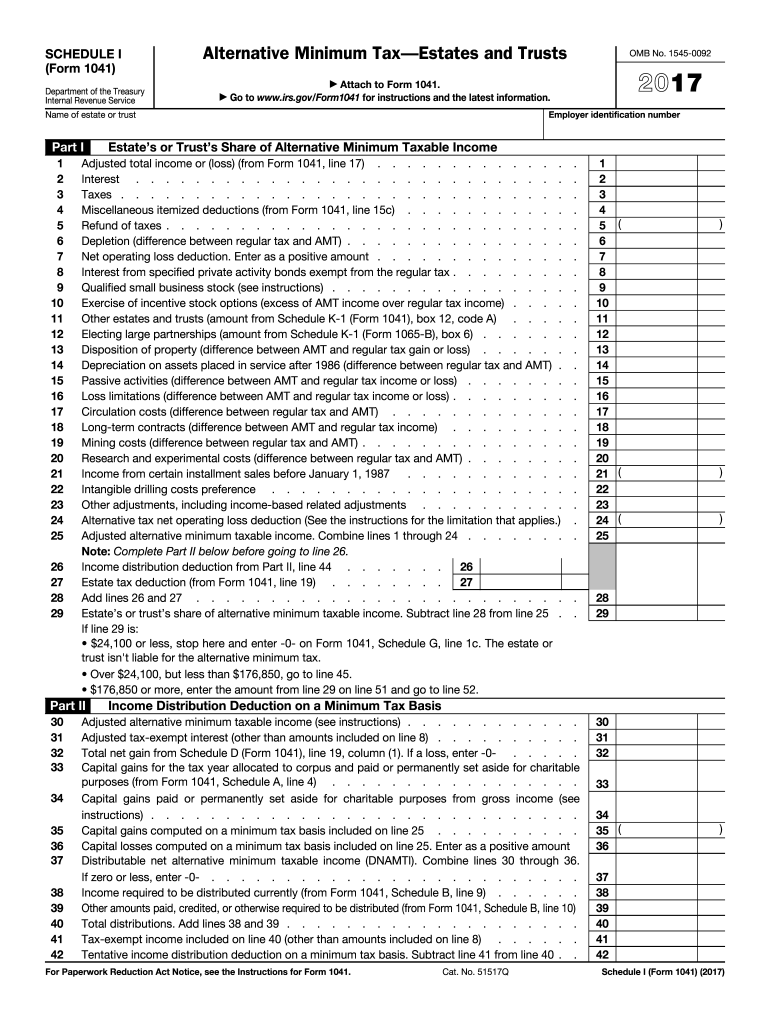

Definition & Meaning

The "1041 i form 2017" refers to Schedule I of Form 1041, which is used by the IRS for reporting the Alternative Minimum Tax (AMT) for estates and trusts. This form is crucial for calculating alternative minimum taxable income (AMTI), determining income distribution deductions, and assessing tax liabilities associated with the AMT. The 2017 version of this form pertains to tax obligations for that specific year, addressing changes in tax law applicable during that period.

How to Use the 1041 i Form 2017

To effectively use the 1041 i form 2017, one must first gather all relevant financial information regarding income and deductions for the estate or trust. This involves accurately reporting data across various sections of the form that focus on computing the AMTI and calculating any exemptions or adjustments required. The use of precise numbers and thorough understanding of the tax code is essential for minimizing errors and ensuring compliance.

Steps for Completion

- Gather Required Documents: Collect all financial records, including income statements, tax deductions, and previous tax returns.

- Compute AMTI: Fill out the sections calculating alternative minimum taxable income, considering adjustments and preferences.

- Evaluate Deductions and Credits: Detail any deductions and income distribution amounts that impact the AMT calculation.

- Complete the Tax Calculation: Use the form to compute total AMT liability by applying the appropriate IRS rates and guidelines.

- Review and File: Double-check all entries for accuracy before submitting either electronically or via mail.

Filing Deadlines / Important Dates

The filing deadline for the 1041 i form 2017 aligns with the standard tax filing deadlines. Generally, this means it was due on April 15, 2018, unless specific extensions were requested and granted. It is crucial for estates and trusts to adhere to these deadlines to avoid penalties.

Important Terms Related to 1041 i Form 2017

- Alternative Minimum Tax (AMT): A parallel tax system ensuring that entities pay at least a minimum amount of tax by eliminating certain deductions.

- Income Distribution Deduction: Deduction afforded to estates and trusts for income distributed to beneficiaries, directly impacting AMT calculations.

- Tax Preferences: Special tax treatment or exclusion items that could alter taxable income under AMT rules.

IRS Guidelines

The Internal Revenue Service provides comprehensive guidelines for filling out the 1041 i form 2017. These guidelines include instructions on computing AMTI, identifying eligible deductions, and clarifying reporting requirements for complex income scenarios. Adhering to these instructions is pivotal to ensure full compliance.

Penalties for Non-Compliance

Failing to submit the 1041 i form 2017 correctly or missing the filing deadline may result in penalties. These penalties can include fines based on the tax liability or income associated with the underreported or incorrectly reported amounts. Non-compliance can also trigger audits, leading to further scrutiny and potential interest charges on unpaid taxes.

Required Documents

- Income Statements: Documentation of all income received by the estate or trust, including dividends, interest, and capital gains.

- Deduction Records: Detailed records of all applicable deductions, including distributions to beneficiaries and related expenses.

- Prior Tax Returns: Previous years' tax returns may provide reference points for depreciation, losses carried forward, and other deductions.

Examples of Using the 1041 i Form 2017

Estate Example

An estate with significant capital gains and qualified dividends might use the 1041 i form 2017 to adjust its AMTI. By itemizing income and applicable deductions carefully, the estate can determine its AMT obligation and ensure compliance.

Trust Scenario

A family trust distributing income to multiple beneficiaries will require the 1041 i form 2017 to calculate income deductions efficiently. Proper use of the form ensures each beneficiary's share is calculated accurately, minimizing tax liability under the AMT framework.

Who Typically Uses the 1041 i Form 2017

Estates and trusts that meet the threshold for AMT are required to file the 1041 i form 2017. Specifically, this pertains to fiduciaries who manage these entities and are responsible for reporting taxable income distributions and ensuring all tax liabilities are met per IRS guidelines for the 2017 tax year.