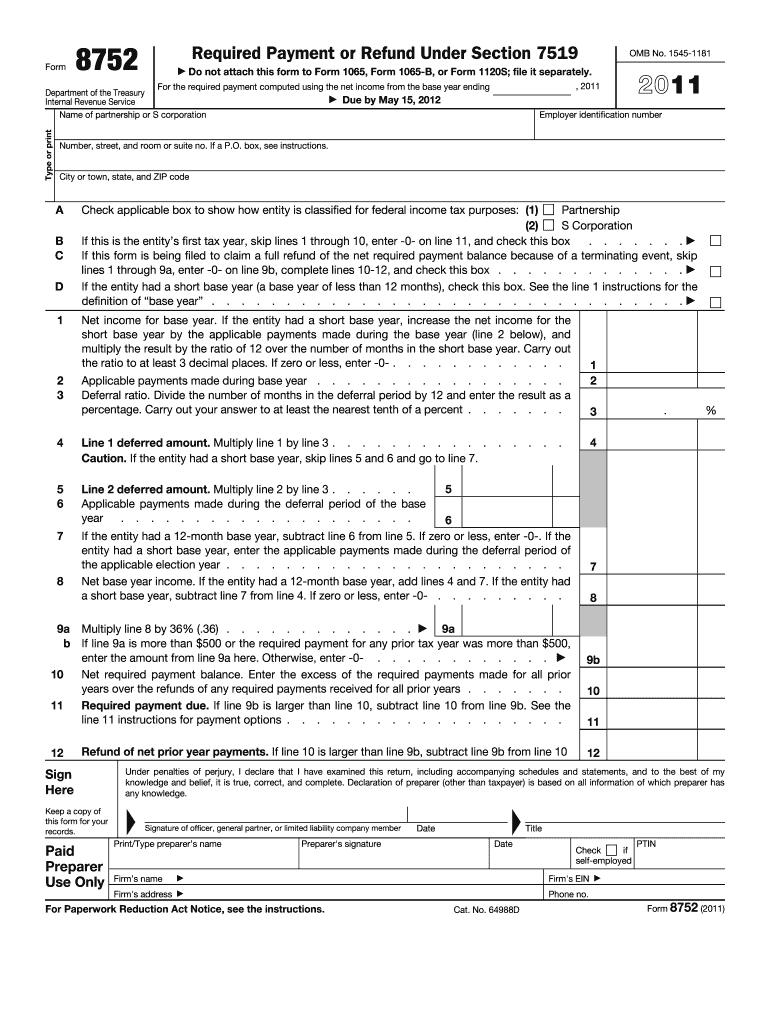

Definition and Purpose of the 2011 Form 8752

Form 8752 is used by partnerships and S corporations in the United States to comply with IRS Section 7519. It involves calculating and reporting the required payments due for adopting a tax year different from the mandatory calendar year or claiming refunds on previous payments. For the 2011 tax year, businesses must complete this form to ensure compliance with IRS regulations, reporting any required payments due by May 15, 2012. The form aids businesses in ensuring their tax year adjustments are properly accounted for by reconciling their fiscal activities with IRS timelines.

Key Elements of Form 8752

- Identifying Information: Basic details about the entity, such as its name and employer identification number (EIN).

- Computation of Required Payment: Instructions for calculating the payment required under Section 7519, taking into account net income offsets and any prior year credits.

- Refund Requests: Steps for claiming a refund of prior year payments if the calculated payment is less than previously paid.

- Signature Fields: Authorization sections which must be signed by a responsible officer or partner of the firm to validate the form.

Steps to Complete the 2011 Form 8752

- Fill in Identification Details:

- Enter the business’s name, address, and EIN at the top of the form.

- Calculate Net Income:

- Use the form’s instructions to determine the net income applicable to the deferral period.

- Compute Required Payments:

- Follow the line-by-line instructions to apply any credits or debits related to prior payments or adjustments.

- Review and Authorize:

- Carefully check all entries for accuracy and sign the form.

- Submit by Deadline:

- Ensure that the completed form is submitted by the IRS deadline, typically May 15 of the following year.

Required Documents

- Financial Statements: For the deferral period being reported.

- Previous Year’s Form 8752: If applicable, to guide refund or credit requests.

- EIN Verification Statement: To ensure accuracy in the identification section.

Legal Use of the 2011 Form 8752

This form is legally required for specific businesses opting for a fiscal year that does not coincide with the calendar year. It's crucial for partnerships and S corporations that have fiscal year elections to accurately report deferrals and associated tax impacts to the IRS. Failure to comply with the form’s filing can result in penalties assessed on the unpaid balance or miscalculated income deferrals.

Filing Deadlines and Important Dates

Form 8752 must be filed separately by May 15, 2012, for the 2011 tax year in compliance with IRS deadlines. Late submissions could lead to penalties or interest on unpaid amounts, emphasizing the importance of understanding and meeting the specified deadline to avoid potential financial repercussions.

IRS Guidelines for Form 8752

The IRS provides detailed instructions for calculating payments and securing any applicable credits. Entities must ensure that they adhere strictly to these guidelines to accurately reflect any tax liabilities or credits for the specified fiscal period.

Key Considerations

- Annual Filing: Must be repeated each year that the entity’s fiscal year differs from the calendar year.

- Accuracy: Ensure correct computation of net income and payments to minimize errors.

- Documentation: Maintain detailed records supporting all calculations.

Business Entity Types That Benefit Most

- Partnerships: Especially those with multiple fiscal year deferral periods.

- S Corporations: Entities benefiting from fiscal flexibility to optimize financial reporting.

Entities that understand and correctly use Form 8752 can better manage cash flow and leverage fiscal year adjustments to their advantage, supporting strategic financial planning throughout the tax year.