Definition and Purpose of the 2014 Form 1042

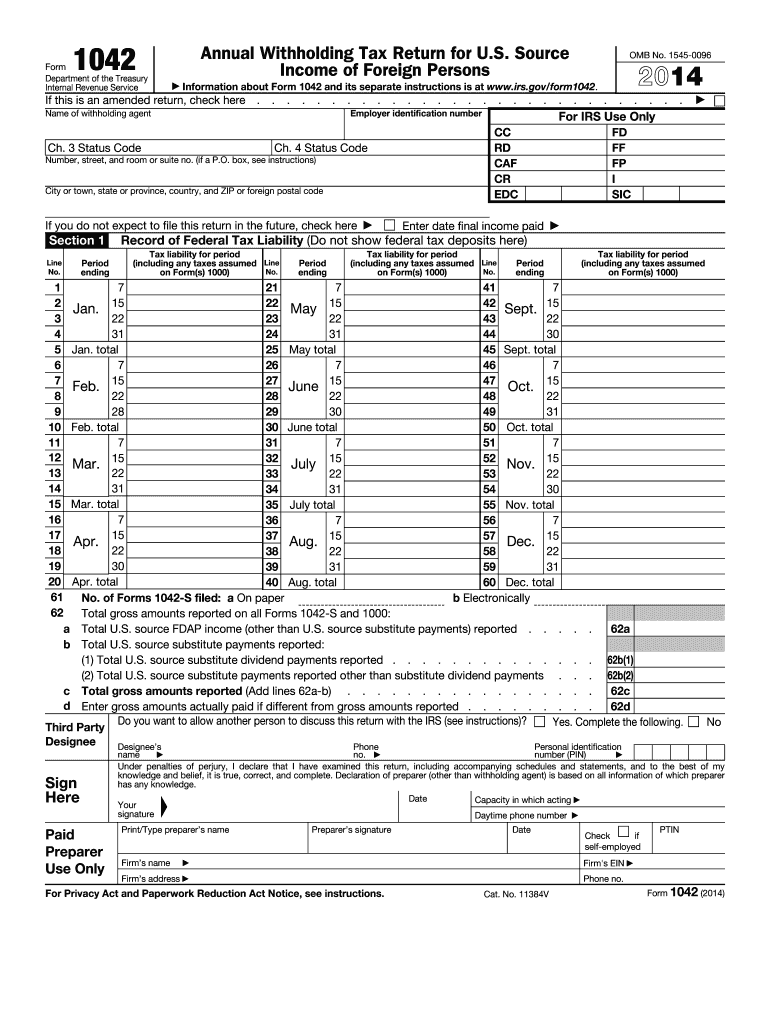

The 2014 Form 1042, also known as the Annual Withholding Tax Return for U.S. Source Income of Foreign Persons, is primarily used by withholding agents in the United States to report tax withheld on certain types of U.S. source income paid to foreign persons. This includes interest, dividends, royalties, and other types of income that fall under the jurisdiction of U.S. tax laws. The form plays a critical role in ensuring compliance with the Foreign Account Tax Compliance Act (FATCA), introduced to improve tax compliance and combat tax evasion.

Key Elements of the 2014 Form 1042

The form is divided into several essential sections, each requiring detailed information:

- Withholding Agent's Information: Critical details about the withholding agent, such as name, address, and employer identification number (EIN).

- Income Types and Amount Withheld: Detailed reporting of the types of income paid and the tax withheld for each type.

- Country-Specific Tax Details: Information on tax rates applicable under tax treaties between the United States and the recipient's country of residence.

- Tax Liability Allocation: Breakdown of any adjustments, refunds, or credits applicable to the withheld tax.

Steps to Complete the 2014 Form 1042

Completing the form involves a methodical approach:

- Gather Information: Collect all necessary data about the withholding agent, recipients, and income classifications.

- Report Income Types: Accurately classify and record all income payments subject to withholding.

- Compute Tax: Use applicable tax treaties and rates to determine the correct amount of withholding tax.

- Verify Withholding Amounts: Double-check calculations to ensure accuracy.

- Complete Form Sections: Fill in each section of the form clearly and accurately, using guidance from IRS instructions.

- Review and Sign: Ensure all information is correct before signing and submitting the form.

IRS Guidelines for the 2014 Form 1042

The IRS provides detailed guidance on completing and filing the form, including:

- Form Instructions: Comprehensive instructions are available on the IRS website, detailing how to fill out each section.

- Filing Deadlines: The form is typically due by March 15 of the year following the calendar year in which the income was paid.

- Amendments and Corrections: Procedures are in place for amending filed forms if errors are discovered after submission.

Legal Use and Compliance of the 2014 Form 1042

Adhering to legal requirements involves:

- Understanding FATCA: The form reflects compliance needs under FATCA, applicable for financial institutions and withholding agents.

- Ensuring Accurate Reporting: Misreporting or non-compliance can result in significant penalties.

- Maintaining Record Security: Sensitive information must be securely managed to protect against data breaches.

Filing Deadlines and Important Dates for the 2014 Form 1042

Timely filing is critical:

- Annual Deadline: March 15 is the standard deadline for submitting the form.

- Extended Deadlines: Extensions can be requested, but they must be filed before the original due date.

- Penalties for Late Filing: Failing to meet deadlines can incur penalties, including fines and increased scrutiny from the IRS.

Software Compatibility and Submission Methods

Form 1042 can be managed using various platforms:

- Compatible Software: Programs like TurboTax and QuickBooks offer compatibility for filling and filing the form.

- Submission Methods: The form can be submitted electronically via the IRS's FIRE system or by mail for those filing paper forms.

Penalties and Compliance Risks for Non-Submission

Non-compliance entails significant risks:

- Penalties: Financial penalties vary based on the extent and nature of the compliance failure.

- Risks to Business: Ongoing non-compliance can lead to audits, loss of treaty benefits, and reputational damage.

Examples and Scenarios of Using the 2014 Form 1042

Examples of usage include:

- Financial Institutions: Banks use the form to report interest payments to foreign account holders.

- Multinational Corporations: Corporations report dividends or royalties paid to foreign shareholders or licensors.

- Partnerships: Partnerships fulfilling roles as withholding agents for payments to foreign partners.

These sections provide a comprehensive understanding of the 2014 Form 1042, highlighting its importance, requirements, and applications within the context of ensuring tax compliance for foreign income paid by U.S. withholding agents.