Definition and Purpose of 2009 Form 706

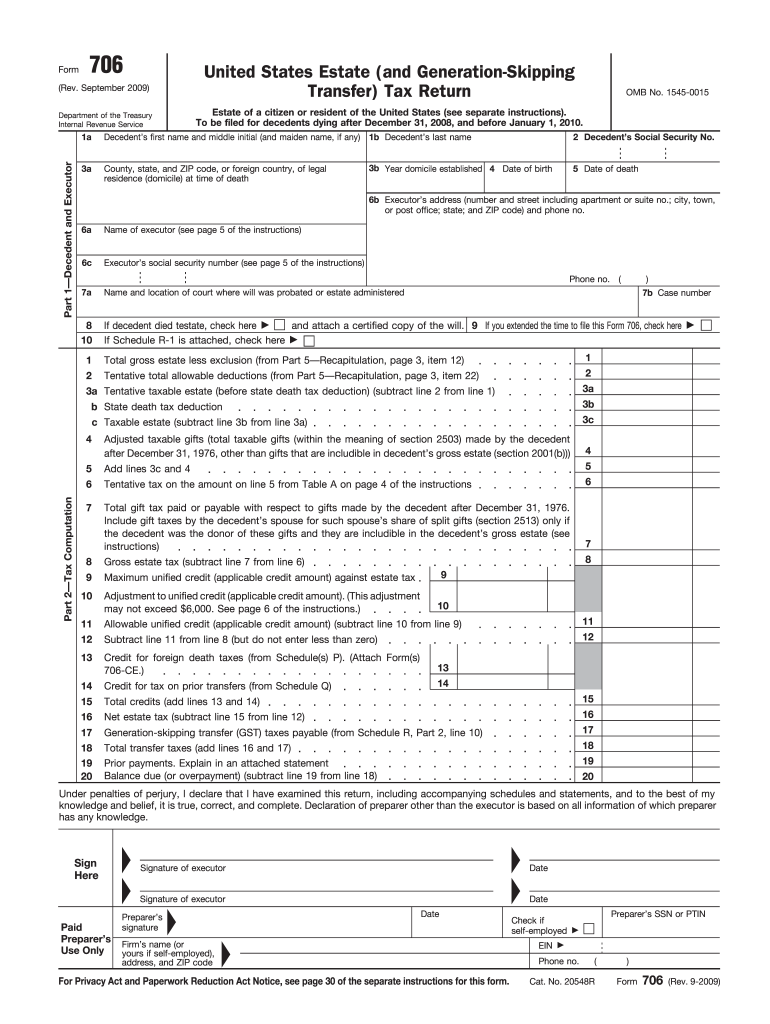

2009 Form 706 is the United States Estate (and Generation-Skipping Transfer) Tax Return. It is specifically designed for the estates of decedents who passed away between December 31, 2008, and January 1, 2010. The primary purpose of this form is to calculate and report estate taxes owed to the federal government. It includes sections for a detailed breakdown of the decedent's assets and liabilities. Executors are required to document the gross estate, which encompasses real estate, stocks, bonds, insurance policies, and any lifetime transfers made by the decedent.

Key Components of 2009 Form 706

Decedent and Executor Information

-

Decedent's Information: This section requires basic details about the decedent, including their full name, Social Security number, date of death, and citizenship status.

-

Executor's Details: The executor must provide their information, including full name, address, and contact information. This ensures clear communication and proper handling of the estate's tax matters.

Estate Valuation and Deductions

-

Asset Valuation: Executors must value all the assets in the gross estate. These include real estate properties, investments, personal belongings, and business interests.

-

Deductions: The form allows for various deductions, such as funeral expenses, outstanding debts, and charitable contributions, which can decrease the taxable estate.

How to Complete the 2009 Form 706

Gathering Required Information

- Collect comprehensive details about all assets and liabilities in the estate, including appraisals for real estate and valuations for financial assets.

- Obtain records of any taxable gifts made by the decedent to adjust the estate's value accordingly.

Completing Each Section

-

Personal Identification: Fill out the sections related to the decedent’s and executor's personal information accurately to avoid processing delays.

-

Asset Reporting: Provide a detailed report of all estate assets, using fair market values as of the date of death. Note any lifetime transactions that affect the estate's valuation.

Finalizing the Document

- Double-check all calculations and ensure all required fields are completed.

- Attach relevant documents such as appraisals, valuation reports, and proof of payment for deductible expenses.

Who Should Use 2009 Form 706

This form is intended for executors managing estates of decedents who died within the specified date range. If the value of the estate exceeds the filing threshold set by the IRS for that year, the form must be filed. This ensures compliance with federal laws regarding estate and generation-skipping transfer taxes.

Important Terms Related to 2009 Form 706

Gross Estate

- Refers to the total value of all assets owned by the decedent at the time of death, before deducting any liabilities or deductions.

Generation-Skipping Transfer (GST) Tax

- A tax on transfers of property made to beneficiaries who are two or more generations younger than the donor, like grandchildren.

Unified Credit

- A tax credit available that can reduce estate taxes owed. The amount is determined by the total value of the deceased's lifetime taxable transfers.

IRS Guidelines on Filing 2009 Form 706

Filing Deadline

- The form should be filed within nine months of the decedent's date of death. An extension can be requested if more time is needed to gather information or complete the form.

Submission Methods

- Executors can submit the form electronically through the IRS e-file system or via mail to the designated IRS processing center.

Penalties for Late Filing

- Failure to file by the deadline may result in penalties and interest. It is crucial to submit on time or request an extension to avoid financial consequences.

Required Documents for 2009 Form 706

When filing, include the following documentation:

- Copies of the decedent’s will and any trust arrangements.

- Appraisals or valuations for real estate and significant personal property.

- Financial statements detailing accounts, investments, and liabilities.

- Evidence of any prior taxable gifts or transfers.

Comparison of Digital vs. Paper Version

Digital Version

- Allows for easier revisions and quicker submission.

- Supports integration with financial software for enhanced accuracy and efficiency.

Paper Version

- Traditional method involving manual entry and physical mailing.

- Suitable for those preferring a tangible document record.

Each method has its benefits, and the choice depends on the executor's preference and resources.

State-by-State Differences in Estate Tax

While 2009 Form 706 deals with federal estate tax, each state may have its specific regulations and additional forms for state estate taxes. Executors should familiarize themselves with laws applicable in the state where the decedent was a resident to ensure complete compliance both federally and locally.