Definition and Meaning

The form "U.S. Citizens and Resident Aliens AbroadInternal Revenue" refers to the tax obligations and special provisions for American citizens and resident aliens who are living and working overseas. The form typically aids taxpayers in reporting their global income to the Internal Revenue Service (IRS) and may include provisions for claiming exclusions or credits like the foreign earned income exclusion or housing expense exclusion. It is essential for ensuring compliance with the U.S. tax system, which taxes citizens on worldwide income regardless of residency.

How to Use the Form

To successfully utilize the "U.S. Citizens and Resident Aliens AbroadInternal Revenue," taxpayers must first gather comprehensive records of all foreign income and any eligible deductions or exclusions. The form serves as a conduit through which taxpayers can report income, claim deductions, and provide proof of their foreign housing expenses if applicable. Properly utilizing this form is crucial for minimizing tax liability while adhering to IRS requirements.

Steps to Complete the Form

-

Gather Documentation: Collect all W-2 forms, 1099 forms, and foreign income statements to accurately fill out the form.

-

Determine Eligibility for Exclusions: Assess eligibility for foreign earned income exclusion or housing deduction.

-

Calculate Total Foreign Income: Sum up all income sources from foreign employment.

-

Fill Out Income Sections: Enter the calculated foreign income in the designated sections.

-

Claim Deductions: Enter eligible housing deductions or exclusions.

-

Attach Necessary Schedules: Include any required schedules, such as Schedule B for interest and dividend income.

-

Review and Submit: Check for accuracy and submit the form by the stipulated deadline, either electronically or by mail.

Important Terms Related to the Form

- Foreign Earned Income Exclusion (FEIE): Allows eligible taxpayers to exclude a certain amount of their foreign earnings from U.S. taxation.

- Housing Deduction: A deduction for housing costs incurred overseas, which may reduce taxable income.

- Bona Fide Resident Test: Criteria used to determine a taxpayer's residency status abroad for the purpose of claiming tax exclusions.

- Physical Presence Test: Requirement that taxpayers must be physically present in a foreign country for 330 full days during any 12-month period to qualify for exclusions.

IRS Guidelines

The IRS provides detailed guidelines about who qualifies for tax exclusions under the "U.S. Citizens and Resident Aliens AbroadInternal Revenue" provisions. It is imperative for taxpayers to closely read the IRS instructions pertaining to various tests used for exclusion qualification. Furthermore, taxpayers should use IRS publications, such as Publication 54, to understand their reporting obligations and leverage available exclusions and credits optimally.

Filing Deadlines and Important Dates

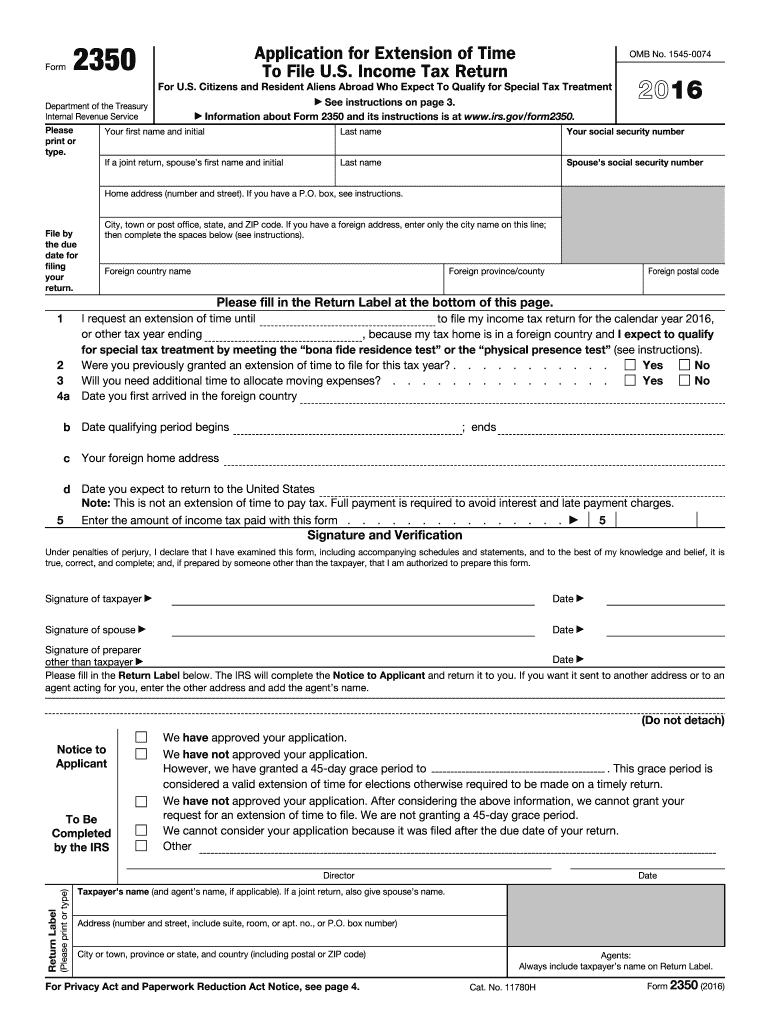

The regular filing deadline for Americans living abroad is typically set on June 15, giving expatriates an automatic two-month extension beyond the standard April 15 deadline in case they need additional time to gather foreign income details. However, any taxes owed must still be paid by April 15 to avoid interest charges. Further extensions are available, but they require filing Form 2350, which allows additional time to meet exclusion criteria.

Required Documents

To complete the "U.S. Citizens and Resident Aliens AbroadInternal Revenue" form, essential documents include employment income records (W-2, 1099), proof of foreign residency or physical presence, and housing expense records. These documents support claims made on the tax return regarding income, presence abroad, and eligibility for exclusions.

Penalties for Non-Compliance

Failure to comply with the requirements of the "U.S. Citizens and Resident Aliens AbroadInternal Revenue" can result in penalties, including fines, accrued interest on unpaid taxes, and potentially losing eligibility for beneficial exclusions or credits. Taxpayers can avoid such penalties by filing accurately and on time, keeping thorough records of all claimed deductions and exclusions, and where necessary, seeking professional tax advice.

Digital vs. Paper Version

The form can be completed in a digital format using tax software compatible with IRS systems, ensuring calculations are handled accurately. Alternatively, paper versions are still accepted for submission. Digital submissions are often more efficient due to built-in accuracy checks and immediate filing confirmation. Both options require the same diligent attention to detail to ensure accuracy in reported information.