Definition & Meaning

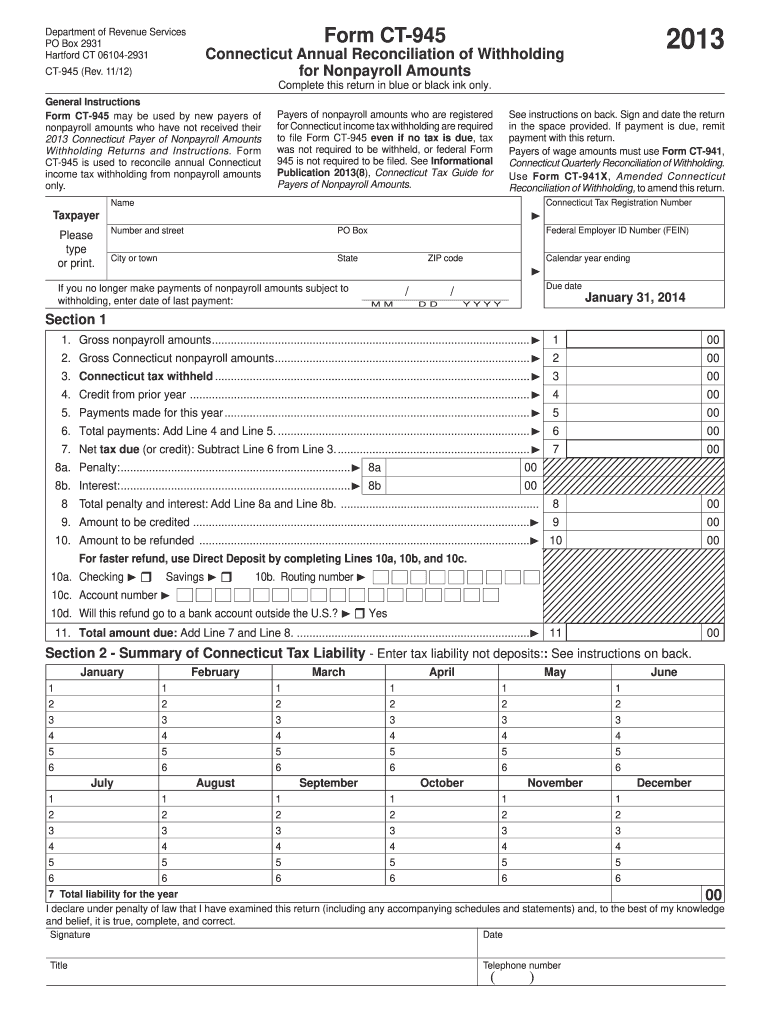

The Connecticut Form CT-945 for the year 2013 is an annual reconciliation form for nonpayroll amounts. It is used by employers or payers to report the amounts withheld for Connecticut income tax from nonpayroll payments throughout the fiscal year. This form ensures that the annual withholding amounts have been accurately reported and reconciled, reflecting the correct total of nonpayroll income tax withheld for the state of Connecticut.

How to Use the Form CT

Employers and payers should use Form CT to summarize the total nonpayroll amounts from which Connecticut taxes were withheld over the year. It acts as a reconciliation tool, aligning periodic withholding reported throughout the year with the actual amounts withheld. The form should be completed with precision, ensuring that all figures are accurately represented. Typically, the user will need to reference payroll records and other financial documentation to complete the form accurately.

Steps to Complete the Form CT

- Gather Required Documents: Collect all relevant payroll records and any documents that reflect nonpayroll withholdings, such as 1099s.

- Fill in Identifying Information: Enter the employer's name, address, and federal employer identification number (FEIN).

- Enter Total Nonpayroll Amounts: Calculate and fill in the total nonpayroll amounts paid to recipients.

- Calculate Withholding Amounts: Report the total Connecticut income tax withheld throughout the year.

- Reconcile Withholdings: Compare the reported periodic payments with the totals to ensure consistency.

- Sign and Date: Ensure the form is signed and dated by authorized personnel before submission.

- Submit by Deadline: Complete and submit the form by January 31, 2014.

Filing Deadlines / Important Dates

- Annual Submission Deadline: January 31, 2014, for the fiscal year 2013.

- Payment Submission if Owing: Any discrepancies or outstanding amounts from withheld tax must be resolved by this deadline.

Missing these deadlines may result in penalties and interest charges imposed by the Connecticut Department of Revenue Services.

Who Typically Uses the Form CT

Businesses and entities that have withheld Connecticut state income taxes from nonpayroll payments such as pensions, retirement distributions, and gambling winnings are typical users of Form CT. This includes corporations, limited liability companies (LLCs), and other business entities that process nonpayroll amounts requiring tax withholding.

Penalties for Non-Compliance

Failure to submit Form CT by the stated deadline can result in significant penalties. These may include:

- Late Filing Penalties: Financial penalties accrued per month until the form is filed.

- Interest Charges: Daily interest on overdue taxes from the due date until the payment is received.

Ensuring timely and accurate submission of Form CT helps avoid such financial liabilities.

Required Documents for Form Submission

- W-2s and 1099 Forms: Reflecting nonpayroll compensation and withholding.

- Payroll Records: Providing detailed accounts of all nonpayroll transactions with tax withheld.

- Previous Filings: Prior year reconciliation forms for reference, if needed.

Having these documents prepared can streamline the form completion process and aid in accurate reconciliation.

Software Compatibility

Form CT can be completed using accounting software compatible with the Connecticut filing requirements. Common software includes:

- TurboTax: Offers user guidance on state-specific tax forms.

- QuickBooks: Facilitates detailed financial record tracking and form preparation.

These platforms allow for efficient data management and help ensure compliance with state-specific tax legislation, simplifying the filing process for businesses.

Examples of Using the Form CT

Consider a corporation that distributes gambling winnings to residents of Connecticut. Throughout 2013, the company withheld state income taxes from these winnings. At the end of the fiscal year, the corporation would use Form CT to report and reconcile the withheld taxes against the payments made during the year, ensuring all amounts match the reported totals. This form would ensure compliance with state tax laws and avert potential penalties.