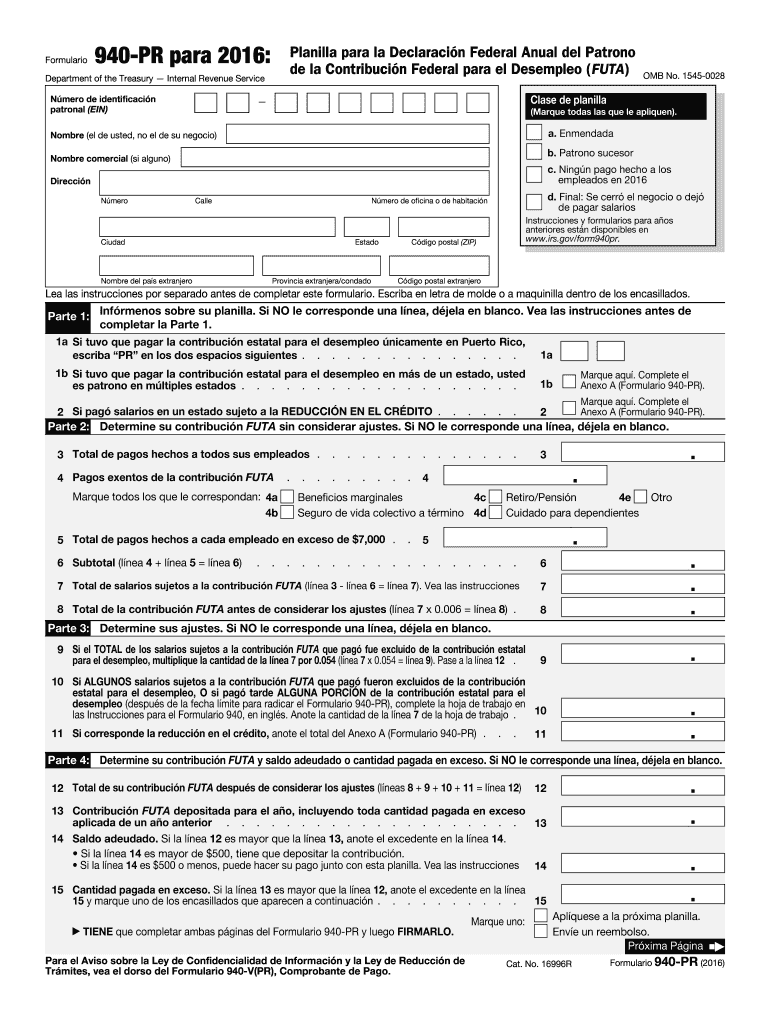

Definition and Purpose of Form 940-PR for 2016

Form 940-PR is the Puerto Rico version of the Federal Unemployment Tax Act (FUTA) annual tax return for employers. It is used to report unemployment contributions and associated tax liabilities. Employers in Puerto Rico use this form to calculate their FUTA tax obligations, which help fund unemployment compensation to workers who have lost their jobs. The form includes various sections to detail employee wages, exemptions, and adjustments necessary for accurate tax computation.

How to Use the 2016 Form 940-PR

Employers must fill out Form 940-PR to report and pay their FUTA taxes. The process involves calculating the total taxable wages paid to employees and accounting for any adjustments or credits. Here's a high-level overview of how to use the form:

- Enter Employer Information: Provide your Employer Identification Number (EIN) and other identifying details.

- Calculate Taxable Wages: List all employee wages paid during the tax year.

- Compute Adjustments: Include adjustments for exempt wages or credits for state unemployment taxes paid.

- Calculate FUTA Tax: Apply the applicable tax rate to determine the amount owed.

- Check for Overpayment or Underpayment: Adjust for any overpaid or underpaid taxes from prior years.

- Sign and Date the Form: Ensure the document is signed and dated for it to be valid.

Steps to Complete the 940-PR 2016 Form

Completing Form 940-PR can be broken down into several steps to ensure accuracy and compliance:

-

Section One: Employer Details

- Provide the name, address, and EIN of your business.

-

Section Two: Total Wage Calculation

- List total wages paid and specify which are subject to FUTA tax.

-

Section Three: Adjustments

- Deduct wages that exceed the $7,000 cap and compute any credits for state unemployment.

-

Section Four: Tax Computation

- Multiply taxable wages by the current FUTA rate (typically 0.6% but confirm for 2016).

-

Section Five: Final Review

- Recalculate your entries to check for errors or omissions and confirm figures match supporting documents.

-

Finalize and Submit

- Ensure all fields are complete, signed, and securely submitted to the IRS.

Who Typically Uses the 2016 Form 940-PR

The form is primarily used by Puerto Rican employers participating in FUTA. Eligible businesses include corporations, sole proprietorships, LLCs, and partnerships with employees in Puerto Rico. These entities must comply with both local and federal requirements for filing unemployment taxes.

Key Elements of the 2016 Form 940-PR

Form 940-PR includes several key sections:

- Employer Information: Basis for the entire filing, requiring accurate identification details.

- Taxable Wages: Documentation of all wages that constitute taxable income.

- State Credits and Adjustments: Allows businesses to reduce their tax liability by accounting for state unemployment tax payments.

- Special Allocations: Addresses different funding arrangements or reductions based on specific state agreements.

Filing Deadlines and Important Dates

For the 2016 tax year, the filing deadline for Form 940-PR was January 31, 2017. If taxes were paid in full throughout the year, a deadline extension to February 10, 2017, was allowed. Employers should verify with the IRS or consult with a tax advisor for any specific date accommodations or extensions that may apply.

Required Documents for Form 940-PR

Several documents are essential for completing Form 940-PR accurately:

- Employee Wage Statements: To determine the total taxable wages for the year.

- State Unemployment Tax Records: To apply any eligible credits or adjustments.

- Payment Records: Relevant for documenting any prior overpayments or credits.

- Employer Identification Number (EIN): Required for all tax communications.

Penalties for Non-Compliance

Failure to file Form 940-PR or payment discrepancies can result in penalties:

- Late Filing Penalties: Typically 5% of the unpaid tax per month, not to exceed 25% of the total tax due.

- False Information Fines: Penalties are assessed for providing inaccurate information knowingly.

- Interest on Underpayment: Accumulated on any unpaid tax amount from the due date until full payment is made, based on current IRS interest rates.

Employers should ensure compliance with all filing requirements and deadlines to avoid financial and legal repercussions.