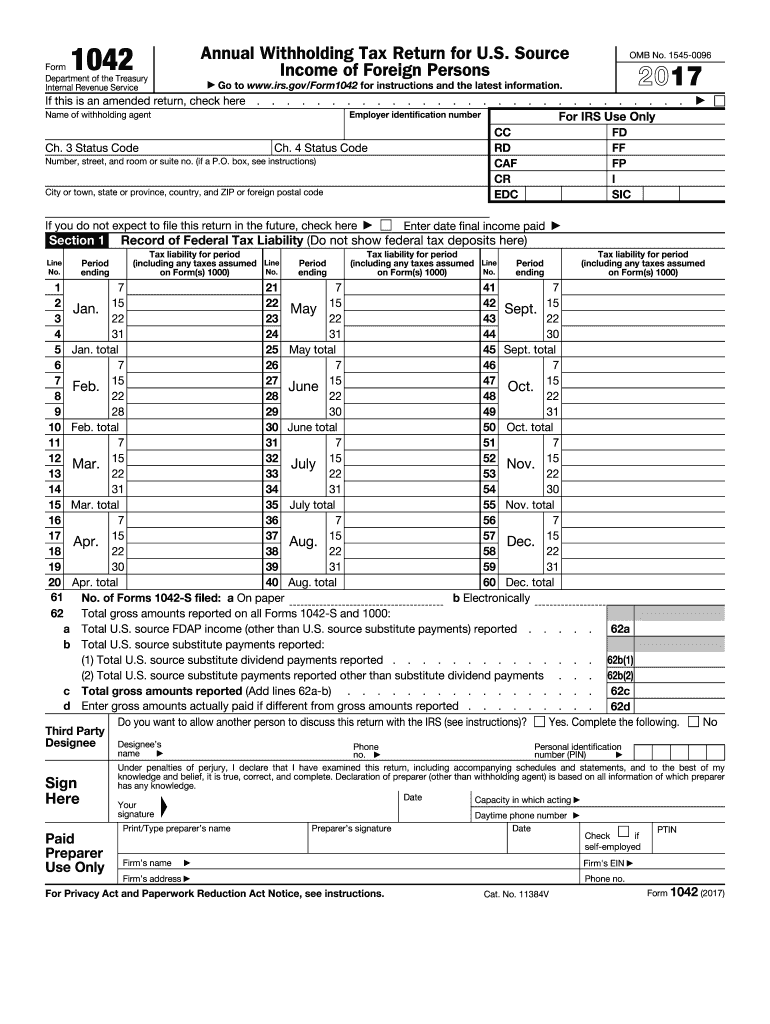

Definition & Meaning

Form 1042 is the Annual Withholding Tax Return for U.S. Source Income of Foreign Persons. It is primarily used by withholding agents to report tax withheld on income paid to non-resident aliens and foreign entities. This form ensures that taxes on income like interest, dividends, or royalties, which originate from U.S. sources, are appropriately reported and paid to the IRS. It encompasses various reporting requirements related to Fixed, Determinable, Annual, or Periodical (FDAP) income that these foreign individuals or businesses might earn from U.S. sources.

How to Obtain Form

Acquiring Form 1042 for the year 2017 is a straightforward process. It can be directly downloaded from the Internal Revenue Service (IRS) website. This digital availability ensures that withholding agents can easily access the necessary documentation without hassle. Alternatively, you can request a paper version by contacting the IRS, though this method might take additional time due to mailing processes. Ensuring you have the latest version of the form is crucial for compliance and accurate filing.

Steps to Complete Form

Gathering Information

- Identify Withholding Agent Details: Include the name, address, and Taxpayer Identification Number (TIN) of the withholding agent.

- Report Income Types: Enumerate all types of FDAP income paid to foreign entities or individuals.

- Calculate Withholding: Accurately determine the amounts withheld based on the applicable rates.

Filling Out the Form

- Line-by-Line Instruction: Start with calculating the total income subject to withholding.

- Reconcile Payments: Include any adjustments or credits against the withholding amount.

- Account for Any Penalties: Ensure that all necessary information and calculations are completed to avoid potential penalties.

Final Review and Submission

- Double-check all entries for accuracy.

- Submit the form via the preferred method ensuring that it is postmarked by the due date, typically March 15.

Who Typically Uses Form

The primary users of Form 1042 are withholding agents, including U.S. companies, financial institutions, and other entities that handle payments to foreign persons. These agents ensure that taxes on income like interest, royalties, and dividends are withheld and reported. The form is essential for meeting legal obligations and avoiding penalties for non-compliance. Foreign entities receiving U.S.-sourced income but expecting no direct obligation to fill the document thoroughly depend on their withholding agents to fulfill this duty correctly.

Key Elements of Form

- Withholding Agent's Information: Identification of the entity responsible for withholding.

- FDAP Income Types: The specific categories of income subject to withholding.

- Tax Liability Calculations: Accurate computation of taxes withheld.

- Country Codes: The relevant codes for countries that foreign income recipients are associated with.

- Refund Claims: Sections to claim any overpayments or adjustments made during the year.

IRS Guidelines

The IRS provides comprehensive guidelines for the accurate completion and timely filing of Form 1042. These regulations include detailed instructions on how to report various types of FDAP income and apply appropriate withholding rates. Furthermore, the guidelines explain the reporting requirements for various situations, such as affiliations with multiple jurisdictions or entities.

Filing Deadlines / Important Dates

Form 1042 for the year 2017 must typically be filed by March 15 of the following year. Filing by this date ensures compliance and avoids late submission penalties. Be prepared to submit any payments due alongside this form by the same deadline. The IRS permits electronic submissions through approved channels, streamlining compliance for withholding agents with larger volumes of transactions.

Penalties for Non-Compliance

Failing to file Form 1042 by the due date, or providing incorrect information, can lead to significant penalties. The IRS may impose fines based on the degree of incompleteness or inaccuracy of the filed form. Withholding agents must be diligent in ensuring the proper calculations and complete reporting to avoid these punitive measures. In severe cases, non-compliance could lead to legal challenges or audits by the IRS.

Digital vs. Paper Version

There are two primary methods to process Form 1042: digital and paper versions. The digital version, typically submitted through the IRS's FIRE system, offers quicker processing and confirmation of receipt. The paper form may be useful for entities with limited digital access but involves a more extended processing period and the risk of mailing delays. Choosing the right method depends on the organization's infrastructure and preference for confirmation or record-keeping.