Definition and Meaning

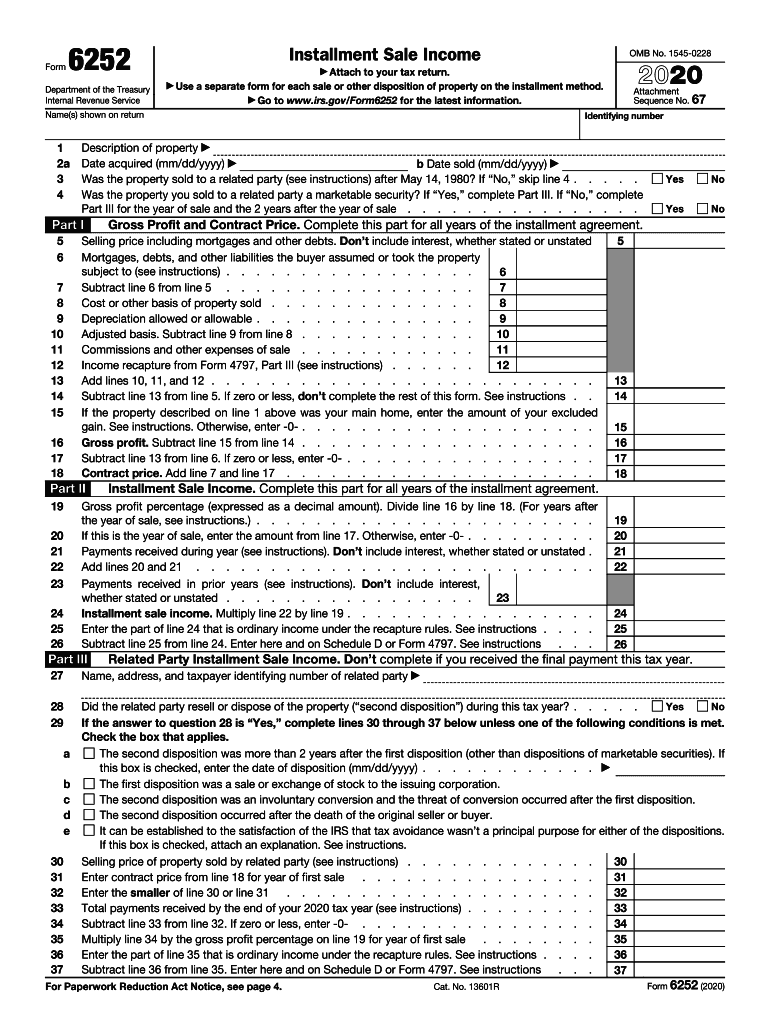

Form 6252, "Installment Sale Income," is a tax form used to report income from installment sales where at least one payment is received after the tax year of the sale. The IRS requires this form to report details such as the gross profit from the sale, the contract price, and total payments received during the year. It's crucial for taxpayers engaging in installment sales, providing a structured way to spread income tax payments over the period the payments are received. This method is beneficial for managing cash flow and tax liabilities effectively over time.

Steps to Complete Form 6252

Completing Form 6252 involves several key steps:

-

Determine Eligibility: Verify if the sale qualifies for installment sale reporting.

-

Fill Out Part I: Calculate the gain and determine the contract price. Include the selling price, adjusted basis, and selling expenses.

-

Fill Out Part II: Report payments received for the current year, including down payments and any payments made towards principal.

-

Calculate Gross Profit Percentage: Determine the percentage by dividing the gross profit by the contract price. This percentage helps in calculating taxable income for each year.

-

Complete Part III: Report interest received, if applicable, which should not be included in the gross profit percentage but reported separately.

-

Review for Accuracy: Double-check all calculations and the entries against supporting documents before submission to avoid errors.

Who Typically Uses Form 6252

Form 6252 is particularly used by taxpayers involved in installment sales. These can include individuals, small business owners, and real estate investors. The form allows sellers to defer a portion of their tax liability until the payments are actually received. By spreading out tax payments, individuals and businesses engaged in large sales, such as real estate transactions, can better manage their income tax obligations across multiple years. This is especially useful in scenarios involving large capital gains.

Important Terms Related to Form 6252

Several critical terms are associated with Form 6252 that users should understand:

- Installment Sale: A sale of property where at least one payment is received after the tax year in which the sale occurs.

- Gross Profit: The total gain realized from the sale, calculated as the selling price minus the adjusted basis and selling expenses.

- Contract Price: The total amount to be received for the property, excluding interest, if any.

- Adjusted Basis: The original cost of the property adjusted for various factors like depreciation and improvements.

- Interest: Any interest earned from the installment sale, which should be reported separately from the installment sale income.

IRS Guidelines

The IRS provides specific guidelines to ensure proper compliance with installment sales. Form 6252 must accurately reflect the taxpayer’s gain and payment terms. The IRS may require verification if the sale appears unfavorable to the tax liability. Detailed record-keeping of all transactions related to the sale is necessary. Taxpayers must adhere to IRS documentation and reporting standards to avoid penalties or audits. The guidelines emphasize accuracy in computing the gross profit percentage and in reporting each year's payments.

Filing Deadlines and Important Dates

Form 6252 must be filed annually with your federal tax return for each year of the installment agreement. The typical deadline is the same as your IRS tax return, usually April 15. If you file for an extension on your federal return using Form 4868, the deadline for Form 6252 would also be extended. Being aware of these timelines is essential to ensure timely submission and avoid late filing penalties, which could include interest charges on unpaid taxes.

Required Documents

When preparing to file Form 6252, you should gather specific documents:

- Sales Contract: Includes details of the property sold and payment schedule.

- Payment Records: Documentation of payments received, including down payments.

- Basis Documents: Evidence of the original purchase price and capital improvements to determine adjusted basis.

- Interest Receipts: If applicable, to separate interest income from principal payments.

These documents ensure accurate reporting and support claims in case the IRS requests further information.

Examples of Using Form 6252

Imagine you sold a property for $100,000 more than the cost basis and received $20,000 upfront. You’d use Form 6252 to recognize only a portion of the gain in the year of sale and defer the rest over the installment payments. Business owners converting large transactions to installment sales can also apply Form 6252. For example, selling a business unit on installments enables cash flow alignment with tax obligations, making Form 6252 a valuable tool for strategic financial planning.

State-Specific Rules for Form 6252

While Form 6252 applies federally, some states might have specific rules. For instance, California requires its equivalent form to be filed along with state tax returns. These variations necessitate understanding both federal and state tax codes for installment sales. Consulting with tax professionals can provide clarity on any unique state filing requirements or variations from federal guidelines, ensuring compliance across different jurisdictions.