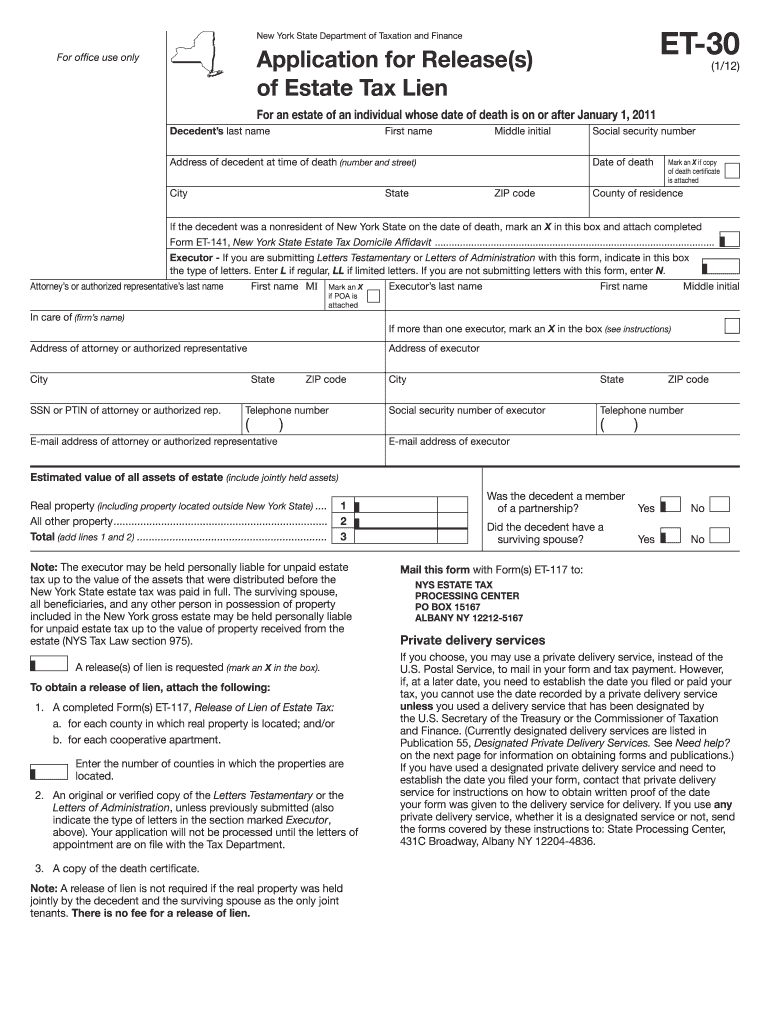

Definition and Purpose of the ET-30 2012 Form

The ET-30 2012 form is a specific application used by the New York State Department of Taxation and Finance. Its primary purpose is to facilitate the release of estate tax liens on properties of individuals who passed away on or after January 1, 2011. This form serves as a vital tool for executors or authorized representatives of an estate, providing essential information about the deceased, their assets, and the necessary supplementary documents needed for compliance with estate tax regulations.

Steps to Complete the ET-30 2012 Form

- Gather Personal Details: Start with collecting information about the decedent, including their full name, Social Security number, and date of death.

- Asset Inventory: Compile a comprehensive list of the decedent’s assets. This includes real estate, bank accounts, investments, and personal property.

- Required Documentation: Prepare supplemental documents such as death certificates and letters of appointment from the court.

- Form Completion: Fill out the form by entering all required data in the specified fields, making sure each section is thoroughly completed.

- Review and Verification: Double-check all entries for accuracy and completeness to prevent delays or rejections.

Who Typically Uses the ET-30 2012 Form

The ET-30 2012 form is primarily used by executors or authorized representatives of an estate. Executors are responsible for managing and settling the decedent’s estate, ensuring compliance with estate tax laws, and relaying necessary information to the tax authorities. Legal professionals, such as estate attorneys, might also utilize this form to ensure proper estate management and taxation compliance.

Key Elements of the ET-30 2012 Form

- Decedent Information: Include details such as the name, Social Security number, and date of death of the deceased.

- Estate Details: A summary of the estate's total value, including real property and personal assets.

- Attachments: Required supporting documents like death certificates, court-issued letters of appointment, and other relevant paperwork.

- Signatory Section: Space for signatures of the executor or authorized representative to validate the information provided.

Legal Use of the ET-30 2012 Form

The ET-30 2012 form plays a crucial role in the legal process of estate taxation. It aids in determining the liability for estate taxes under New York State law and ensures that any tax liens on the decedent's properties are addressed, allowing for legal transfers to heirs or beneficiaries. Proper completion of this form helps in the clearance of any governmental claims against the estate, thus assisting in settling the decedent's affairs legally.

Steps to Obtain the ET-30 2012 Form

- Official Website: Visit the New York State Department of Taxation and Finance website to download the form directly.

- Local Tax Offices: Request the form from local offices to ensure you have the latest version available.

- Professional Assistance: Contact an estate attorney or tax professional who can provide the form and assist with its completion.

State-Specific Rules for the ET-30 2012 Form

In New York, estate tax laws stipulate the need for the ET-30 form specifically for estates of a certain size or complexity. Executors must adhere to New York's guidelines, which may differ from federal estate tax regulations. It’s essential to be aware of specific state-level exemptions, tax rates, and deadlines to ensure compliance and avoid any penalties.

Required Documents When Filing the ET-30 2012 Form

- Death Certificate: This official document verifies the decedent’s death and informs the tax authority of the need to process the estate.

- Court Appointment Letters: These letters confirm the executor’s authority to act on behalf of the estate.

- Estate Inventory: A detailed list of the decedent's assets, providing the total value of the estate for tax assessment purposes.

Penalties for Non-Compliance with the ET-30 2012 Form

Failing to file the ET-30 2012 form in a timely manner can result in significant penalties. Potential consequences include fines, increased tax liabilities, and delays in the processing of the estate. Non-compliance may also affect the legal release of estate tax liens, potentially hindering the transfer of estate assets to beneficiaries. Executors must ensure timely and accurate submission to avoid these legal and financial repercussions.