Definition and Purpose of the 2-OID Form

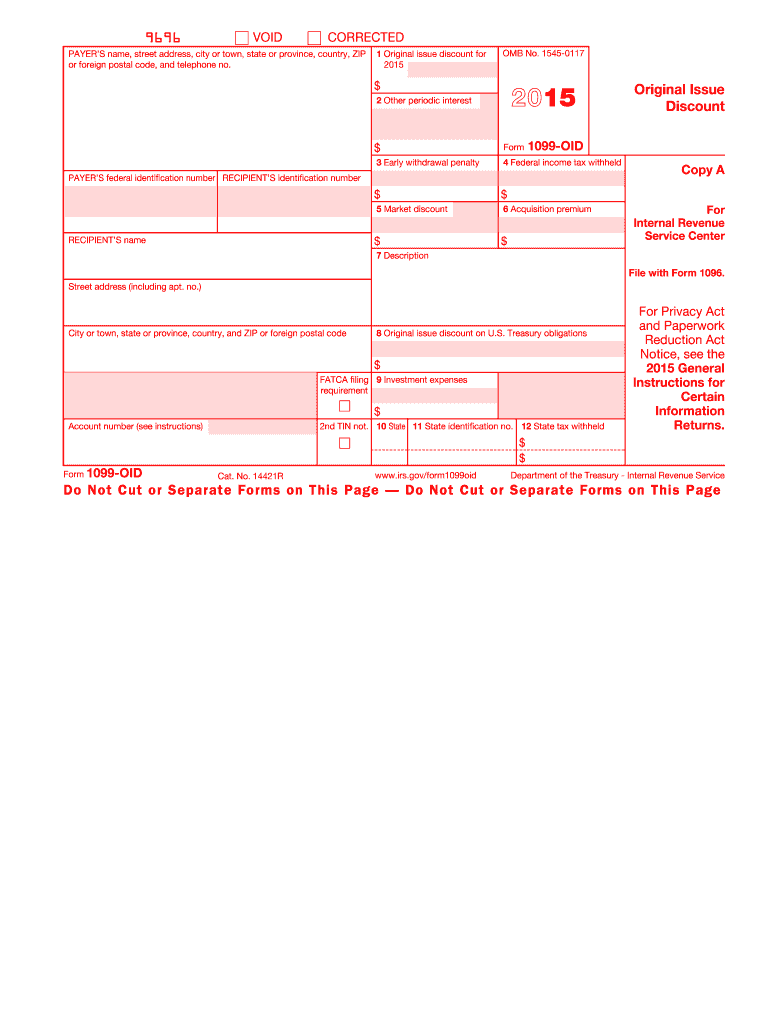

The 2-OID form is a tax document used by payers to report original issue discount (OID) — a type of interest income — to the IRS and taxpayer. This discount arises when a debt instrument, like a bond, is issued at a price lower than its redemption value. The OID form allows taxpayers to report this income on their federal tax returns accurately, ensuring compliance with tax regulations.

Original Issue Discount is considered taxable interest income and must be reported regardless of whether the debt instrument matures. It is essential for individuals and financial institutions handling securities that feature OID to understand this form thoroughly to report accurately and avoid potential penalties.

How to Obtain the 2-OID Form

Taxpayers and financial entities can access the 2-OID form from several sources. The IRS website provides downloadable versions, which can be printed for personal use. Alternatively, individuals can request the form from their financial institution that released the debt instrument with an OID. It is crucial to obtain the official printed version for filing, as online duplicates might not meet IRS scanning requirements.

Those managing investments through a brokerage or other financial service firm will typically receive the 1099-OID form automatically if applicable. This document should be part of the annual tax forms provided to investors.

Steps to Complete the 2-OID Form

-

Gather Necessary Information:

- Ensure you have all the relevant details, including the recipient's name, address, and taxpayer identification number (TIN).

- Collect issuer information if you are completing the form on behalf of a firm.

-

Complete Each Box on the Form:

- Box 1 requires the OID amount that is taxable in the current year.

- Box 2 may include the early withdrawal penalties if applicable.

- Other boxes include acquisition premium and market discount information.

-

Verify and Sign:

- Confirm all entered details for accuracy.

- An authorized individual should sign the form before submission.

Key Elements of the 2-OID Form

- Box 1: Original Issue Discount: This is where the taxable OID amount is reported.

- Box 2: Other Interest: Income other than OID may be reported here.

- Box 8: Bond Premium: Shows the bond premium amortization if applicable.

- Payer and Recipient Details: Ensure names, addresses, and TINs are correctly mentioned.

Every section of the 1099-OID form captures specific financial data, and accurately filling them ensures compliance with IRS requirements.

Filing Deadlines and Important Dates

The IRS mandates specific timelines for submitting the 2-OID form. Generally, these forms must be mailed to the IRS and the recipient by January 31 for paper submissions and March 31 for electronic filings. Adhering to these deadlines avoids late-filing penalties and ensures both the payer and taxpayer report financial details within the tax year accurately.

Penalties for Non-Compliance

Failing to file the 2-OID form or submitting incorrect information can result in substantial penalties from the IRS. The severity of the fines depends on the delay in rectifying the errors — a prompt correction incurs lower charges. Ensuring timely and accurate filing safeguards against financial liabilities.

Who Typically Uses the 2-OID Form

This form is typically used by financial institutions and other entities that issue bonds and other debt instruments carrying an OID. Investors receiving interest income from such securities must accurately report on their tax returns to stay compliant with federal tax obligations.

Businesses issuing OID securities must understand this form's requirements to ensure proper issuance to investors. Individuals holding such investments, even on a small scale, must familiarize themselves with this form for their tax filing needs.

Digital vs. Paper Version of the Form

While both digital and paper submissions of the 2-OID form are acceptable, electronic filing offers several advantages, including confirmation of receipt and faster processing times. Digital forms reduce the risk of errors due to handling and help maintain a comprehensive audit trail. Contrarily, the paper version requires manual handling, which may involve more time and resources. Each taxpayer or issuing entity must determine the most suitable submission method based on their specific circumstances.

Taxpayer Scenarios and Use Cases

- Self-Employed: Independent contractors investing in securities with OID need to report this income.

- Retirees: Those holding municipal bonds or zero-coupon bonds within their retirement accounts.

- Students: Individuals, including students with investment portfolios containing these financial instruments.

Understanding varying scenarios helps in accurately preparing one’s tax return and ensures that all OID income is appropriately reported, maintaining compliance with IRS standards.