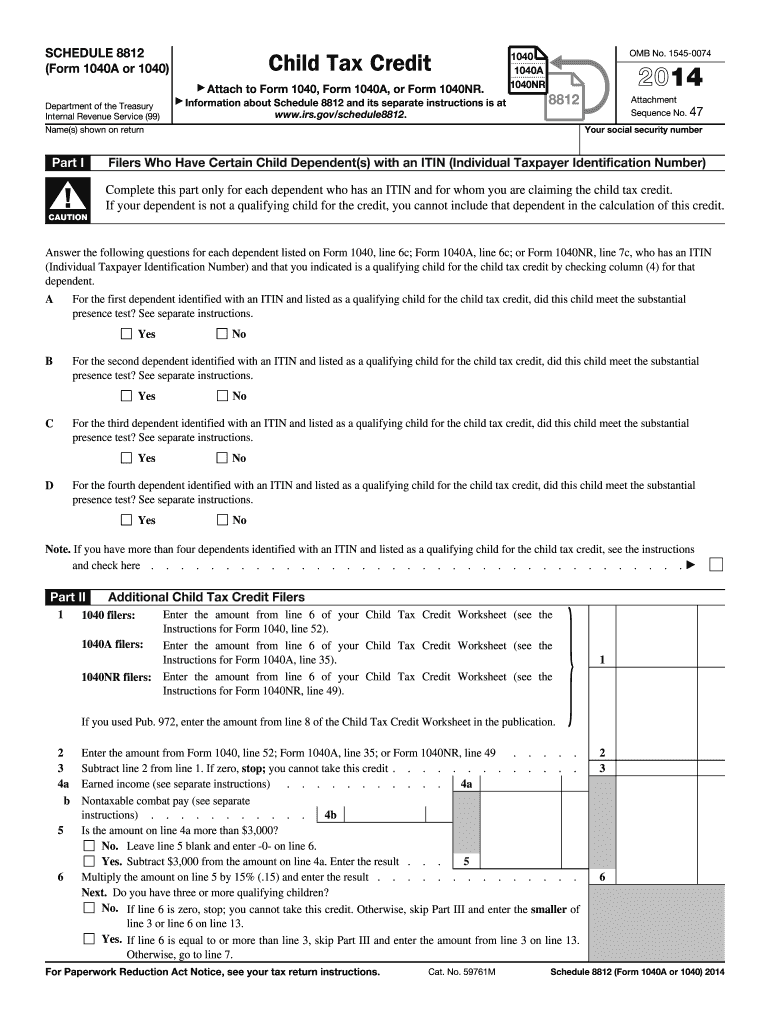

Definition and Purpose of the 2014 Form 8812

The 2014 Form 8812, also known as Schedule 8812, is a tax document used to claim the Additional Child Tax Credit. This credit is intended for taxpayers who qualify for the Child Tax Credit but are unable to claim the full amount due to insufficient tax liability. Designed to support working families, this form allows eligible individuals to receive a refund that exceeds their owed tax. The form includes sections that help calculate the credit based on income and the number of qualifying children.

How to Use the 2014 Form 8812

Using the 2014 Form 8812 involves a series of steps to determine eligibility and the amount of credit. Taxpayers must first complete the Child Tax Credit worksheet found in the Form 1040 instructions. After calculating the Child Tax Credit, taxpayers use Form 8812 to determine if they qualify for the Additional Child Tax Credit. The form requires detailed information about income and qualifying children to compute the amount of refundable credit, which is then entered on Form 1040.

- Start by determining if you qualify for the regular Child Tax Credit.

- Use the form to calculate any additional refundable credit you may be eligible for.

- Report the calculated refundable credit on the appropriate line of your Form 1040.

Steps to Complete the 2014 Form 8812

Completing the 2014 Form 8812 requires careful attention to detail. Follow these steps for accurate completion:

- Identify Qualifying Children: Enter the names, Social Security numbers, and other required information for each child who qualifies.

- Calculate Income Limits: Utilize the worksheets provided to calculate your modified adjusted gross income.

- Determine Base Credit: Use part I of the form to figure out the initial credit based on your income and number of children.

- Adjust for Additional Credit: Complete part II to determine if an additional credit is applicable.

- Finalize Calculations: Transfer the final amount to your Form 1040.

Who Typically Uses the 2014 Form 8812

The primary users of the 2014 Form 8812 are taxpayers who have qualifying children and earn income that might not be sufficient to claim the full Child Tax Credit. Typically, these include:

- Families with multiple dependents

- Low-to-moderate income earners

- Individuals with a tax liability that is lower than their eligible credit

Eligibility Criteria for the 2014 Form 8812

Eligibility for the 2014 Form 8812 involves several criteria:

- Children: Must have Social Security numbers and meet the IRS-defined relationship and age requirements.

- Income: Your earned income must exceed a specific threshold to qualify for the additional credit.

- Filing Status: Taxpayers must file Form 1040 or Form 1040A.

Key Elements of the 2014 Form 8812

Form 8812 is structured to capture crucial information necessary to compute the Additional Child Tax Credit:

- Part I: Figures the initial Child Tax Credit.

- Part II: Calculates any additional refundable credit.

- Supporting Documents: May require additional worksheets to ensure accurate submission.

Required Documents for the 2014 Form 8812

To correctly fill out Form 8812, gathering the right documents is vital:

- Social Security numbers for all qualifying children

- Income documents such as W-2s or 1099s

- Previous years' tax returns for reference, if applicable

- Completed Child Tax Credit worksheet from Form 1040 instructions

IRS Guidelines for the 2014 Form 8812

The IRS guidelines for using Form 8812 are designed to ensure accuracy and compliance:

- Keep Records: Maintain records of all documents and calculations for at least three years.

- Follow Instructions: Carefully read the form instructions to ensure all income and child data are accurate.

- Amended Returns: If errors are discovered after filing, an amended return should be submitted using Form 1040X.

Filing Deadlines and Important Dates

Adhering to filing deadlines is crucial to claim the Additional Child Tax Credit using Form 8812:

- Filing Deadline: Typically, April 15th of the following year.

- Extensions: File Form 4868 for an automatic six-month extension if you need more time.

- Amendments: File any amended returns by the deadline for claiming a refund, usually three years from the original filing date.

Penalties for Non-Compliance

Failing to accurately complete and submit Form 8812 can result in penalties:

- Late Filing Penalties: Failure to file by deadlines may result in fines.

- Accuracy-Related Penalties: Significant inaccuracies or omissions might incur further fees from the IRS.

- Forfeiting the Credit: If the form is not submitted correctly or timely, you may lose eligibility for the credit.

Software Compatibility for the 2014 Form 8812

Many taxpayers use software to simplify the form completion process:

- TurboTax and QuickBooks: Compatible with these platforms to automate calculations and submissions.

- Tax Preparation Services: Many offer compatibility features to ensure precision and ease for preparing taxes with Form 8812.

State-Specific Rules for the 2014 Form 8812

While Form 8812 is a federal form, some states have their own rules regarding tax credits:

- Check State Requirements: Each state may have distinct tax rules affecting credits.

- State Credits: Some offer additional child-related tax incentives that may complement the federal Additional Child Tax Credit.

Digital vs. Paper Version

Taxpayers opting for digital submission over traditional paper filing can benefit from:

- Efficiency: Electronic filing ensures quicker processing and potentially faster refunds.

- Accuracy: Software checks reduce human error, particularly with complex calculations.

- Record Keeping: Digital storage of submitted forms streamlines future tax preparation and record management.