Definition and Purpose of Form 8833

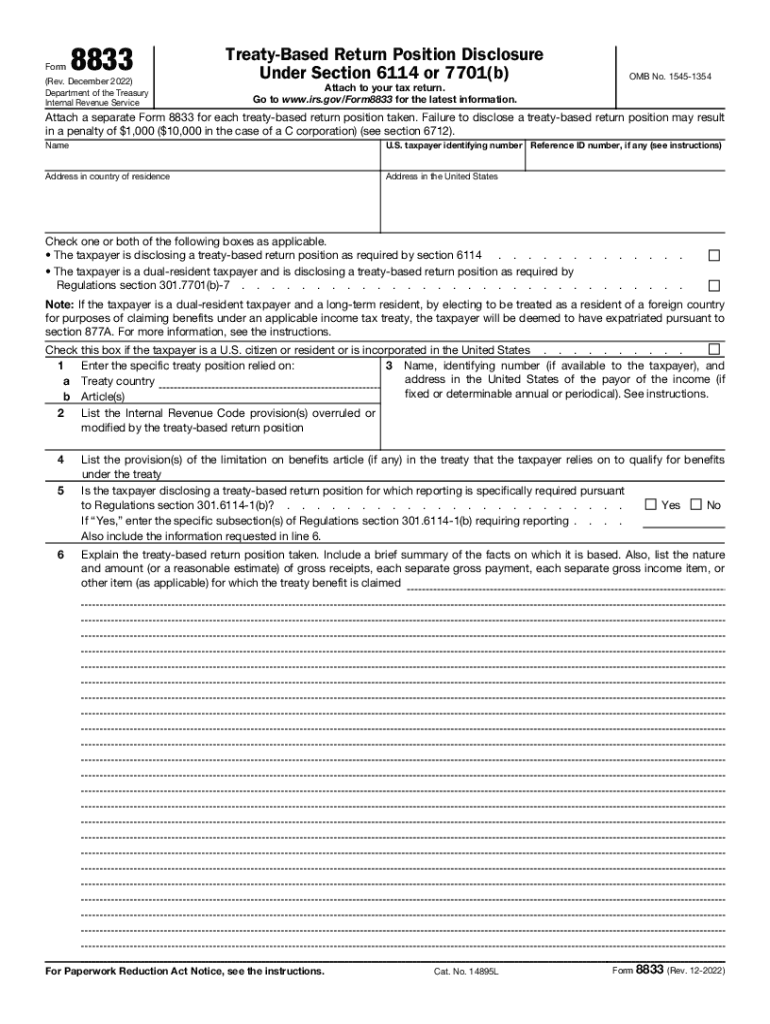

Form 8833 is essential for U.S. taxpayers who wish to disclose treaty-based return positions. It serves two key purposes: compliance with sections 6114 and 7701(b) of the Internal Revenue Code and claiming benefits under international tax treaties. The form is vital for taxpayers and dual-resident taxpayers to communicate their intent to apply certain treaty provisions that could affect their tax obligations in the U.S.

Adhering to this requirement ensures transparency with the IRS regarding the use of treaty provisions. Taxpayers failing to disclose treaty-based positions may face substantial penalties. The form requires a clear articulation of the treaty position being claimed, supporting the legitimacy and accuracy of the submitted tax return.

How to Use Form 8833

Using Form 8833 is crucial for taxpayers who wish to claim either a tax benefit or exclusion based on an international treaty. To use the form, taxpayers must identify applicable treaty articles and detail how these provisions influence their tax obligations. The requirement to attach Form 8833 to the annual tax return makes it a crucial document, ensuring that taxpayers can justify their claims under applicable treaties.

The form must be submitted with the taxpayer's annual return. Detailed explanations, including references to specific treaty articles and sections of the Code that involve treaty positions, are necessary for compliance. Proper use of Form 8833 helps maintain complete and transparent communication with the IRS.

Steps to Complete Form 8833

-

Identify the Treaty and Provisions:

- Determine the specific treaty and articles applicable to your situation.

- Reference the sections of the Internal Revenue Code involved in your treaty claim.

-

Complete Personal Information:

- Fill in general information such as name, address, and taxpayer identification number.

-

Explain the Treaty Position:

- Provide detailed descriptions of the treaty position and its application to your tax situation.

- Explain the effects and implications of the treaty-based return position on your tax obligations.

-

Attach Relevant Documents:

- Include any documentation supporting the treaty position claim, such as agreements or records.

-

Review and Submit:

- Verify accuracy by reviewing all entries.

- Attach the completed Form 8833 to your tax return before submission to the IRS.

Eligibility Criteria

Eligibility to use Form 8833 mainly includes U.S. taxpayers and dual-resident individuals or entities seeking to apply treaty provisions on their tax obligations. To qualify, one must have a specific treaty position affecting tax liability, where claimable benefits exist under a treaty with the United States.

Taxpayers who believe they are exempt from certain U.S. taxes or those seeking reductions because of international treaties may need to file Form 8833. Additionally, dual-resident taxpayers combining U.S. and foreign residency for tax purposes will find the form essential when claiming treaty-defined benefits. Understanding eligibility is crucial for compliance and maximizing available treaty-based benefits.

Key Elements of Form 8833

Form 8833 comprises specific fields that taxpayers must complete:

- Taxpayer Information: Basic personal details and taxpayer identification numbers.

- Treaty Article Details: Specific articles from international treaties that apply to the taxpayer's situation.

- Disclosure of Treaty Position: Clear descriptions of treaty benefits being claimed and their impact.

- Supporting Documentation: Any additional records or documents that support the taxpayer's position.

Each section of the form demands precise and accurate completion to ensure that the IRS can process the treaty position claim effectively. These key elements form the backbone of Form 8833, directly impacting its approval or rejection.

IRS Guidelines

The IRS issues specific guidelines for completing Form 8833, primarily focusing on the accurate reporting of treaty-based positions. These guidelines aim to streamline the disclosure process, ensuring that taxpayers adhere to requirements set by sections 6114 and 7701(b).

The guidelines incorporate instructions on identifying applicable treaties and determining qualification criteria for tax relief based on said treaties. Additionally, the IRS outlines potential penalties for failing to properly complete or submit the form, underscoring the importance of adherence. These guidelines are a critical resource for any taxpayer dealing with international treaties.

Filing Deadlines and Important Dates

Form 8833 must be filed as an attachment to the taxpayer's U.S. federal tax return. As such, it follows the annual tax return submission deadline, typically April 15. Failing to meet this deadline may result in penalties or the inability to apply the desired treaty benefits.

Should extensions be required, taxpayers have the option to file for an extension of time to file their individual income tax returns. However, this extension applies only to the submission of the form and not the payment of any taxes due. Maintaining awareness of these critical dates is essential for successfully utilizing treaty-based claims.

Penalties for Non-Compliance

The IRS imposes penalties on taxpayers who fail to submit Form 8833 when mandatory or inaccurately represent their treaty-based return positions. These penalties can be significant, based on the specifics of non-compliance, and may include fines up to $1,000 for individuals or $10,000 for corporations.

Non-compliance may result from failing to submit the form, not adhering to IRS instructions, or inaccurately claiming treaty benefits. Staying informed about these potential penalties encourages taxpayers to complete and submit the form accurately, minimizing financial risk and aiding in maintaining regulatory compliance.