Definition and Purpose of Form 706

Form 706, officially known as the United States Estate (and Generation-Skipping Transfer) Tax Return, is used to determine the estate tax liability of deceased individuals with estates surpassing the federal estate tax exemption threshold. Relevant for estates of individuals who passed away after December 31, 2012, it serves a critical role in reporting the fair market value of the decedent's assets. It includes a comprehensive evaluation of various components, such as bank accounts, real estate, and closely held businesses, to determine the correct tax liability. The form also facilitates the portability election, allowing a surviving spouse to apply the deceased spousal unused exclusion (DSUE) amount to their future estate and gift tax returns.

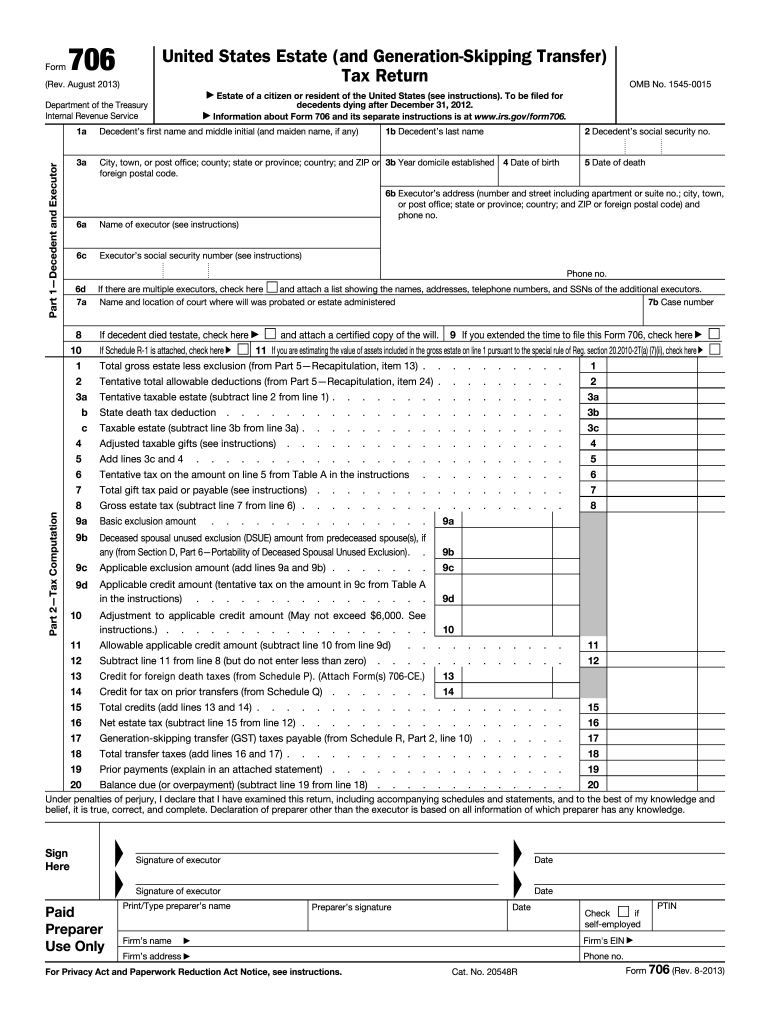

Key Components of Form 706

Completing Form 706 involves several important sections that require detailed information:

- Decedent and Executor Information: This section captures the personal details of the decedent, including their Social Security number and the executor’s contact information.

- Gross Estate Calculations: It demands a precise calculation of the estate's value, encompassing property values at the time of death or, alternatively, six months later using the alternate valuation date.

- Deductions and Tax Computations: Outlining allowed deductions, such as funeral expenses, debts, and qualified charitable bequests, helps determine the taxable estate.

- Portability Election: This optional section is crucial for executors wishing to elect portability of the DSUE to the surviving spouse.

- Schedule Listings: Detailed asset and deduction schedules, like Schedule A for real estate and Schedule B for stocks and bonds, provide transparency and completeness in the tax reporting process.

Steps to Complete Form 706

Completing Form 706 requires careful attention to detail. Follow these steps to ensure accuracy:

- Gather Necessary Documents: Collect all pertinent records, including death certificates, property appraisals, and financial statements.

- Accurate Valuation: Determine the fair market value of all assets from the estate and account for any liabilities.

- Deduction Calculation: Identify and compute all applicable deductions to reduce the estate’s taxable value.

- Complete Relevant Schedules: Fill in all applicable schedules to provide a detailed account of assets and liabilities.

- Elect Portability, if applicable: Make the portability election on part six if desiring to transfer the DSUE to the surviving spouse.

- Review and Submit: Double-check for accuracy before submitting the form to the IRS by the respective due date.

Who Uses Form 706

Form 706 is primarily used by the executors of estates of deceased individuals in instances where the estate's value exceeds the federal exemption threshold. Executors, often family members or estate attorneys, complete the form not only to comply with federal tax regulations but also to efficiently manage the deceased’s financial legacy. It is especially relevant when involving more complex estates with multiple asset types or significant liabilities, ensuring all components are considered in the estate valuation process.

IRS Guidelines and Filing Deadlines

The IRS mandates that Form 706 be filed nine months after the decedent's death. An extension of six months can be requested by submitting Form 4768. It is imperative to adhere to these deadlines to avoid penalties and interest on underpaid taxes. The IRS provides a comprehensive set of instructions for completing Form 706, which outlines specific rules for asset valuation, filing procedures, and what documentation is required.

Required Documents for Submission

When submitting Form 706, executors need to include several essential documents:

- Certified Death Certificate: To verify the date of death.

- Will and Trust Documents: Relevant for outlining the disposition of the estate.

- Real Estate Appraisals: Necessary for accurately valuing property included in the estate.

- Financial Account Statements: Including details and balances for all financial instruments.

- Appraisals for High-Value Items: Such as jewelry or artwork, for appropriate valuation in the gross estate total.

Form Variants and State-Specific Differences

While Form 706 is standardized at the federal level, certain states have additional estate or inheritance tax return forms. Executors should verify state-specific requirements, as states like New York and New Jersey have unique forms for state-level estate tax reporting. These forms often mirror the federal process but contain state-specific thresholds, rates, and deductions that can affect the overall tax strategy.

Penalties for Non-Compliance

Failure to file Form 706 on time or incorrect filing can lead to significant penalties. The IRS may impose late filing penalties, which could amount to 5% of the tax due per month, up to 25%. There are also potential accuracy-related penalties if there is a substantial understatement of estate tax due to negligence or ignorance of tax laws. Therefore, accuracy and punctuality are critical in estate tax administration to minimize financial risks and ensure compliance with regulations.