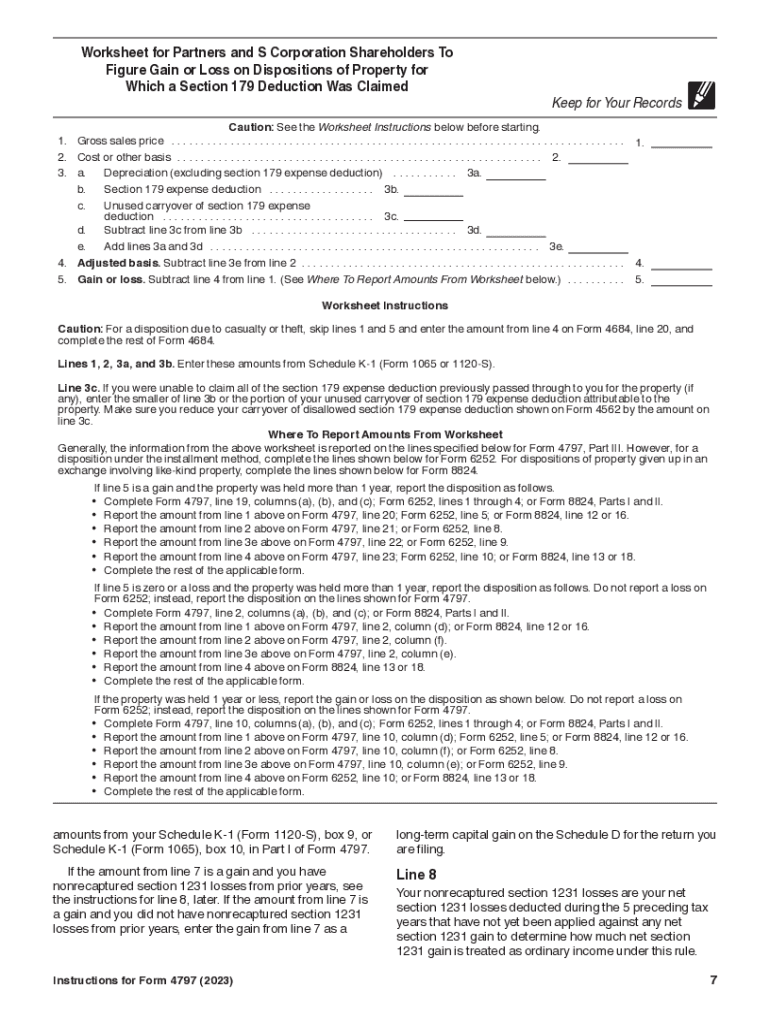

Definition and Purpose of Form 4797

Form 4797 is used for reporting the sale or exchange of business property, particularly real estate and depreciable assets. It serves several key purposes, such as tracking the profit or loss from sales, exchanges, involuntary conversions, or the disposition of certain business assets. It is crucial for accurately calculating capital gains and losses that affect your taxable income. The form addresses various scenarios, including installment sales and special elections regarding capital gains. Understanding its purpose within the tax code is essential for ensuring compliance and optimal financial reporting.

How to Use the Instructions for Form 4797

To effectively use the instructions for Form 4797, begin by identifying the specific type of property transaction you are reporting. The instructions provide detailed guidelines on categorizing your assets and calculating gains or losses. Pay close attention to sections detailing specific schedules and parts of the form. For example, real estate transactions might require completing Parts I and III, while involuntary conversions are addressed in Part IV. Regularly refer to examples provided in the instructions to verify the correct application of rules to your situation.

Steps to Complete Form 4797

- Gather Required Information: Collect details about the property, including purchase date, cost basis, improvements, and sale price.

- Choose Correct Part: Identify which part of Form 4797 applies to your transaction:

- Part I for sales of business property.

- Part II for ordinary gains and losses.

- Part III for recapture calculations.

- Part IV for involuntary conversions.

- Complete Necessary Sections: Enter information according to the specific guidelines:

- Calculate gains or losses for each transaction.

- Apply recapture rules where applicable.

- Review and Attachments: Ensure all figures align with documentation and attach supporting documents if required.

- Submission: File the completed form with your federal tax return.

Eligibility Criteria for Form 4797

Taxpayers eligible to use Form 4797 include individuals, corporations, and partnerships that have sold or disposed of business-use property. The form applies to transactions involving assets subject to depreciation recapture rules and capital gain or loss considerations. Eligibility may also depend on specific scenarios, such as conversion to personal use or involuntary conversions due to theft or casualty.

Filing Deadlines and Important Dates

Form 4797 must be submitted alongside your annual tax return, typically due on April 15th for calendar-year taxpayers. Extensions to file, such as Form 4868, extend the deadline but not the time to pay any taxes owed. It’s critical to align Form 4797 submission with other tax forms to avoid penalties for late filing, so plan accordingly and mark your calendar with important dates.

Required Documents for Form 4797

Adequate documentation is vital when completing Form 4797:

- Purchase Agreements: Demonstrates original purchase terms and price.

- Receipts for Improvements: Needed for adjusting the basis.

- Sales Contracts: Details the sale terms and disposition value.

- Depreciation Records: Essential for accurate recapture calculations.

- Expenses Related to Sale: Such as agent fees or closing costs.

Organize these documents meticulously, as they support figures reported on the form.

IRS Guidelines and Compliance

Adhere to IRS guidelines for accurately reporting gains or losses on Form 4797. Familiarize yourself with IRS publications that relate to your transactions to avoid common errors, such as incorrectly categorizing property types or omitting necessary schedules. Consistent compliance minimizes the risk of audits or penalties and promotes accurate tax payment. Consult IRS Publication 544 for additional insights.

Penalties for Non-Compliance

Failure to properly file Form 4797 can result in penalties, including late fees, interest on unpaid taxes, and additional scrutiny during audits. Misreporting or neglecting to report relevant transactions might invalidate deductions or capital loss claims. Ensuring accuracy and thorough documentation can significantly reduce risks associated with non-compliance.

Taxpayer Scenarios and Examples

Consider several examples of how taxpayers use Form 4797 for different scenarios:

- Small Business Owner: Selling a piece of machinery results in a gain, necessitating a report on Part II for ordinary income.

- Landlord: Disposing of a rental property qualifies for reporting in Parts I and III due to depreciation recapture.

- Accidental Conversion: A fire damages business property, triggering an involuntary conversion outlined in Part IV.

Recognizing these diverse scenarios aids in understanding the comprehensive use of the form across varying circumstances.