Definition & Function of Form 706

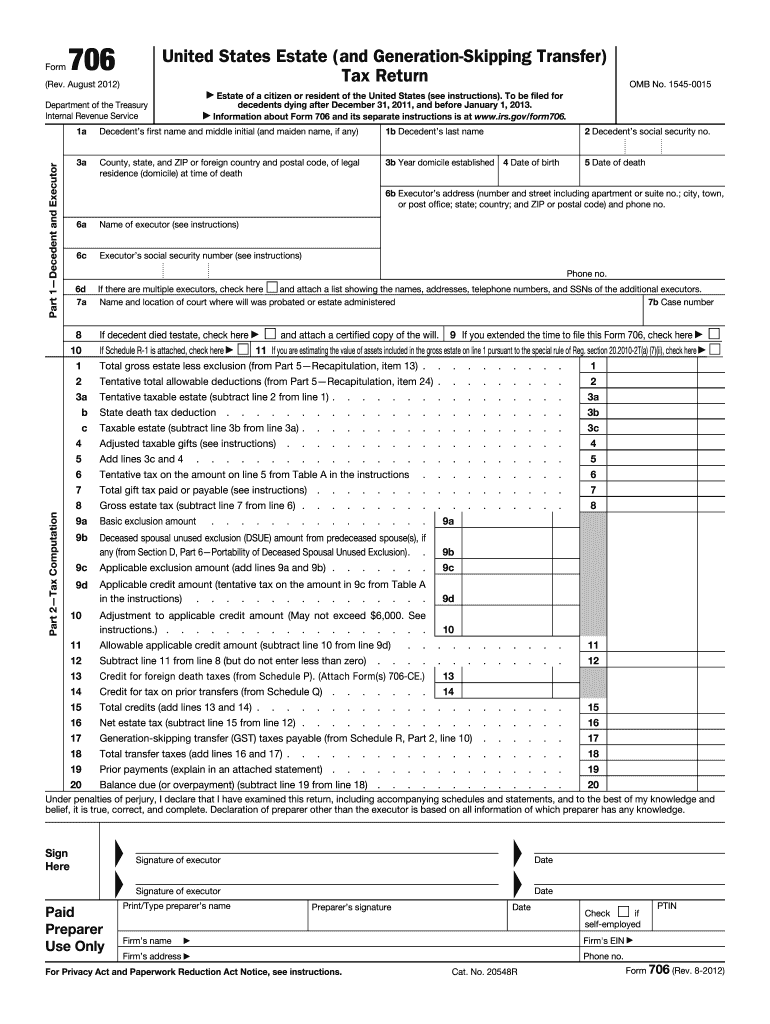

Form 706, officially known as the United States Estate (and Generation-Skipping Transfer) Tax Return, is primarily used by estates to calculate the federal estate tax owed for a decedent who passed away between December 31, 2011, and January 1, 2013. This form reports the estate's total value at the time of death, applicable deductions, and computes the resulting estate tax due. It's crucial for executors managing the legal and tax responsibilities of an estate, especially when significant assets are involved.

Steps to Complete Form 706

Filing Form 706 requires a detailed approach to ensure accurate representation of the estate’s financial status. Here are the essential steps:

-

Identify the Decedent's Information: Include the decedent’s full name, Social Security number, and date of death.

-

Determine the Gross Estate: Calculate the total value of all assets owned, including real estate, investments, bank accounts, and life insurance policies.

-

Account for Deductions: Deduct expenses like funeral costs, debts, mortgages, and estate administration fees.

-

Compute the Tax Due: Use the value derived from steps two and three to determine the taxable estate and compute any estate taxes owed.

-

Elect Portability: If applicable, decide whether to elect portability of any deceased spousal unused exclusion (DSUE) amount.

-

Attach Required Documentation: Ensure all supporting documentation is included before submission.

Required Documents for Form 706

To file Form 706, ensure you have the following essential documents:

- Official death certificate

- List of assets and corresponding appraisals or valuations

- Previous gift tax returns, if applicable

- Copies of the decedent's will or trust documents

- Detailed list of debts and obligations

These documents support the values and deductions reported on the form, aiding in accurate tax calculation.

Who Typically Uses Form 706?

Form 706 is generally used by executors or legal representatives of an estate. It is particularly applicable for estates where the total value exceeds the federal exemption limit at the time of the decedent's death. Executors must ensure compliance with filing requirements to avoid penalties and safeguard beneficiaries' interests.

Legal Implications of Form 706

Completing Form 706 ensures compliance with federal estate tax laws applicable to the decedent's financial estate. It allows the IRS to identify taxable estates and collect due taxes, enforcing legal obligations tied to posthumous asset transfers and wealth transition. Misreporting or failure to file can lead to significant legal repercussions, including penalties and interest on unpaid taxes.

Important Terms Related to Form 706

Understanding the terminology associated with Form 706 is crucial:

- Gross Estate: Total value of all property interests held by the decedent at death.

- Deductions: Allowable reductions from the gross estate, such as debts and expenses.

- Taxable Estate: Net value subject to estate tax after deductions.

- Deceased Spousal Unused Exclusion (DSUE): Portion of a deceased spouse's exemption that can be transferred to the surviving spouse.

- Portability Election: Option to transfer DSUE to the surviving spouse.

These terms are integral to understanding the form's requirements and implications.

IRS Guidelines for Form 706

The IRS provides specific guidelines for filing Form 706, emphasizing precise valuation of assets and deductions. Executors should reference IRS instructions for each schedule within the form to ensure accurate completion. Regular updates to tax laws may affect filing thresholds and exemptions, so staying informed of IRS publications is beneficial.

Filing Deadlines for Form 706

Form 706 must be filed within nine months following the decedent's date of death, though executors can request a six-month extension. Timeliness is critical to avoid penalties. An extension, however, does not delay the time for payment of taxes due, which remains at the original deadline.