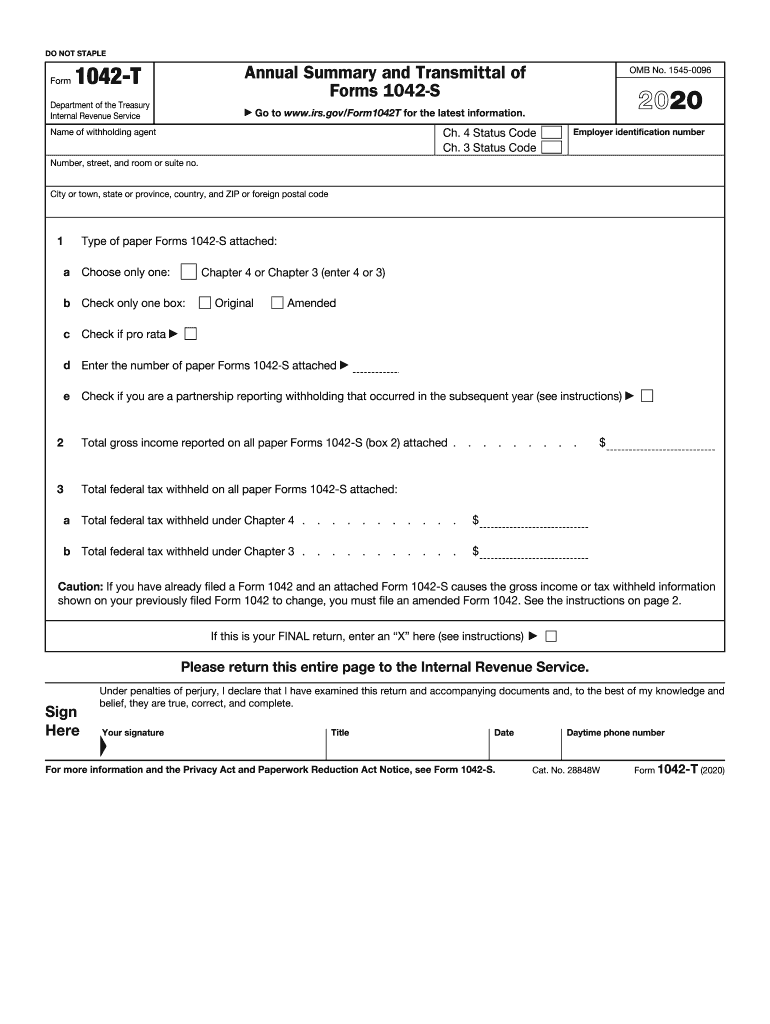

Definition and Purpose of Form 1042-T

Form 1042-T serves as a transmittal document for Forms 1042-S, which report income paid to non-resident aliens and foreign entities subject to withholding under U.S. tax laws. It is used specifically to transmit paper Forms 1042-S to the IRS. The need for accurate reporting through Form 1042-T ensures that withholding agents comply with federal tax regulations by consolidating the information relayed from multiple Forms 1042-S.

Features of Form 1042-T

- Consolidation: Compiles multiple 1042-S forms into a single submission.

- Tax Year Relevance: Used for a specific tax year, such as 2020, aligning with filing requirements.

- Information Transmission: Facilitates data aggregation for IRS processing purposes.

Steps to Complete Form 1042-T

Filing Form 1042-T involves several key steps to ensure compliance and accuracy.

- Gather Necessary Forms 1042-S: Ensure all relevant Forms 1042-S are completed and available for submission.

- Complete the Identification Section: Provide information such as the Withholding Agent’s name, address, and TIN.

- Aggregate Information: Calculate the total number of Forms 1042-S and the total income and withholding reported.

- Submit Original Copies: Ensure that all Forms 1042-S submitted with the 1042-T are original copies.

- Mailing: Complete and mail the form to the IRS by the due date to avoid penalties.

Common Mistakes to Avoid

- Inaccurate Totals: Verify that totals on Form 1042-T align with those on the attached Forms 1042-S.

- Missing Information: Double-check all entries for completeness to prevent issues with IRS processing.

Filing Deadlines and Important Dates

The deadline for filing Form 1042-T is generally March 15 of the year following the tax year in question. Meeting this deadline is crucial to adhere to IRS guidelines.

Key Dates

- Filing Deadline: March 15

- Amendment Period: Generally, amendments can be made shortly after the filing deadline, but it is always best to consult current IRS guidelines for specific dates.

Who Typically Uses Form 1042-T

Form 1042-T is typically used by withholding agents including corporations, partnerships, estates, and trusts within the U.S., tasked with managing income payments to foreign persons and entities.

Scenarios and Examples

- Corporations: Often act as withholding agents for dividends paid to foreign investors.

- Partnerships: Handle distributions to foreign partners needing withholding.

Legal Use of Form 1042-T

Complying legally with Form 1042-T requirements involves adhering to IRS regulations on withholding and income reporting for foreign beneficiaries.

Compliance Elements

- Accurate Withholding: Ensure withholding aligns with applicable treaties and U.S. laws.

- Timely Filing: Adhere strictly to the filing deadlines to avoid penalties.

Key Elements of Form 1042-T

Understanding the core components of Form 1042-T is essential for proper filing:

- Identification Information: Includes basic data about the filer such as name and TIN.

- Total Number of Forms 1042-S: Count of submitted 1042-S forms.

- Income and Withholding Totals: Aggregated financial information from the accompanying Forms 1042-S.

Detailed Field Explanation

- Section 1: Basic filer data must be clear to prevent processing delays.

- Section 2: Proper enumeration and summation of linked documents are crucial.

IRS Guidelines for Form 1042-T

Adhering to IRS guidelines reduces the risks associated with incorrect filing.

Key IRS Instructions

- Electronic vs. Paper Filings: Understand which methods are permissible and how to transition between them.

- Corrective Procedures: Follow proper protocols for correcting errors or amendments.

Penalties for Non-Compliance

Failure to comply with Form 1042-T requirements can lead to IRS-imposed penalties.

Common Penalties

- Failure to File: Incur penalties for missed deadlines.

- Inaccurate Filings: Correct any errors promptly to minimize financial and legal consequences.

Mitigation Strategies

- Timely Amendments: Rectify inaccuracies as soon as possible following recognition.

- Proactive Communication: Engage actively with the IRS to clarify and resolve any discrepancies.

By covering these details, users can maintain compliance with IRS standards and ensure accurate tax reporting on foreign income transactions.