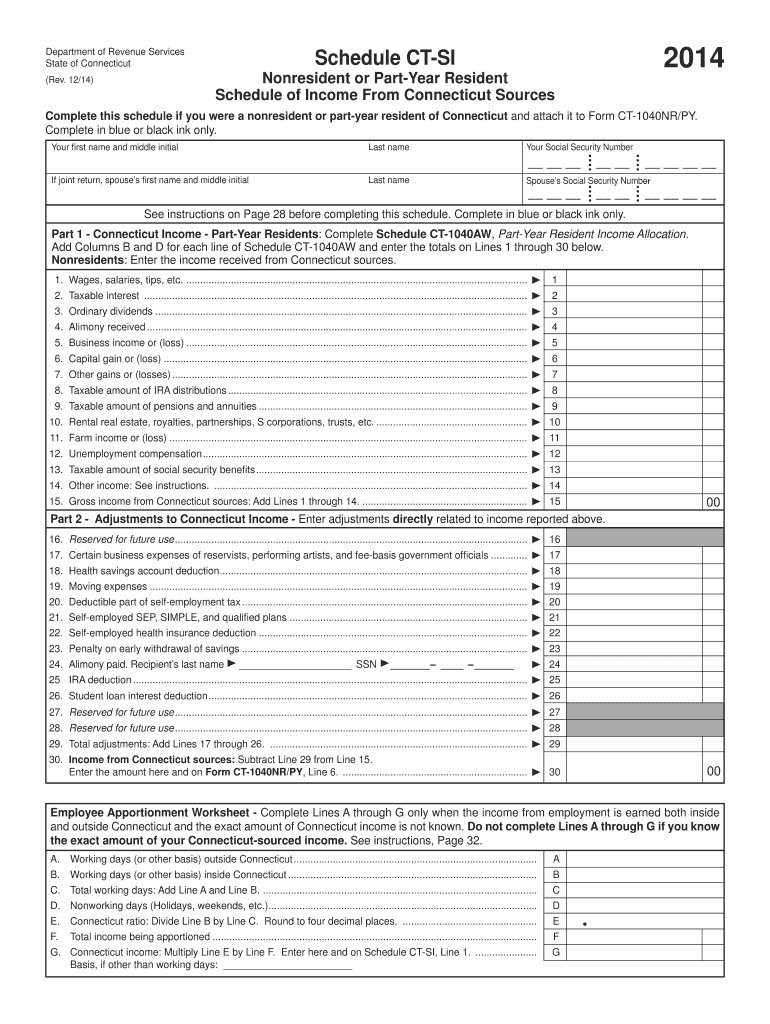

Understanding the Connecticut SI 2014 Form

The Connecticut SI 2014 Form, also known as Schedule CT-SI, is a documentation requirement specifically designed for nonresidents and part-year residents of Connecticut. It plays a crucial role in reporting income derived from sources within Connecticut. This form must be completed with precision as it is a requirement for both transparency and compliance with state tax regulations. It outlines various types of income and adjustments that should be reported in conjunction with the primary Form CT-1040NR/PY.

Steps to Complete the Connecticut SI 2014 Form

-

Gather Required Documents: Before starting, gather documents that prove income sources such as pay stubs, 1099s, or other relevant financial statements pertaining to Connecticut-derived income.

-

Identify Income Sources: Categorize types of income explicitly connected to Connecticut. This often includes wages, rental income, and business income within the state.

-

Report Adjustments: Include any necessary adjustments or deductions that apply to your reported income based on Connecticut tax laws.

-

Attach to Form CT-1040NR/PY: Once completed, the Schedule CT-SI must be attached to your main tax form for nonresidents or part-year residents.

-

Review and Submit: Double-check all entries for accuracy and compliance before submission. Filing can be done through mail or electronically, depending on your preference and the guidance provided by Connecticut tax authorities.

Who Typically Uses the Connecticut SI 2014 Form?

This form is essential for:

-

Nonresidents: Individuals who reside outside Connecticut but have income sources within the state.

-

Part-Year Residents: Those who moved into or out of Connecticut within the tax year and earned income while physically present in Connecticut.

-

Individuals with Multiple State Incomes: Those who work in more than one state or have diversified income streams that include Connecticut sources.

Important Terms Related to the Connecticut SI 2014 Form

-

Nonresident: A taxpayer who does not permanently reside in Connecticut but earns income from within the state.

-

Part-Year Resident: An individual who resides in Connecticut for a portion of the tax year.

-

Connecticut-Sourced Income: Income earned from jobs, businesses, or properties located in Connecticut.

Legal Use of the Connecticut SI 2014 Form

Schedule CT-SI is legally mandated for accurate tax reporting and compliance. The form's completion is necessary to ensure that individuals are taxed appropriately on income sources attributed to Connecticut, thereby avoiding potential legal penalties for underreporting.

Key Elements of the Connecticut SI 2014 Form

-

Income Categories: Clearly defined sections for different income types, such as wages, dividends, and business earnings.

-

Adjustments and Deductions: Fields for specific state-allowed deductions and credits that affect the taxable income amount.

-

Attachment Requirement: This form must be attached to Form CT-1040NR/PY for nonresidents and part-year residents.

State-Specific Rules for the Connecticut SI 2014 Form

Connecticut law dictates certain unique tax rules that must be followed when filing:

-

Specific Deductions: Only deductions recognized by Connecticut tax law can be claimed.

-

Source Verification: Income must be verifiably tied to Connecticut activities to be applicable.

This ensures compliance and correct tax obligations are met for income earned within the state’s jurisdiction.

Filing Deadlines / Important Dates

The filing deadline is typically aligned with federal tax deadlines, which means April 15 of the following year unless extensions are filed or specific Connecticut guidelines dictate differently for that tax year. Late submissions may incur penalties, so timely compliance is recommended.

Form Submission Methods

-

Online: Electronic submission is often available through Connecticut’s Department of Revenue Services website for convenience.

-

Mail: Alternatively, forms can be printed and mailed to the state's tax department, ensuring they are postmarked by the due date.

-

In-Person: Some may also opt to deliver their forms in person at designated Connecticut tax offices if necessary.