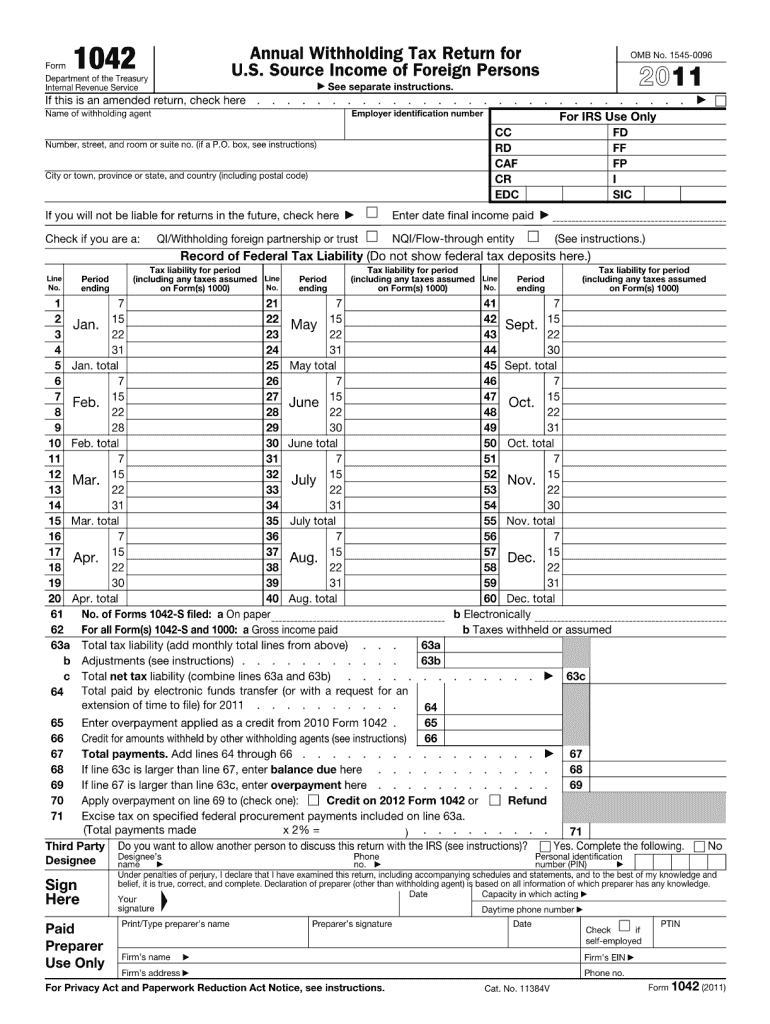

Definition and Meaning of 2011 Form 1042

Form 1042 is used by withholding agents to report tax withheld on certain income of a foreign person. Specifically, this form is relevant for reporting amounts withheld on U.S. source income paid to foreign recipients. The form addresses taxes withheld on payments such as interest, dividends, rents, royalties, and other fixed or determinable income. In 2011, Form 1042 encapsulated the regulations and compliance requirements pertaining to tax withheld at source for foreign payees and was crucial for ensuring proper reporting and remittance to the IRS. Unlike forms related to domestic transactions, Form 1042 addresses international tax compliance, emphasizing the need for accurate and comprehensive documentation.

How to Use the 2011 Form 1042

To correctly utilize the 2011 Form 1042, withholding agents must first identify the taxable U.S. source income paid to foreign persons. Key steps include calculating the amount subject to withholding, applying the applicable tax rate as per applicable tax treaties or standard IRS rates, and subsequently documenting all transactions accurately. The form itself requires detailing information such as the type of income, the total amount reported, the total taxes withheld, and specific details about the foreign payee. As the form incorporates complex tax regulations, consulting the IRS instructions for Form 1042 is advisable to understand nuanced filing requirements and ensure compliance.

Steps to Complete the 2011 Form 1042

-

Gather Necessary Information: Collect all relevant financial records, including details about payments, withholding amounts, and information about recipients.

-

Determine Applicable Tax Rates: Review the applicable tax treaties or IRS guidelines to determine the correct withholding rates.

-

Fill Out Income Details: Enter details on income types, total amounts, and any specific categories required by the form.

-

Calculate Total Tax Withheld: Accurately report the total taxes withheld from payments made to foreign persons.

-

Complete Identification Sections: Provide specific details about the withholding agent and foreign recipient, including names, addresses, and tax identification numbers where applicable.

-

Review for Accuracy: Double-check all entries for correctness to avoid errors that could lead to penalties.

-

Submit the Form: File the completed form with the IRS before the deadline, typically March 15 following the tax year in question.

Key Elements of 2011 Form 1042

The 2011 Form 1042 includes several critical components: identifying information for the withholding agent, detailed breakdowns of income paid to foreign persons, the applicable tax treaty-based rates or default rates used, and total amount of tax withheld. Supplemental schedules may be required to provide further detail about particular income categories and transactions, as well as backup withholding where applicable. The accuracy and thoroughness in these sections directly influence compliance with IRS requirements.

IRS Guidelines for 2011 Form 1042

The IRS guidelines for the 2011 Form 1042 detail the specific obligations of withholding agents regarding documentation, calculation, and remittance of taxes on U.S.-sourced income paid to foreign entities. Responsibilities encompass precise reporting of each transaction within the proper sections of the form and ensuring all applicable tax treaties are honored. The guidelines emphasize readiness to supply additional documentation if audited and clarify terms such as effectively connected income, withholding responsibilities, and treaty benefits.

Filing Deadlines and Important Dates

Deadlines play a pivotal role in the filing of the 2011 Form 1042. Generally, the form was due by March 15 following the tax year, allowing withholding agents sufficient time to compile and verify financial information. Adhering to this deadline was crucial to avoid possible penalties and interest charges from the IRS. In instances where the deadline could not be met, withholding agents needed to consider filing for extensions well in advance, in accordance with IRS extension provisions.

Penalties for Non-Compliance with 2011 Form 1042

Failing to file the 2011 Form 1042 or filing it inaccurately could result in significant penalties. The IRS imposed penalties based on lateness, errors in the reported amounts, or neglecting to provide requested information. Financial penalties could escalate depending on the length of delay and severity of inaccuracies. Furthermore, repeated non-compliance could attract more scrutiny from the IRS and increased audit risk, underscoring the importance of meticulous filing and adherence to compliance requirements.

Digital vs. Paper Versions of 2011 Form 1042

The 2011 Form 1042 was available in both digital and paper formats. Filing electronically offered several advantages, such as faster processing and error-checking mechanisms, which helped reduce risks associated with manual data entries. Additionally, digital submissions facilitated easier record-keeping and retrieval. For those opting for paper submissions, attention to detail was necessary to ensure clarity and completeness, as paper forms required manual checks which were more prone to human errors.

Business Entity Types That Use the 2011 Form 1042

A diverse range of business entities needed to file the 2011 Form 1042, encompassing corporations, partnerships, trusts, and any other legal entity that made payments subject to withholding laws to foreign individuals or organizations. The classification of the business entity impacted how withholding was applied and reported. For multinational corporations and partnerships engaging with non-U.S. partners or stakeholders, the form played an integral role in maintaining tax compliance and transparency in cross-border transactions.

Who Issues the 2011 Form 1042

The Internal Revenue Service (IRS) is responsible for the issuance of the Form 1042. The IRS provides the relevant compliance framework and necessary instructions that govern how withholding agents are to report taxes withheld on foreign income. Through periodic updates and communications, the IRS ensures that any legal or regulatory changes impacting the form are communicated to withholding agents, aiding them in their compliance processes.