entities engaging in transactions that involve foreign payees. These entities can include corporations, partnerships, and limited liability companies that manage international financial dealings and require routine tax reporting of withholdings from payments made abroad.