Definition and Meaning of the 1999 Form 706

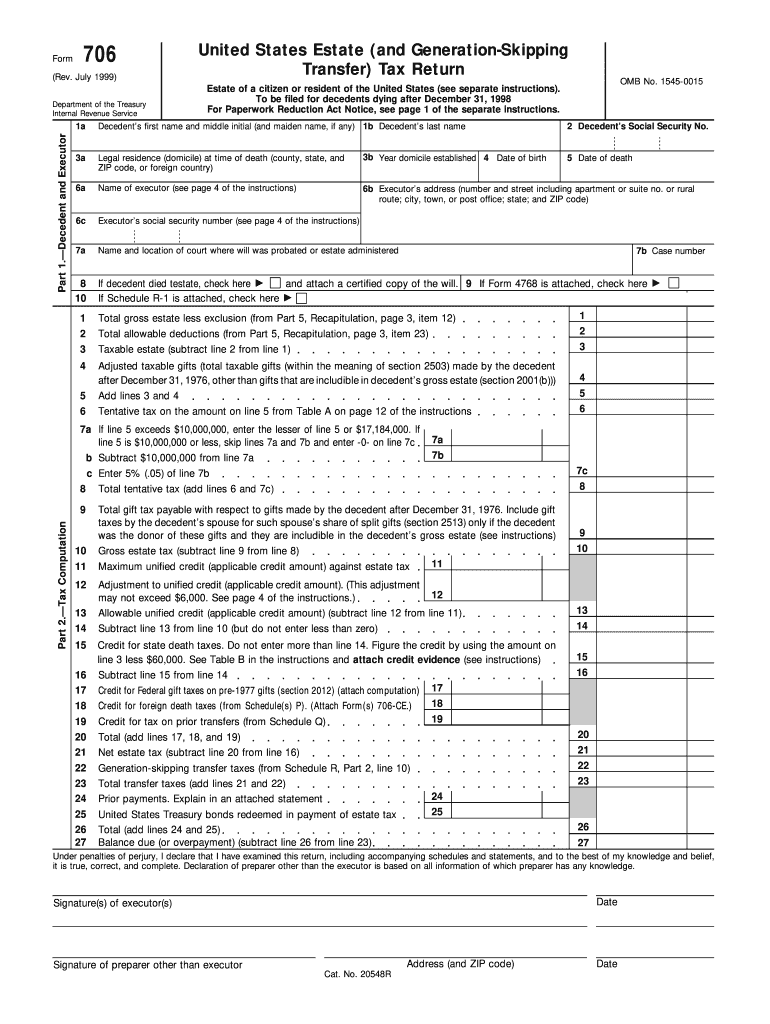

Form 706, also known as the United States Estate (and Generation-Skipping Transfer) Tax Return, is designed to report and calculate the estate tax obligations of decedents who passed away after December 31, 1998. This form is pivotal in documenting the financial particulars of the deceased individual’s estate, allowing the Internal Revenue Service (IRS) to assess and levy taxes where applicable. The document captures various financial details, including the valuation of the gross estate, deductions, and any taxes due on transfers to beneficiaries. Understanding the form's purpose is essential for executors handling estate matters in compliance with federal tax laws.

How to Use the 1999 Form 706

To utilize Form 706 effectively, executors must gather the decedent’s comprehensive financial information, including assets, liabilities, and previous tax filings. The form involves entering these details accurately to report the total gross estate and determine any estate tax liabilities. The executor should ensure that the form reflects all legal deductions and credits available to the estate, such as marital and charitable deductions. Use of the form requires careful adherence to IRS guidelines, making it prudent to consult with a tax professional if complexities arise.

Steps to Complete the 1999 Form 706

-

Collect Necessary Documents:

- Gather all pertinent financial records, including valuations of real estate, stocks, bonds, business interests, and personal property.

- Obtain prior tax returns and pertinent legal documents.

-

Calculate Gross Estate:

- Input valuations of all estate assets to determine the gross estate total.

- Include all tangible and intangible assets, financial holdings, and property interests.

-

Deduct Applicable Expenses:

- Subtract funeral expenses, debts, administrative expenses, and allowable deductions.

- Calculate any spousal transfers to apply marital deductions.

-

Complete Required Schedules:

- Fill out applicable schedules detailing specific asset categories and financial interests.

-

Determine Tax Obligations:

- Utilize the provided worksheets and tax tables to calculate the amount of estate tax due.

-

Submit the Form to the IRS:

- File the completed form with the IRS, ensuring that all sections are properly filled and supporting documentation is attached.

Key Elements of the 1999 Form 706

Form 706 includes several critical sections designed to capture a full snapshot of the decedent's financial standing:

- Gross Estate Valuation: Encompasses all property and assets owned at death.

- Deductions: Categories for marital, charitable, and other permissible deductions.

- Tax Computation: Detailed steps to assess the federal estate tax liabilities.

- Schedules: Required attachments detailing asset types and valuations (e.g., Schedule A for real estate, Schedule B for securities).

Important Terms Related to the 1999 Form 706

- Gross Estate: Total value of all assets and properties owned by the deceased.

- Taxable Estate: The net estate value after deductions used to calculate tax obligations.

- Unified Tax Credit: A credit that can reduce the amount of estate tax owed.

- Executor: The individual appointed to manage the deceased’s estate and ensure proper tax filings.

Required Documents for Filing the 1999 Form 706

A comprehensive list of documents supports the accuracy and completeness of Form 706:

- Valuation Records: Appraisals and valuations for real property and estate assets.

- Debts and Obligations: Documentation listing outstanding liabilities and debts.

- Prior Tax Returns: Federal tax returns from prior years for consistency checks.

- Certificates of Title: Proof of ownership for properties and vehicles.

- Legal Documents: The decedent’s will, trusts, and any relevant legal contracts or agreements.

Filing Deadlines and Important Dates

The completion and submission of Form 706 are subject to strict timing rules:

- Filing Deadline: Typically due nine months after the decedent’s date of death.

- Extension Requests: Extensions are available through Form 4768, providing additional time to file.

Penalties for Non-Compliance

Non-compliance with Form 706 requirements can have significant consequences:

- Late Filing Penalties: Penalties apply if the form is not filed by the deadline, calculated as a percentage of the owed tax.

- Accuracy-Related Penalties: Additional fines may be imposed for errors, omissions, or fraud in the submitted forms.

- Interest on Unpaid Taxes: Interest accrues on any underpaid or outstanding tax amounts due to the IRS after the filing date.