Definition and Purpose of the 4797 Instructions 2016 Form

The 4797 Instructions 2016 Form provides essential information for taxpayers required to report the sale or exchange of business property. This document serves as a comprehensive guide to accurately report gains or losses from property transactions, including real estate and depreciable business assets. It helps taxpayers understand how to report specific transactions, ensuring compliance with IRS regulations.

Involvement in Business Transactions

- The form is integral for reporting varied business transactions, such as sales, exchanges, and involuntary conversions.

- Special rules apply to transactions involving sections 179 and 280F(b)(2) for recapture amounts, pertinent in calculating allowable depreciation deductions.

Steps to Complete the 4797 Instructions 2016 Form

Completing the 4797 Instructions 2016 Form requires careful attention to detail. The following steps guide you through this process:

-

Collect Necessary Information: Gather details about the property sold or exchanged, including purchase and sale dates, cost basis, selling price, and accumulated depreciation.

-

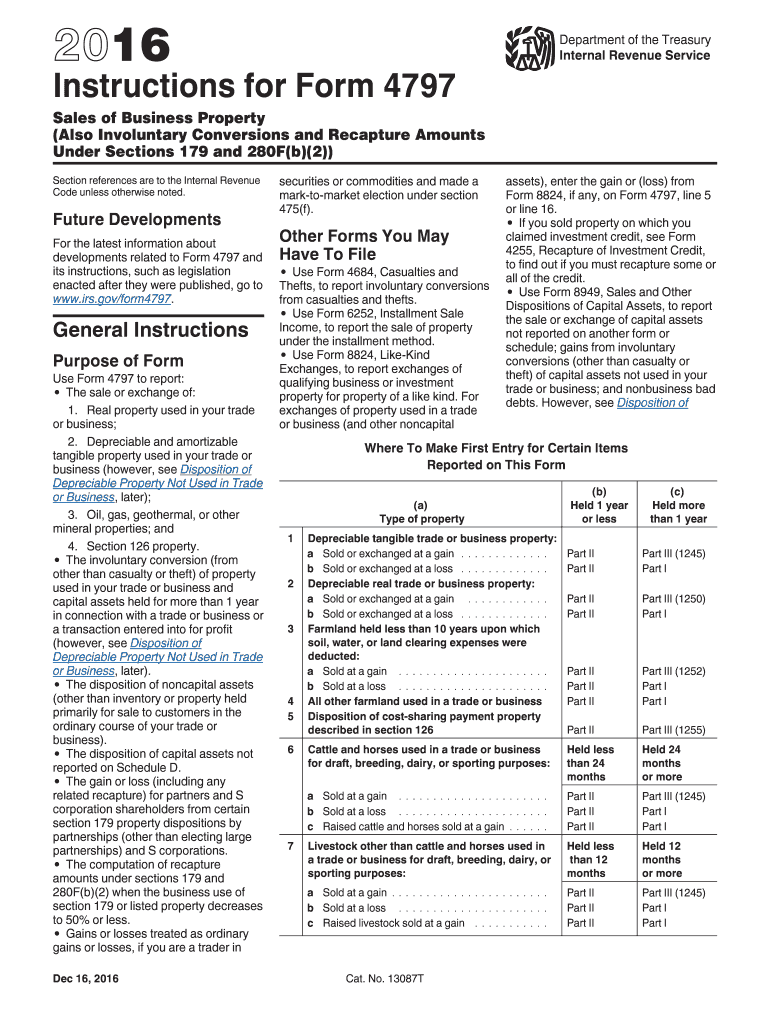

Understand the Sections: The form is divided into parts, each targeting specific types of property transactions. Familiarize yourself with each part to determine what applies to your situation.

-

Complete Part I: Report the sale or exchange of property held for more than one year. This section calculates the total gain or loss from long-term transactions.

-

Fill Out Part II: Document transactions for property held for one year or less, addressing short-term gains and losses.

-

Address Part III: This part focuses on computing ordinary gains and losses resulting from the sale of business property.

-

Utilize Part IV: Record all recapture amounts that may apply under specific IRS guidelines, especially those regarding sections 179 and 280F(b)(2).

Finalizing the Form

- Ensure all calculations are accurate and double-check information entered.

- Attach additional documentation required for specific properties or transactions.

- Review IRS guidelines to ensure compliance with all legal obligations.

Who Typically Uses the 4797 Instructions 2016 Form

Individuals and Business Entities

- Self-Employed Individuals: Frequent users needing to report business property gains and losses.

- Businesses: Corporations and partnerships often engage in transactions requiring this form to report asset dispositions.

- Retirees and Students: May use this form if they have investments in business property transactions.

Important Terms Related to the 4797 Instructions 2016 Form

Understanding specific terminology enhances the user’s comprehension and improves form accuracy:

- Depreciation: The formula for allocating the cost of tangible property over its useful life.

- Involuntary Conversion: Occurs when property is destroyed, stolen, condemned, or disposed of under threat of condemnation.

Tax Implications

- Recapture Amounts: Reflections of adjusted gains or losses based on prior depreciation deductions.

- Cost Basis: Original value of the property for tax purposes, adjusted by improvements, depreciation, and similar factors.

IRS Guidelines

Familiarize yourself with relevant IRS guidelines to ensure proper application of the 4797 instructions:

- The IRS outlines scenarios requiring the form and explanations for each involved tax consideration.

- Special IRS publications may provide further clarification on unique or complex transaction types.

Filing Deadlines and Important Dates

Meeting deadlines is crucial to avoid penalties:

- Tax filing date normally aligns with individual or business tax return deadlines, usually April 15.

- Extensions may provide additional time to file but not to pay owed taxes.

Submission Methods for the 4797 Instructions 2016 Form

Options make submission more flexible:

- Online Filing: Often the quickest method, with direct transmission to the IRS.

- Mail: Traditional, allows submission with the complete tax return package.

- In-Person: Less common, but an option if direct assistance is required.

Penalties for Non-Compliance

Failure to comply with guidelines for the 4797 Instructions 2016 Form can result in:

- Monetary Penalties: Fees imposed for incorrect or late submissions.

- Audit Risks: Increased scrutiny from the IRS during audits or reviews of improperly filed forms.

Avoiding Issues

- Ensure completeness and accuracy in all entries.

- Remain vigilant about deadlines and IRS updates regarding form requirements.