Definition & Meaning

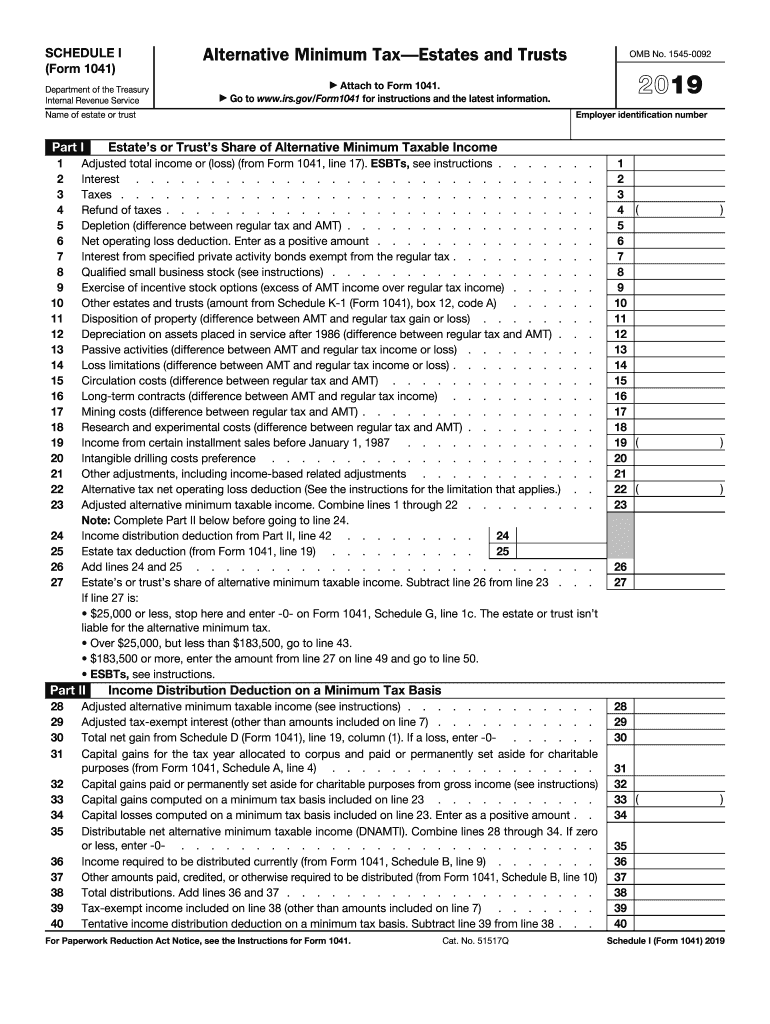

Schedule I (Form 1041) specifically pertains to the Alternative Minimum Tax (AMT) for estates and trusts. It serves to report and calculate a trust's or estate's share of alternative minimum taxable income. Various adjustments, preferences, and deductions outlined on this form play crucial roles in determining an estate's or trust's AMT liability. Understanding the form's purpose is essential for proper tax reporting for estates and trusts.

Who Typically Uses the Tax Form Schedule I

The primary users of Schedule I (Form 1041) are fiduciaries of estates and trusts subject to the Alternative Minimum Tax. These include executors, administrators, and trustees who manage the financial and tax affairs on behalf of the deceased or beneficiaries. Such fiduciaries ensure compliance with tax obligations related to AMT calculations.

Key Elements of the Tax Form Schedule I

The form encompasses several key elements, including:

- Adjustments and Preferences: Lists necessary adjustments to regular taxable income to determine AMTI.

- Exemption Amount: Specifies exemptions applicable to estates and trusts.

- Tax Liability Calculation: Instructions for calculating AMT liability after making requisite adjustments.

Each component must be thoroughly understood and completed to ensure accurate tax reporting.

Steps to Complete the Tax Form Schedule I

- Gather Essential Documents: Collect all relevant financial statements and prior tax returns.

- Determine Regular Taxable Income: Begin with the estate's or trust's previously calculated taxable income.

- Apply Adjustments and Preferences: Follow IRS instructions for adjusting taxable income.

- Calculate AMT: Use the adjusted income to determine AMTI and apply the corresponding AMT rates.

- Complete the Form: Fill out Schedule I using the calculated figures.

This methodical process ensures precise completion and compliance with AMT requirements.

IRS Guidelines

The IRS provides comprehensive guidelines on completing Schedule I. This includes specific instructions on identifying applicable adjustments, calculating exemptions, and applying tax rates. Fiduciaries must closely adhere to these directions to avoid discrepancies and ensure accurate tax filings.

Filing Deadlines / Important Dates

For estates and trusts, both Form 1041 and Schedule I must typically be filed by the 15th day of the fourth month following the end of the tax year. Ensuring timely submission is crucial to avoid IRS penalties or interest charges. Extensions may be requested if additional time is needed to gather information.

Required Documents

Fiduciaries must prepare several documents when filing Schedule I:

- Prior year's Form 1041

- Records of income and expenses for the estate or trust

- Documented adjustments and preferences

- Calculation sheets for AMT

These documents provide the foundation for accurately determining AMTI.

Penalties for Non-Compliance

Failing to file Schedule I when required can result in significant penalties from the IRS. These penalties may include fines, interest on unpaid taxes, and other legal ramifications. Ensuring timely and accurate submission is essential to avoiding such consequences.