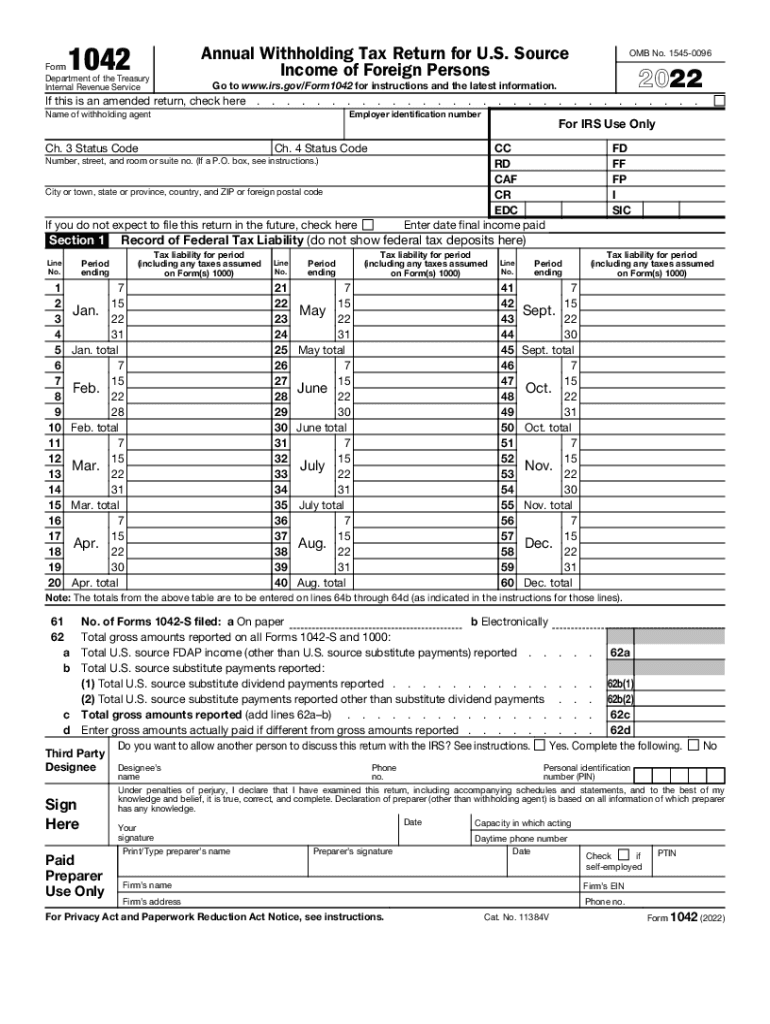

Definition and Purpose of Form 1042

Form 1042, officially titled the "Annual Withholding Tax Return for U.S. Source Income of Foreign Persons," is issued by the Internal Revenue Service (IRS) for reporting taxes withheld on payments to foreign persons. Withholding agents, such as financial institutions or employers, use this form to report and pay taxes on U.S. source income distributed to foreign individuals or entities. Notably, it includes sections to declare tax liabilities, reconcile accounts, and detail potential adjustments linked to Foreign-Derived Amounts Paid (FDAP) income, Section 871(m) transactions, and dividend equivalent payments.

How to Use Form 1042

When preparing Form 1042, withholding agents report all relevant income payments with corresponding tax withholdings. This involves a thorough review and entry of details concerning the identity of each recipient, the type of income paid, and the amount withheld in U.S. dollars. Additionally, withheld taxes must be matched with the payments made throughout the tax year. This form helps the IRS monitor and ensure proper taxation and compliance with U.S. tax laws regarding foreign income.

Obtaining Form 1042

The IRS provides Form 1042 through its official website, where users can download and print the form. Furthermore, taxpayers can receive it by mail upon request or by visiting local IRS offices. Online accessibility ensures that withholding agents can efficiently acquire and prepare forms as part of their tax documentation process.

Steps to Complete Form 1042

- Initiate the Form: Start by entering the withholding agent’s identifying information, including name, address, TIN, and more.

- Income Reporting: Record all U.S. source income payments made to foreign persons during the year, ensuring all categories, such as fixed or determinable annual or periodical (FDAP) income, are captured accurately.

- Withholding Details: Declare the total amounts withheld and deposited with the IRS, verifying that they align with the reported payments.

- Supporting Documentation: Attach forms 1042-S, which provide a detailed breakdown of each payment recipient and associated tax information.

- Review and Submit: Double-check for accuracy and submit the form by the specified deadline, typically March 15 of the following year.

Filing Deadlines and Important Dates

Form 1042 must be submitted annually by March 15. This deadline is crucial to avoid penalties for late filing. Withholding agents should ensure that all supportive documentation, such as Form 1042-S, is prepared timely alongside the primary form. Meeting this deadline helps maintain compliance with tax regulations.

Required Documentation for Form 1042

- Form 1042-S: Provides details of each individual income recipient and the amounts withheld.

- Tax Identification Number (TIN): Ensures legal identification of all relevant parties.

- Payment Records: Evidence of all payment transactions to foreign persons, including the associated tax withholdings.

Legal Implications of Form 1042

Form 1042 holds significant legal weight, serving as a formal declaration of withheld taxes and payments to foreign persons. It plays a vital role in U.S. tax law enforcement, requiring precise information to maintain compliance and avoid legal issues. Inaccurate reporting or omission could result in severe penalties or audits by the IRS.

Penalties for Non-Compliance

Failure to file Form 1042 accurately or submit it on time may lead to penalties. The IRS imposes fines based on the severity and intent of the non-compliance. Deliberate evasion could lead to higher fines, while honest mistakes usually result in lesser penalties. Ensuring accurate and timely filing is key to avoiding these repercussions.