Understanding the NYC-114 7 Form

The NYC-114 7 is a specialized tax form used by partners in partnerships to claim a credit against their Unincorporated Business Tax (UBT) liability. This form plays a crucial role in ensuring that businesses operating as partnerships within New York City can optimize their tax obligations effectively.

Purpose and Utility

The NYC-114 7 form is designed to facilitate the calculation and application of the UBT Paid Credit. By using this form, partners in partnerships can accurately report their distributive shares and guaranteed payments, which are essential for determining the exact credit amount applicable against their UBT liability. This structured approach ensures compliance with local tax regulations and helps in minimizing the potential for errors that could lead to financial penalties.

Steps to Complete the NYC-114 7 Form

Completing the NYC-114 7 requires attention to detail and a thorough understanding of the associated instructions and schedules. Here's a step-by-step guide to ensure that the form is filled out accurately:

- Gather Required Information: Before starting, collect all necessary documents, including partnership agreements and records of distributed income.

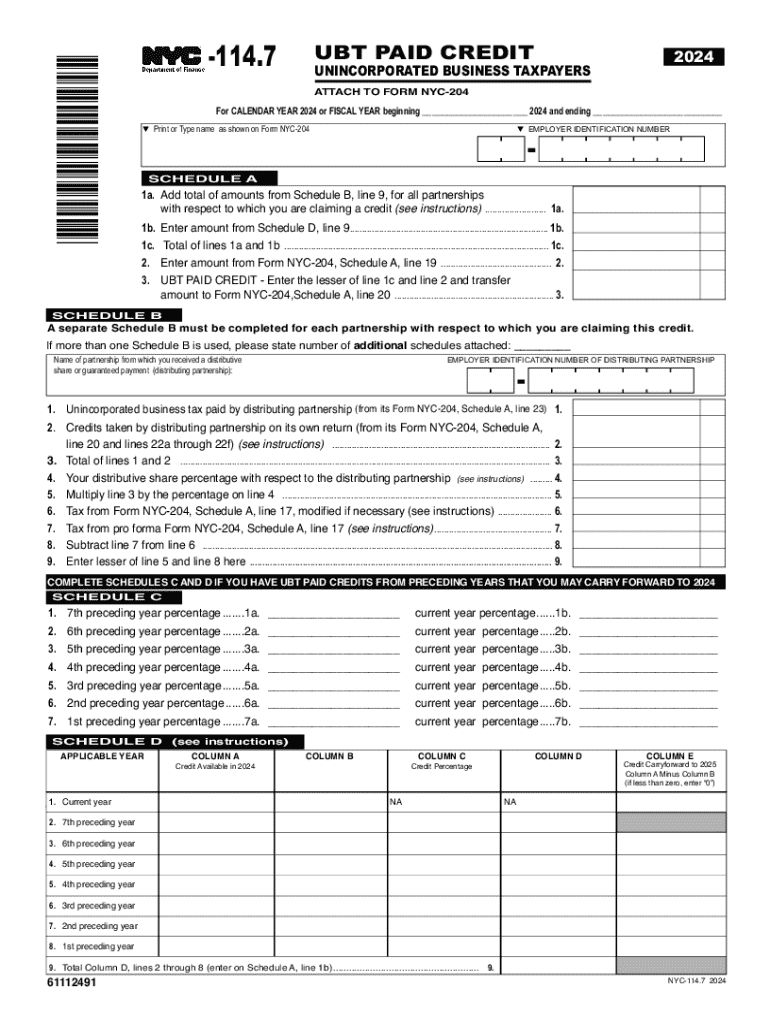

- Complete Schedules A-D: Each schedule requires specific details:

- Schedule A: Report distributive shares, ensuring that all income is accounted for properly.

- Schedule B: Detail guaranteed payments made to partners.

- Schedule C: Calculate total income and deductions.

- Schedule D: Summarize the credits and calculate the total UBT credit.

- Verify Calculations: Double-check all entered data and calculations to verify accuracy.

- Submit the Form: Once completed, review the form for errors before submission. Ensure that deadlines are met to avoid penalties.

Common Mistakes to Avoid

- Miscalculating distributive shares, which can lead to incorrect credit claims.

- Omitting any schedule, as each is integral to the overall calculation.

- Missing the filing deadline, resulting in potential late fees or penalties.

Essential Terms and Legal Considerations

Key Terms

- Distributive Shares: The portion of income or loss allocated to each partner in a partnership.

- Guaranteed Payments: Fixed payments made to partners, which must be reported accurately.

Legal Implications

Using the NYC-114 7 form incorrectly can result in penalties. It's crucial that each item on the form is substantiated with factual and verifiable data to withstand any potential audit by tax authorities. Partnerships should maintain comprehensive records to support all entries made on the form.

Practical Examples and Real-World Scenarios

Example 1: Small Business Partnership

A small business operating as a partnership in NYC needs to determine each partner's UBT liability. By thoroughly completing the NYC-114 7, they manage to correctly allocate distributive shares and guarantee payments, maximizing their available credits and minimizing taxes owed.

Example 2: Complex Partnerships

Consider a large consultancy firm with multiple partners, each having different profit-sharing ratios. The NYC-114 7 allows clear articulation of each partner’s share and ensures that all credits are appropriately calculated, avoiding potential conflicts or errors in tax filings.

Integration with Software

While the NYC-114 7 is a paper form, many software programs like QuickBooks and TurboTax may help track distributive shares and guaranteed payments, streamlining the process of completing the form manually. This integration facilitates easier tracking and ensures accuracy, reducing the likelihood of errors.

Compliance and Penalties

Important Deadlines

Adhering to deadlines for the NYC-114 7 is essential. Late submissions can lead to penalties that exacerbate the tax burden on partnerships. Ensure timely filing to benefit fully from the UBT Paid Credit.

Penalties for Non-Compliance

Failing to properly file the NYC-114 7 could attract financial penalties, additional interest on late payments, and increased scrutiny from tax authorities. To avoid these consequences, partnerships should have a proactive approach towards tax compliance, including regular audits and consultation with tax professionals when necessary.