Definition & Meaning

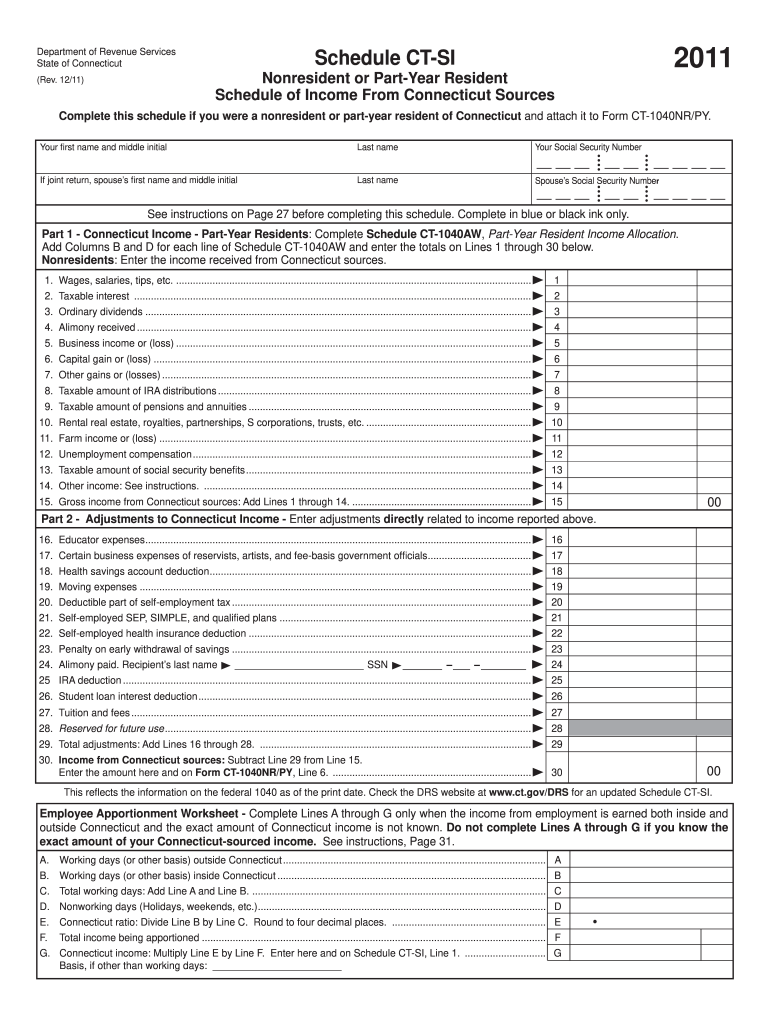

The Schedule CT-SI for 2011 is a tax document used by nonresidents or part-year residents of Connecticut. It facilitates the reporting of income derived from Connecticut sources. This schedule is essential for taxpayers to provide an accurate accounting of different income types and detail any necessary adjustments. It is a crucial attachment to Form CT-1040NR/PY when filing state taxes and ensuring compliance with Connecticut tax regulations.

Purpose and Significance

- Taxpayer Obligation: It aids taxpayers in meeting state mandates by accurately reporting income from Connecticut sources.

- Income Reporting: It allows for the documentation of various income types, such as wages, dividends, and other earnings linked to Connecticut.

- Required Attachment: It needs to be attached to the primary tax form, Form CT-1040NR/PY, for completing a nonresident or part-year resident return.

Use Cases

- Nonresidents Earning in Connecticut: Individuals living out-of-state but earning income from Connecticut are required to use this schedule.

- Part-Year Residents: Those who have moved into or out of Connecticut during the tax year need to report their Connecticut-source income for the period they were residing there.

How to Use the Schedule CT-SI 2011 Form

Preparation Steps

- Gather Information: Collect all documentation related to income earned from Connecticut, including pay stubs, dividend reports, and other financial statements.

- Understand the Form Requirements: Familiarize yourself with each section of the form. Note the requirements for each type of income to ensure accurate reporting.

Working through the Form

- Income Types: Identify and list each type of Connecticut-source income.

- Adjustments: Note any adjustments to income as required by Connecticut tax laws.

- Instructions: Carefully follow instructions to avoid errors, ensuring that all required fields are completed before submitting.

Tax Filing

- Attach the Schedule to Main Tax Form: Ensure it is attached to Form CT-1040NR/PY.

- Double-Check Details: Verify all entered data for accuracy to prevent issues with tax authorities.

Steps to Complete the Schedule CT-SI 2011 Form

-

Section A - Income Reporting:

- List all income earned from Connecticut sources.

- Include wages, self-employment income, and investments derived from Connecticut-based entities.

-

Section B - Adjustments:

- Record any applicable adjustments to accurately reflect net income.

- Adjustments may include various deductions allowed under Connecticut tax rules.

-

Section C - Documentation:

- Ensure necessary supporting documents are collected and referenced.

- Include proof of income and any other documents supporting reported figures and computations.

-

Final Review:

- Go through all entries with a focus on accuracy.

- Ensure the attachment to the primary tax filing form for submission.

Important Considerations

- Accuracy is Crucial: Errors can lead to filing delays or issues with tax compliance.

- Follow State Instructions: Each taxpayer's situation may present unique scenarios, so it's important to consult state-issued guidance when needed.

Key Elements of the Schedule CT-SI 2011 Form

Income Categories

- Employment Income: Wages, salaries, and tips from Connecticut employers.

- Investments and Dividends: Income from financial interests located in Connecticut.

- Other Earnings: Any additional income derived from Connecticut, such as rental income or business activities.

Adjustment Entries

- Allowable Deductions: Apply any dedictions that Connecticut tax laws permit for nonresidents.

- Income Modifications: Note modifications such as contest prizes from Connecticut or other taxable interactions.

Eligibility Criteria

Who Must File

- Nonresidents with Connecticut Income: Any nonresident earning income from Connecticut sources.

- Partial Year Residents: Individuals who lived in Connecticut for part of the year but relocated need to report for the time spent in the state.

Form Submission Methods

Electronic Filing

- Availability: Opt for e-filing for faster processing and an immediate acknowledgment of receipt.

- Platforms: Tax software and online platforms compatible with state e-filing submissions may be used.

Traditional Paper Filing

- Postal Service: Complete and mail the form to the appropriate Connecticut tax department address.

- Deadline Adherence: Ensure that the form is sent well ahead of the filing deadline to avoid delays.

Penalties for Non-Compliance

Consequences of Errors or Omissions

- Fines and Penalties: Failing to accurately report or file may result in penalties.

- Interest on Unpaid Taxes: Late payments can accrue interest, increasing the total amount owed.

Rectification Measures

- Correction Filings: If errors are discovered after submission, file amendments promptly.

- Consult Tax Professionals: Seek advice from tax professionals to navigate complex situations or resolve disputes with tax authorities.

Important Terms Related to Schedule CT-SI 2011 Form

Understanding Terminology

- Nonresident: An individual who lives outside Connecticut but earns income from within the state.

- Part-Year Resident: A resident for part of the year, either moving into or out of Connecticut.

- Source Income: All forms of income originating from Connecticut.

Clarifications

- State-Specific Definitions: Know terms as they are defined under Connecticut tax law to ensure comprehension and accurate filings.

- Tax Verbiage: Understanding specific terminology used in state tax forms is essential for compliance and accuracy.

IRS Guidelines

Relationship to Federal Tax Filing

- Connection to Federal Income: Income reported on federal returns must align with state filings, as differences can trigger reviews.

- State-Specific Rules: Connecticut may impose requirements differing from federal rules; understanding both layers is necessary for accurate filing.