Definition and Meaning of Revocation of S-Corporation Election

Revocation of S-Corporation election refers to the process by which a business entity, such as a Limited Liability Company (LLC) or a corporation, formally rescinds its election to be taxed as an S-Corporation. The S-Corporation status allows businesses to pass corporate income, losses, deductions, and credits directly to their shareholders, avoiding double taxation. However, there might be instances where a business finds it advantageous to revoke this status, shifting back to being taxed under C-Corporation rules or other tax classifications. This revocation is a legal and tax procedure recognized by the Internal Revenue Service (IRS), and it involves notifying the IRS of the intent to cancel the existing S-Corporation election.

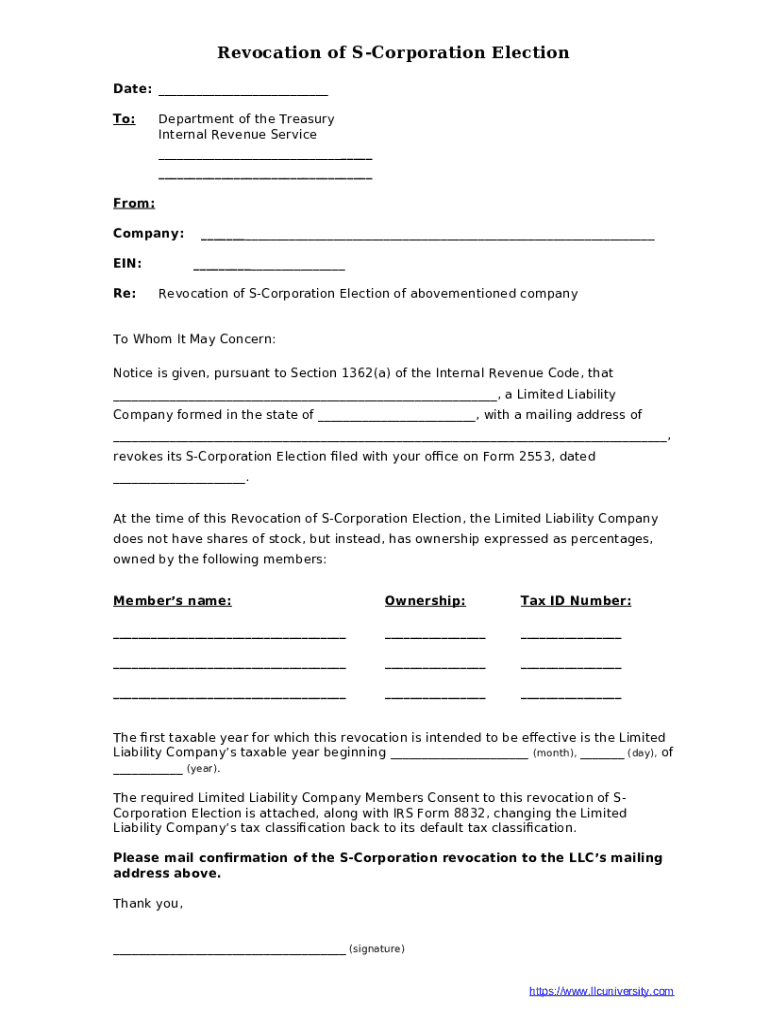

Steps to Complete the Revocation of S-Corporation Election

-

Determine Revocation Eligibility: Before initiating the revocation, ensure that the business is eligible to revoke the S-Corporation status. This often involves confirming that shareholders consent and the timing is in compliance with IRS regulations.

-

Prepare IRS Submission: Draft a formal statement indicating the intent to revoke the S-Corporation election. This document should include the business name, Employer Identification Number (EIN), and a clear declaration of the effective date for the revocation.

-

Gather Shareholder Consent: Collect the written consent of shareholders holding more than fifty percent of the shares on the day of the revocation. This consent is crucial for the IRS to consider the revocation valid.

-

File the Revocation with the IRS: Submit the revocation document to the IRS center where the original S-Corporation election was filed. The timing of the submission is critical, as it affects the fiscal year from which the revocation will take effect.

-

Await IRS Confirmation: After submission, the IRS will review the revocation notice. Businesses should request a confirmation letter to ensure that the revocation is processed and acknowledged correctly.

Why Revoke an S-Corporation Election

There are several reasons why a business might choose to revoke its S-Corporation election:

- Tax Considerations: The business may find that the tax benefits initially anticipated from S-Corporation status are not realized, or a C-Corporation tax structure presents better financial advantages.

- Shareholder Changes: Significant changes in shareholder composition might make it more viable to operate outside the S-Corporation framework.

- Operational Flexibility: Businesses seeking more operational flexibility and fewer restrictions on stock classes may opt to revoke.

IRS Guidelines for Revocation

The IRS outlines specific procedures and guidelines for the revocation of S-Corporation status:

- Timing: The revocation must be submitted before the fifteenth day of the third month of the tax year for it to be effective in that year.

- Documentation: All required documents, including shareholder consents and revocation statements, must be complete and accurate.

- Validity: Ensuring compliance with IRS rules is crucial to maintain the validity of the revocation.

Required Documents for Revocation

To successfully revoke the S-Corporation election, the following documents are typically required:

- A formal revocation statement addressing the IRS.

- Written consents from a majority of the shareholders.

- A copy of the original S-Corporation election (Form 2553) for reference.

Penalties for Non-Compliance

Failure to properly revoke S-Corporation status or submit the required documents can have several repercussions:

- Tax Complications: The business may face unexpected taxation issues or penalties for non-compliance.

- Delayed Status Changes: Incorrect revocation procedures can result in a delay in status changes, affecting tax planning and financial reporting.

Legal Use and Importance

Revocation of S-Corporation election is a strategic decision that should align with the business’s long-term goals and regulatory compliance. Understanding the legal framework ensures that businesses do not inadvertently incur penalties or lose tax advantages. Legal advisement is often recommended to navigate the complexities of tax status changes and to align business operations with financial objectives.