Definition and Purpose of Form 8821

Form 8821, Tax Information Authorization, is a document that enables a taxpayer to authorize an individual or entity to review and receive their confidential tax information from the Internal Revenue Service (IRS). This form is important for individuals who want someone else, such as a tax professional, to access their tax records for various reasons including tax planning or problem resolution. It's crucial to note that this form does not allow the appointed person to act on behalf of the taxpayer with the IRS in any matter. Form 8821 simply serves as a means to facilitate the sharing of information.

How to Use the 2012 Form 8821

To effectively use the 2012 Form 8821, taxpayers must accurately fill out all sections, specifying who is authorized to access their information and what specific tax matters are involved. The form applies to various types of tax information, including income, payroll, and excise taxes. Users should be meticulous in designating the types of tax years or periods covered in the authorization to avoid any misunderstanding. It’s advisable to review each entry for accuracy before submission to ensure the information is correctly recorded and accessible by the appointee.

Steps to Complete the 2012 Form 8821

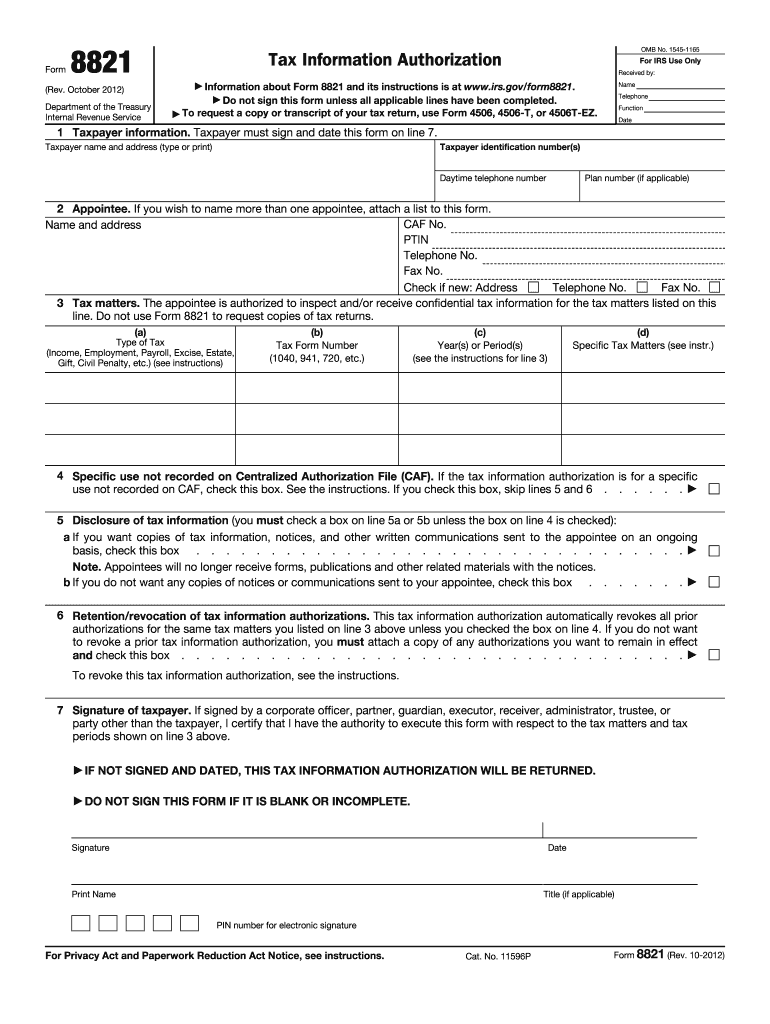

- Taxpayer Information: Fill in your personal information, including your name, address, and taxpayer identification number, at the top of the form.

- Appointee Details: Enter the name and address of the individual or organization you are authorizing to access your information. Include their Taxpayer Identification Number if applicable.

- Tax Matters: Specify the types of tax matters and the periods they cover by listing tax form numbers and the years or periods involved.

- Authorized Acts: Clearly indicate the acts your appointee is authorized to perform. Remember, representation is not allowed under this form.

- Expiration Date: Determine if a specific expiration date is required or if it follows the standard duration of authorization.

- Signature and Date: Sign and date the form. The IRS requires your signature to confirm your consent.

Legal Use of the 2012 Form 8821

Using Form 8821 legally involves complying with IRS regulations regarding the authorization of tax information access. The form must be filed within 120 days of signature to remain valid. It's important not to confuse this form with Form 2848, which authorizes representation before the IRS. Form 8821 is limited solely to the inspection and receipt of tax information, providing a layer of oversight and confidentiality in managing access to sensitive data.

Key Elements of the 2012 Form 8821

- Taxpayer Identification: Essential personal details that uniquely identify the taxpayer.

- Appointee Identification: Contact information for the designated individual or entity authorized to receive the information.

- Tax Matters Specification: Detailed listing of the tax types and periods, including specific form numbers.

- Signature: The form will not be accepted or processed without the taxpayer's signature.

Filing Deadlines and Important Dates

The 2012 Form 8821 has specific deadlines and time frames to keep in mind. It must be filed within 120 days from the date of signing to ensure it is processed by the IRS. Additionally, the taxpayer can choose to establish a specific expiration date for the authorization, which allows for tailored time limits depending on the nature of the agreement between the taxpayer and the appointee.

Form Submission Methods

Submitting Form 8821 can be done through several methods:

- Mail: Send the completed form to the designated IRS processing center address listed on the form instructions.

- Fax: An option for faster delivery, but be sure to follow IRS guidelines regarding fax submissions to prevent loss of sensitive information.

Penalties for Non-Compliance

Failure to comply with the regulations surrounding Form 8821 can lead to potential penalties. Providing inaccurate information or using the form to deceptively share information can result in severe legal consequences. It is the taxpayer's responsibility to ensure that all data on the form is accurate and truthful, safeguarding themselves from unintended breaches of confidential tax data.

Who Issues the Form

The Internal Revenue Service (IRS) is the agency responsible for the issuance and processing of Form 8821. The form can be obtained from the IRS website or ordered directly through IRS service numbers. The IRS maintains the authority for any changes, updates, or recalls regarding the form.