Definition and Meaning of the Family Loan Agreement

The Family Loan Agreement is a legally binding contract between family members to outline the terms of a loan. Typically, these agreements are used to avoid misunderstandings and ensure clarity regarding repayments and interest rates. Unlike informal verbal agreements, a written family loan agreement includes detailed terms such as repayment schedules, interest due, and obligations of both the lender and borrower. This formal document helps maintain harmonious relationships by setting clear expectations and preventing potential disputes.

How to Use the Family Loan Agreement

Using the Family Loan Agreement involves several essential steps to ensure its effectiveness. Firstly, the lender and borrower should have a detailed discussion about the loan's terms. It's crucial to document these terms explicitly in the agreement. Include specifics such as loan amount, interest rate, repayment schedule, and any late payment penalties. Additionally, both parties should review the document to confirm all information is accurate. Once agreed upon, both lender and borrower should sign the document to make it legally enforceable. Storing a copy in a safe location for future reference is recommended for both parties.

Important Terms Related to Family Loan Agreement

Understanding key terms related to the Family Loan Agreement is vital for its proper execution. Terms such as "principal amount" refer to the initial loan amount. "Interest rate" indicates the percentage charged for borrowing. "Maturity date" is when the loan must be fully repaid. Terms like "default" describe the borrower's failure to meet repayment obligations. Familiarity with these terms ensures both parties are informed about their responsibilities and the agreement's stipulations.

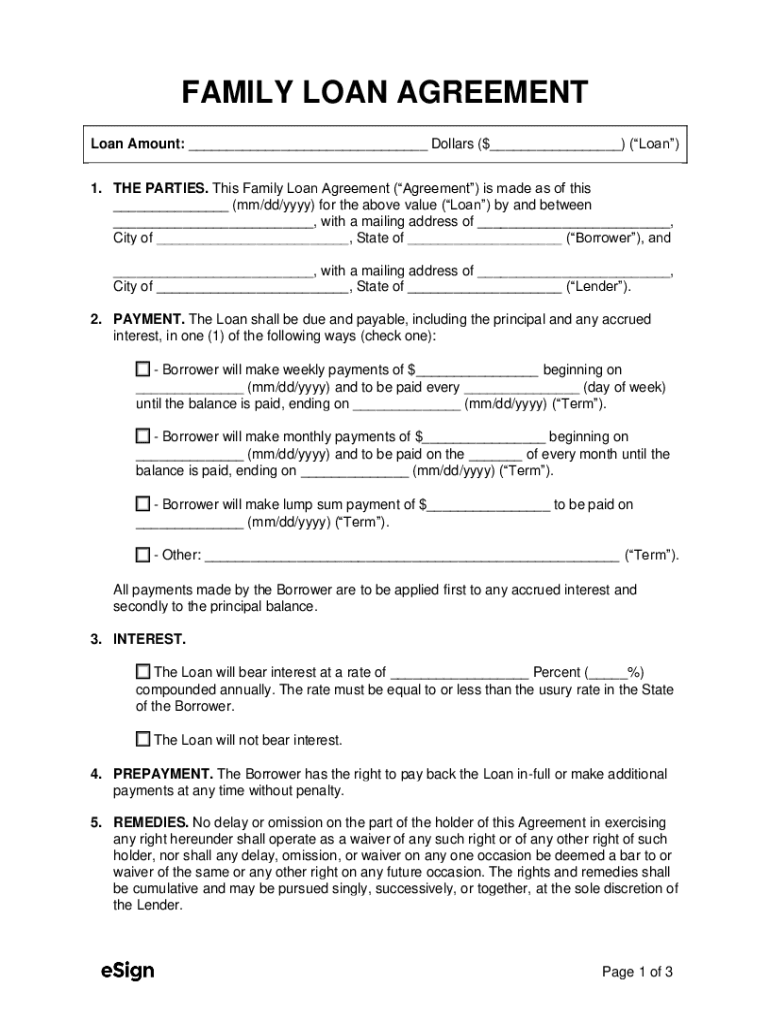

Key Elements of the Family Loan Agreement

Several critical elements must be included in any Family Loan Agreement to enhance its clarity and enforceability. These elements encompass the loan amount, interest rate, repayment schedule, and any applicable fees. A clear description of penalties for late payments and a default clause should also be included. Additionally, specifying whether the loan is secured or unsecured and, if secured, detailing the collateral can protect both parties' interests. Each element must be described in detail to ensure there is no room for ambiguity.

Steps to Complete the Family Loan Agreement

- Negotiation: Begin with a detailed discussion between the borrower and lender to outline the loan terms.

- Drafting: Use precise language to draft the agreement, incorporating all agreed-upon terms such as amounts, dates, and rates.

- Review: Both parties should thoroughly review the agreement for accuracy and completeness.

- Signatures: Once finalized, the agreement must be signed by both parties to become legally binding.

- Witness: Although not always necessary, having a third-party witness can add an extra layer of validity.

- Filing: Store signed copies securely with each party retaining a copy for reference.

Legal Use of the Family Loan Agreement

The legal enforceability of a Family Loan Agreement provides protection and structure for informal loans between family members. By documenting the transaction, the agreement can be used in legal settings to resolve disputes. It serves as evidence of both parties' intentions and obligations, minimizing ambiguity. Furthermore, incorporating state-specific lending laws ensures the agreement complies with applicable legal standards, further solidifying its legitimacy.

State-Specific Rules for the Family Loan Agreement

Different states may have specific rules or guidelines concerning interest rates and terms that can apply to family loans. It's important to understand the usury laws in your state as these dictate the maximum interest rate allowable. Some states require notarization or additional legal formalities for certain loan amounts. Reviewing your state's specific requirements will ensure the Family Loan Agreement complies with local regulations and avoids potential legal complications.

Examples of Using the Family Loan Agreement

A Family Loan Agreement can prove beneficial in various scenarios. For instance, parents lending money to a child for purchasing a home often use the agreement to establish repayment terms formally. Similarly, siblings might use the agreement when one lends to another for business capital. These examples highlight the agreement's flexibility in ensuring clear expectations are set, fostering trust while safeguarding financial accountability in familial settings.

IRS Guidelines Related to the Family Loan Agreement

The IRS has specific guidelines for loans provided within families, particularly concerning "below-market loans." If a family loan charges no interest or an interest rate lower than the IRS's Applicable Federal Rate (AFR), it may be deemed a gift, subject to federal gift taxes. It is crucial to familiarize oneself with these guidelines to ensure compliance and avoid undesirable tax implications. Consulting with a tax professional can guide the proper structuring of the loan under IRS rules.