Definition & Meaning of the 2016 Estates Form

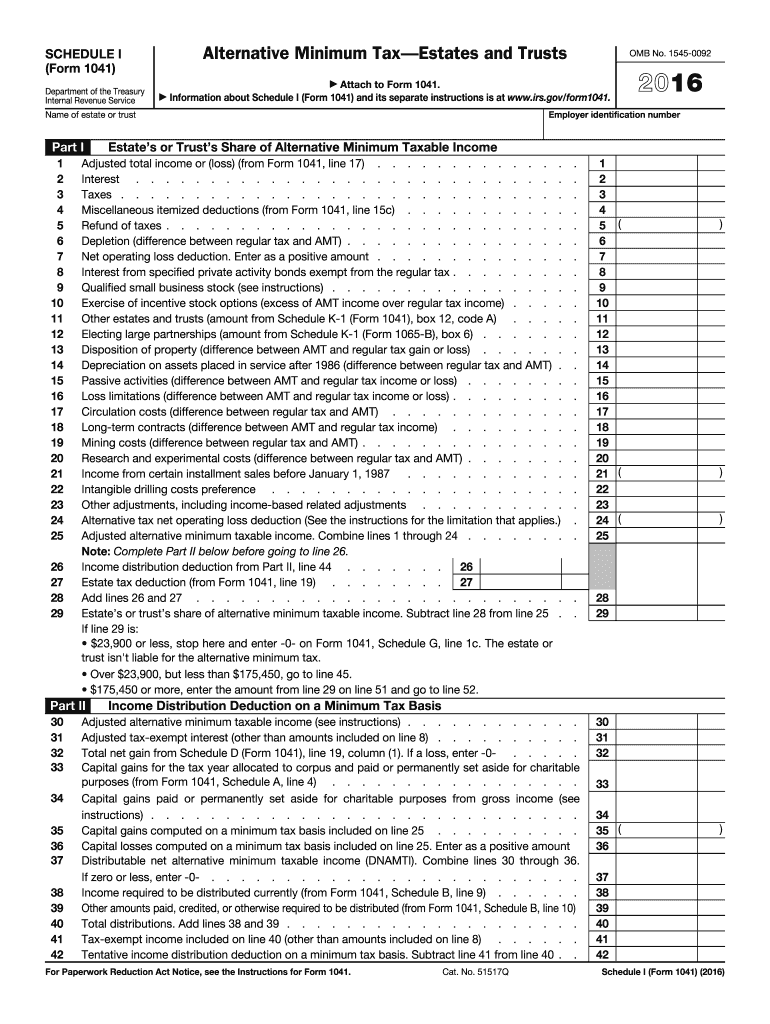

The 2016 Estates Form, specifically known as Schedule I (Form 1041), pertains to the Alternative Minimum Tax (AMT) for estates and trusts. This form is used to calculate an estate's or trust's share of alternative minimum taxable income. The AMT was designed to ensure that entities with significant income cannot eliminate their tax liability through deductions and other tax benefits. In understanding this form, one must recognize its role in adjusting the regular income tax liability of estates and trusts to account for various income and deduction modifications.

This form is integral for those managing estate or trust finances, as it mandates the accounting of specific payouts and adjustments, ensuring compliance with federal tax obligations. The form may involve various key calculations involving taxable income thresholds, making it essential for effective financial planning and regulatory adherence.

How to Use the 2016 Estates Form

To utilize the 2016 estates form correctly, you must follow a step-by-step process:

-

Gather Necessary Documents: Start by collating all financial records pertinent to the estate or trust. This includes income statements, records of deductions, and any documents detailing distributions made over the tax year.

-

Identify AMT Adjustments: Calculate the alternative minimum taxable income by making specific adjustments and exclusions from regular taxable income. This typically includes treatment of capital gains, investment interest, and other distinct income sources.

-

Complete the Form: Fill out Schedule I (Form 1041) using gathered documentation and calculated adjustments. Ensure each section of the form is accurately completed, reflecting income appropriations and AMT obligations accurately.

-

Review for Accuracy: Before submission, double-check all entries for accuracy to prevent IRS rejections or requests for additional information. Misfiling can lead to penalties or delayed processing.

Steps to Complete the 2016 Estates Form

The completion of the 2016 Estates Form involves several critical steps:

-

Download the Form: Obtain the form from the IRS website to ensure you have the most updated version.

-

Complete General Information: Fill in identifying information concerning the estate or trust, including name, fiduciary name, and address.

-

AMT Income Calculation: Enter income data in the provided sections, making necessary adjustments for the AMT. This typically involves reporting capital gain distinctions and stating interest differences.

-

Determine Tentative Minimum Tax: Calculate the tentative minimum tax using the income figures and applicable rate brackets.

-

Tax Credits and Payments: Deduct any eligible tax credits or prepayments from the tentative minimum tax to determine final tax liability.

-

Final Review and Submission: Conduct a thorough review of the completed form. Submit the form either electronically or by mail, as per typical IRS submission guidelines.

Important Terms Related to the 2016 Estates Form

Understanding key terminology is crucial for navigating the 2016 estates form:

-

Alternative Minimum Tax (AMT): A parallel tax system meant to ensure tax liability consistency across high-income entities.

-

Tentative Minimum Tax: An initial computation of AMT liability based on adjusted income and applicable rates.

-

Financial Distributions: The disbursement of assets or income from trusts or estates to beneficiaries, influencing taxable income considerations.

-

Exemptions and Deductions: Specific allowances reducing income subject to AMT, necessitating precise documentation and eligibility verification.

Legal Use of the 2016 Estates Form

The 2016 Estates Form has significant legal implications for estate and trust management in the U.S. It is imperative for executors and fiduciaries to file this form accurately, as failure to do so may result in penalties or legal ramifications. The form ensures compliance with the Tax Code, governing how trusts and estates contribute to overall tax revenues. Non-compliance could lead to audits or legal challenges, necessitating meticulous attention to form instructions and IRS guidelines.

Filing Deadlines / Important Dates

Like most IRS forms, Schedule I (Form 1041) abides by strict filing deadlines which must be adhered to for compliance:

-

Filing Deadline: The form should be filed by April 15th for trusts and estates on a calendar year schedule.

-

Extensions: If needed, extensions are available by filing IRS Form 7004, which grants an additional six months to submit the required documentation.

Missing these deadlines could result in penal fees or interest charges, heightening the importance of adherence to the IRS timeline. Ensure you mark these dates on your calendar and plan in advance to collect all necessary documentation.

Required Documents for the 2016 Estates Form

Providing appropriate documentation is critical:

-

Income and Expenses Records: Detailed financial statements showcasing all sources of income and expenses attributed to the estate or trust.

-

Distribution Records: Documents detailing any distributions to beneficiaries, affecting taxable income calculations.

-

Previous Tax Filings: Copies of prior years’ tax filings can aid in consistency and validation of reported figures for comparison and compliance.

Gathering these documents in advance will ensure you have all necessary information for accurate form completion and submission, mitigating potential compliance risks.

Who Typically Uses the 2016 Estates Form

The 2016 estates form is predominantly used by:

-

Executors of Estates: Individuals appointed to manage the estate of a deceased person, ensuring proper distribution and compliance with legal tax obligations.

-

Trustees: Individuals or entities responsible for managing trusts, requiring due diligence in handling tax matters under IRS scrutiny.

Understanding the role of involved parties is essential for ensuring that tax matters are handled appropriately, fulfilling legal responsibilities and maintaining transparency with beneficiaries.

By focusing on these critical aspects, executors and trustees can confidently navigate the complexities of estate and trust taxation.