Definition & Meaning

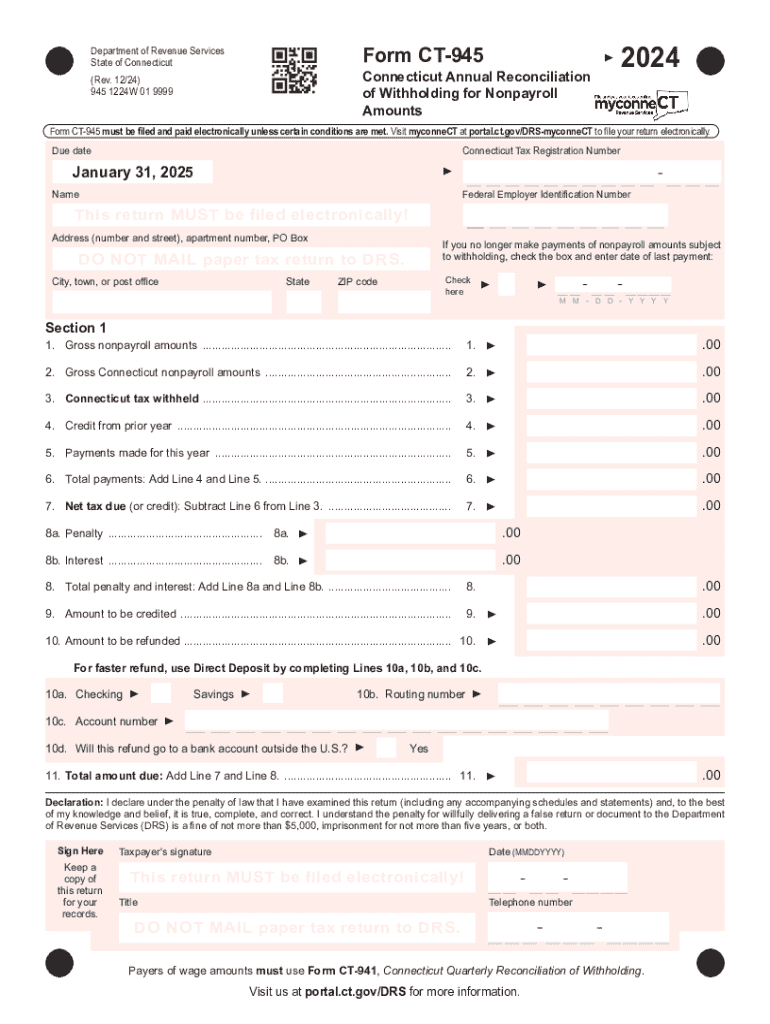

The 2 Form CT DRS CT-945, officially known as the Connecticut Annual Reconciliation of Withholding for Nonpayroll Amounts, serves an essential function for businesses and entities handling nonpayroll payments subject to Connecticut income tax withholding. This includes diverse categories such as lottery winnings, pension distributions, and other miscellaneous income types that aren’t classified under regular payroll. The form aims to consolidate and report the annual reconciliation for these specific withholding categories to the Connecticut Department of Revenue Services (DRS).

For businesses and organizations, understanding the intricacies of the Form CT-945 is crucial to ensure compliance with state tax obligations. This form acts as a comprehensive summary of all amounts that were withheld over the year and ensures that the state receives the correct amount of tax revenue from these nonpayroll sources.

How to Obtain the 2 Form CT DRS CT-945 Fill Online, Printable

Accessing the 2 Form CT DRS CT-945 can be seamlessly accomplished through the Connecticut Department of Revenue Services' website. Businesses and taxpayers can download these forms in a printable format or directly fill them out online. By visiting the official Connecticut DRS site, users will find not only the form needed but also additional resources and instructions that clarify its completion process.

To acquire the form:

- Navigate to the Connecticut DRS official website.

- Enter the "Forms" section.

- Search for "Form CT-945" to find both English and requirement-specific versions.

- Choose between downloading a blank printable PDF or utilizing an interactive online form, allowing real-time submission.

Ensuring access to the latest version of the form is vital to remain compliant with any updated filing requirements or legal standards instituted by the state.

Steps to Complete the 2 Form CT DRS CT-945 Fill Online, Printable

Completing the 2 Form CT DRS CT-945 requires attention to detail and a thorough understanding of Connecticut withholding requirements. Here’s a step-by-step guide to navigate the process:

-

Enter Business Information:

- Include the business name, address, Federal Employer Identification Number (FEIN), and the Connecticut Withholding Remitter Numer if applicable.

-

Provide Nonpayroll Payment Details:

- Gather information on all nonpayroll payments such as lottery winnings or pension distributions. Calculate the total payments for the year that were subject to withholding.

-

Fill Out Withholding Data:

- Detail the total withheld amounts and compare them to the required withholding amount determined by state guidelines. Ensure accuracy by referencing individual nonpayroll transactions.

-

Calculate Adjustments:

- Account for any previous overpayments or underpayments in withholding. Adjust totals accordingly to reflect any changes throughout the filing period.

-

Review Penalty Information:

- Understand the penalties that may be incurred for late filings or under-withholding, ensuring compliance with filing deadlines.

-

Finalize and Submit:

- Verify all information is correct before submitting. For online submissions, utilize SSL-secured platforms for safety. For printed forms, ensure all signatures and dates are accurate for submission via mail.

Each of these steps plays a crucial role in guaranteeing that the form is complete and submitted correctly, reducing the risk of errors and subsequent fiscal penalties.

Legal Use of the 2 Form CT DRS CT-945 Fill Online, Printable

The legal application of the 2 Form CT DRS CT-945 underpins its critical role in ensuring compliance with Connecticut's tax regulations. Entities leveraging this form must adhere to specific legal requirements to guarantee accurate and lawful submission.

-

Compliance with State Law: Businesses operating in Connecticut and making nonpayroll distributions are legally obligated to report these through Form CT-945. Failure to comply can lead to penalties and interest accrual on unpaid tax liabilities.

-

Electronic Filing Requirements: For certain businesses, electronic submission of Form CT-945 becomes mandatory, aligning with Connecticut's push towards modern tax filing systems.

-

Record Retention: Legally, taxpayers must retain copies of their CT-945 submissions and associated records for auditing purposes. This ensures transparency and accountability in case of state inquiries or reviews.

Understanding these legal parameters is essential for organizations to uphold their obligations under state law, mitigating risks associated with non-compliance.

IRS Guidelines

Although Form CT-945 is specific to Connecticut, its guidelines must align with the broader federal regulations overseen by the Internal Revenue Service (IRS). Connecticut tax regulations ensure consistency within federal withholding systems, allowing for coherent tax administration across state and federal levels.

-

Consistency with Federal Standards: Connecticut's withholding requirements must not contradict federal guidelines. This uniformity prevents discrepancies in taxpayer obligations across state and federal entities.

-

Federal Reporting Correlation: Information reported on the Form CT-945 often ties back to specific federal tax reporting requirements, making it imperative to cross-check facts and figures against federal tax returns and documents.

Awareness of these connections ensures that compliance with state filing does not inadvertently cause issues with federal tax obligations.

Filing Deadlines / Important Dates

Understanding critical filing deadlines for the 2 Form CT DRS CT-945 is vital to avoid penalties. The standard deadline for electronic submissions of the form is January 31, 2025, immediately following the tax year it concerns. However, businesses should be prepared with all necessary documentation well before this date to prevent last-minute issues.

- Early Preparation Recommended: Compiling withholding data throughout the year facilitates a smoother filing process once the year concludes.

- Grace Periods and Penalties: Connecticut may provide short grace periods post-deadline, but relying on these can risk incurring financial penalties.

Being proactive with the form submission safeguards against potential fees and non-compliance repercussions.

Penalties for Non-Compliance

Connecticut imposes specific penalties for non-compliance with Form CT-945 filing guidelines. Understanding these penalties encourages timely and accurate submissions:

- Late Filing Penalties: For every late submission, the state applies a fixed percentage penalty on the unpaid withholding amount, incentivizing punctuality.

- Under-Withholding Consequences: Should the reported withholding amount fall short of the required threshold, penalties and interest may accrue on outstanding amounts.

Accurate compliance ensures avoidance of these monetary penalties, protecting businesses financially and reputationally.

Who Typically Uses the 2 Form CT DRS CT-945 Fill Online, Printable

Form CT-945 is typically utilized by entities that handle nonpayroll payments subject to Connecticut income tax withholding, addressing the unique needs of these payment classes:

- Casinos and Lottery Agencies: Regularly report winnings subject to tax.

- Pension Administrators: Handle pension distributions requiring withholding compliance.

- Business Entities with Miscellaneous Nonpayroll Income: Include various companies engaging in financial activities with taxable distributions beyond traditional payroll.

Identifying the scope of businesses and organizations that must use the form helps guide entities in fulfilling their responsibilities effectively.