Definition and Meaning

A Certificate of Liability Insurance is an official document that provides evidence that an individual or company has coverage under a liability insurance policy. This certificate does not modify the insurance contract; it merely provides proof that the insured party has active coverage. It outlines crucial information such as the insured party's name, the insurance company, policy numbers, coverage limits, and effective dates. This document is often used in business transactions to assure third parties—such as clients, partners, or regulatory bodies—that appropriate and adequate insurance coverage is in place.

How to Use the Certificate of Liability Insurance

The Certificate of Liability Insurance is primarily used to demonstrate the existence of an active liability policy to third parties who may request it. Businesses often provide this certificate to clients and partners to fulfill contractual obligations. For example, a construction firm might need to submit this certificate to a client to verify that liability coverage is active before commencing a project. Similarly, consultants or freelancers might provide this certificate to ensure compliance with client requirements. The certificate can also assist in risk assessment processes, allowing other parties to determine the adequacy of the coverage for specific risks associated with contracts or projects.

How to Obtain the Certificate of Liability Insurance

To obtain a Certificate of Liability Insurance, the insured party must contact their insurance provider or insurance agent. Typically, these certificates are issued at no extra cost. The process involves:

- Contacting the insurance provider or agent.

- Requesting the certificate, specifying necessary details such as the name of the party requiring the certificate and any specific information they require.

- Reviewing the issued certificate to ensure accuracy and completeness, including the correct coverage amounts and policy details.

- Providing the certificate to the requesting third party or entity.

Timeliness is crucial, as many business transactions cannot proceed without this documentation.

Steps to Complete the Certificate of Liability Insurance

While insurance policyholders typically do not complete the Certificate of Liability Insurance themselves, understanding the process can be useful. Insurance companies or agents usually fill out the form, ensuring all information aligns with the actual policy. Steps include:

- Gathering all necessary policy details, including policy number, coverage types, and limits.

- Accurately completing the form with this information, ensuring consistency with the policy terms.

- Including any additional insured parties if required by the certificate holder.

- Reviewing the completed certificate for accuracy.

- Issuing the certificate to the requesting party, maintaining a record for future reference.

Why the Certificate of Liability Insurance is Important

The Certificate of Liability Insurance is critical in business operations as it verifies that a company or individual holds insurance that can cover claims of third-party bodily injury or property damage. It helps manage risks by ensuring that contractual partners maintain adequate insurance coverage to protect against potential liabilities. This certificate is pivotal in building trust with clients and partners, as it reassures them that in the event of an incident, there are resources to cover damages or losses, thus safeguarding both parties' financial interests.

Who Typically Uses the Certificate of Liability Insurance

The Certificate of Liability Insurance is commonly used across various industries including construction, real estate, and professional services. Contractors, vendors, freelancers, and consulting firms frequently use it to prove that they meet the insurance requirements stipulated in contractual agreements. Clients, property owners, and regulatory bodies may request these certificates as part of their due diligence processes, requiring proof that service providers or businesses engaged in activities on their behalf are properly insured against liabilities.

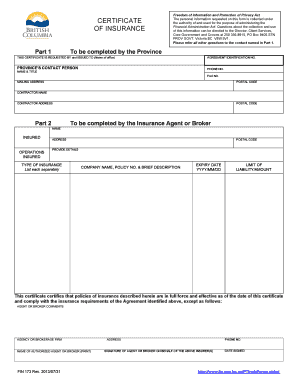

Key Elements of the Certificate of Liability Insurance

The Certificate of Liability Insurance contains several key elements:

- Insured Party Details: Information about the entity or individual covered by the insurance policy.

- Insurer Information: Details about the insurance company providing the coverage.

- Policy Numbers and Types: Identifiers for the specific policies and the type of liability insurance (e.g., general liability, automobile liability).

- Coverage Limits: The maximum amount the policy will pay under covered claims.

- Effective Dates: Start and end dates showing the period the coverage is valid.

- Additional Insureds: Parties, beyond the primary insured, who are also covered under the policy.

These elements ensure that every party reviewing the certificate can understand the scope and limitations of the coverage provided.

State-Specific Rules for the Certificate of Liability Insurance

Each U.S. state may impose specific requirements or standards regarding liability insurance, influencing what must be detailed on the certificate. In some states, certain endorsements or policy adjustments may be mandatory, affecting coverage or certificate language. For example, construction projects in states like California may require particular clauses or additional insured endorsements. Therefore, it is vital for insurance providers and policyholders to familiarize themselves with state-specific regulations to ensure their certificates comply with all applicable local laws and industry standards.

Examples of Using the Certificate of Liability Insurance

Several real-world scenarios illustrate how the Certificate of Liability Insurance is used:

- Contractors and Construction Firms: A contractor submits a certificate to a property developer to confirm they have sufficient liability coverage before starting a commercial building project.

- Event Planners: An event organizer provides a certificate to a venue owner to show they are insured against potential event-related damages.

- Consultants: A consultant sends a certificate to a corporate client to verify that they have professional liability insurance covering their advisory services.

These examples demonstrate how certificates facilitate business transactions by mitigating risk and building trust through verified insurance coverage.