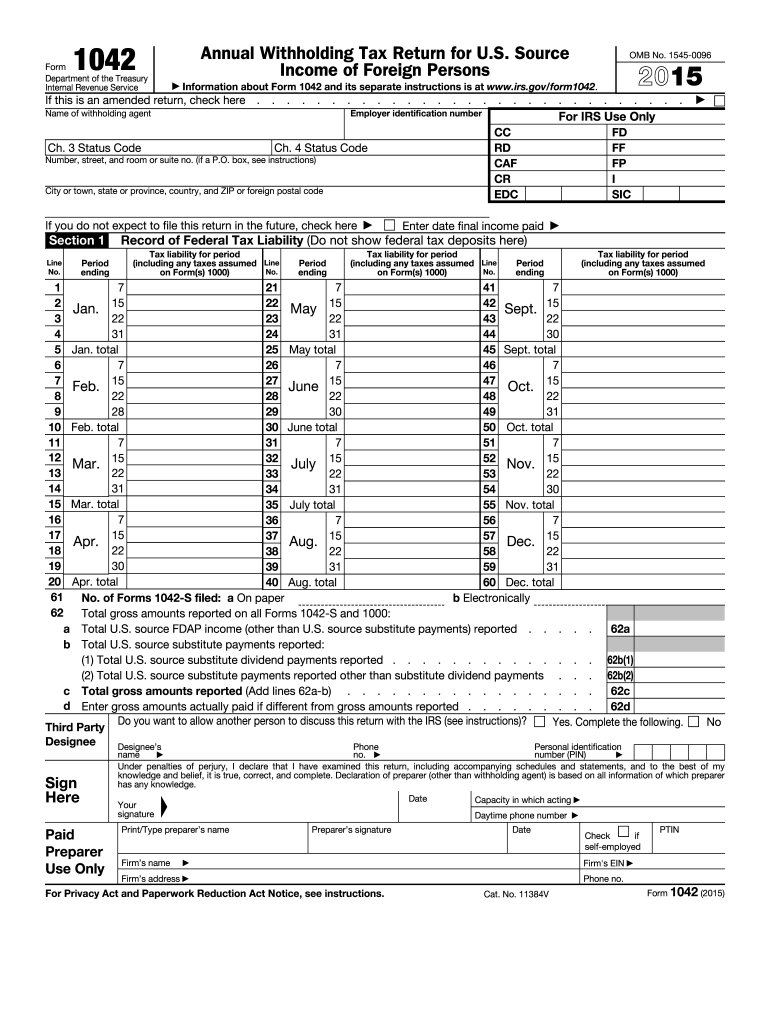

Definition & Purpose of the 2015 Form 1042

The 2015 Form 1042 is officially known as the "Annual Withholding Tax Return for U.S. Source Income of Foreign Persons." It is used by withholding agents, such as businesses and financial institutions, to report and remit taxes for certain types of income paid to foreign individuals or entities. The purpose of this form is to ensure proper tax compliance on U.S. source income that is subject to withholding under IRS regulations. This includes income types such as dividends, interest, royalties, and other fixed or determinable annual or periodic income (FDAP).

A key element of the Form 1042’s function is to reconcile the total tax withheld during the calendar year with the corresponding payments made to the IRS. The document requires reporting detailed tax liabilities and reconciliation information, ensuring that foreign income recipients have been assessed the correct withholding amounts.

How to Obtain the 2015 Form 1042

Obtaining the 2015 Form 1042 is straightforward and can be achieved in several ways to suit your convenience. The form can be downloaded directly from the official IRS website, which is the most reliable option to access the most recent version.

- Online Access: The IRS website offers the form in PDF format, allowing you to download it directly to your computer.

- Tax Software: Many tax software programs include the forms needed for tax preparation, including Form 1042. This integration can simplify the process if you're already using such software for filing.

- Request by Mail: You may also request a physical copy of the form to be mailed to you by contacting the IRS directly. This option is suitable if you prefer to work with paper documents.

Steps to Complete the 2015 Form 1042

Filling out the 2015 Form 1042 involves several detailed steps. It is critical to follow these procedures to ensure accuracy and compliance.

- Aggregate Information: Begin by gathering all necessary information about the U.S. source income paid to foreign individuals or entities. This includes the total amounts paid and respective withholding amounts.

- Enter Withholding Agent Details: Complete Part I with the withholding agent's identification details, including name, address, and taxpayer identification number (TIN).

- Provide Income and Withholding Amounts: In Part II, report the total income subject to withholding and the actual tax withheld during the year.

- Reconcile Payments: Part III requires the reconciliation of actual payments made during the year with the reported withholding obligations.

- Sign and Date the Form: Ensure that the form is signed and dated by an authorized person before submission.

Who Typically Uses the 2015 Form 1042

The primary users of the 2015 Form 1042 are withholding agents who handle payments of U.S. source income to foreign entities. These agents include:

- Banks and Financial Institutions: For interest and dividend payments.

- Corporations: Reporting royalties and other income distributed to foreign shareholders or partners.

- Insurance Companies: Reporting income connected to non-U.S. parties.

- Governmental and Non-Governmental Entities: Dealing with payments to foreign contracts or suppliers.

This form is essential for these entities to remain in compliance with U.S. tax laws and to ensure the appropriate withholding tax is remitted to the IRS on behalf of foreign recipients.

Key Elements of the 2015 Form 1042

Form 1042 contains several key sections that are crucial for its accurate completion:

- Tax Liability and Reconciliation: A critical component that compares the total tax withheld against the required withholding.

- Attachment Requirement: Supporting documents, such as 1042-S forms, must be included to validate reported amounts.

- Amendments and Adjustments: Instructions for making amendments to previously submitted forms or to correct discrepancies from earlier submissions.

The thorough completion of these elements ensures that all relevant income and withholding information is accurately represented.

Filing Deadlines and Important Dates

Proper timing is crucial when dealing with Form 1042. Withholding agents must adhere to the following deadlines:

- Annual Filing Deadline: Typically, the form is due on March 15 of the year following the tax year for which the income is paid. If the deadline falls on a weekend or holiday, it will be adjusted to the next business day.

- Extension Requests: If additional time is needed, withholding agents can file Form 7004 to request an extension. It’s important to note that an extension of time to file is not an extension to pay taxes owed.

Penalties for Non-Compliance

Failure to duly complete and submit the 2015 Form 1042 may result in significant penalties. Common penalties include:

- Late Filing Penalty: A percentage of the unpaid tax can be assessed for late filings.

- Underpayment Penalty: Additional charges may apply if the reported withholding is less than required.

Non-compliance can lead to further scrutiny during audits and potential legal action, making it essential for withholding agents to accurately and timely file the form.

Software Compatibility and Digital Management

Leveraging digital tools can simplify the preparation and filing of Form 1042. Compatible software includes:

- Tax Preparation Software: Tools like TurboTax or QuickBooks can assist with calculations and filings.

- Document Management Solutions: Platforms such as DocHub can aid in editing, signing, and managing digital copies of the form. This digital compatibility ensures seamless transitions from preparation to filing without sacrificing accuracy.

Overall, the 2015 Form 1042 plays a critical role in the compliance landscape for withholding agents paying U.S. source income to foreign parties. Properly understanding and utilizing the form ensures adherence to tax obligations and helps maintain international financial relationships.