Definition & Meaning

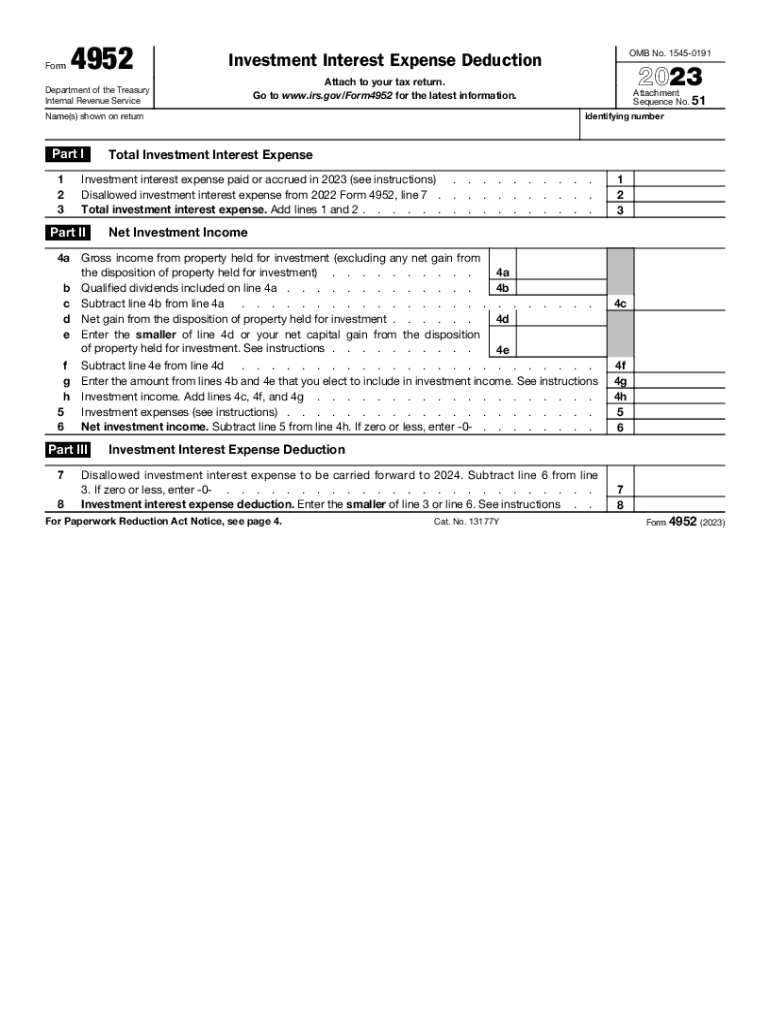

Form 4952, titled "Investment Interest Expense Deduction," is a critical tool provided by the Internal Revenue Service (IRS) for taxpayers to calculate the deduction they can claim for investment interest expenses. Primarily aimed at individual taxpayers, estates, and trusts, the form helps determine the allowable deduction by comparing total investment interest expenses with net investment income. The purpose is to minimize tax liabilities associated with such interests, aligning with the IRS's broader framework on permissible tax deductions.

Investment interest expense refers to the interest paid on borrowed money specifically used to purchase taxable investments. It is crucial to ensure honesty and precision while reporting, as misleading entries can lead to penalties or audits. Understanding this form involves assessing which expenses qualify and how they align with particular income streams, a central element for taxpayers involved in investment activities.

Eligibility Criteria

Eligibility to file Form 4952 hinges on the taxpayer incurring interest expenses due to investments. Both individuals and certain business entities like estates and trusts are eligible. However, the key criterion is that the investment income must be taxable. Therefore, if a taxpayer's investments are tax-exempt, such as municipal bonds, those interests do not qualify for deduction purposes under this form.

Investment expenses must directly tie into generating taxable income to be deductible. Moreover, the taxpayer's filing status, the source of their total income, and whether they're subject to the alternative minimum tax (AMT) could affect their eligibility and the form’s application, making it essential to determine the precise financial circumstances influencing each case.

Key Elements of Form 4952

Form 4952 consists of several crucial parts that guide taxpayers through the process of calculating their eligible investment interest expense deduction:

- Total Investment Interest Expense: The total interest paid during the tax year on investment loans.

- Net Investment Income: The form instructs users on how to calculate their net investment income, which is crucial since deductions cannot exceed this income.

- Disallowed Interest: Any interest expense not deductible in the current year due to limitations and carried forward to future tax years.

This structure ensures clarity and transparency, facilitating an accurate calculation of deductible investment interest. It also emphasizes the importance of detailed record-keeping for all investment-related financial activities.

Steps to Complete Form 4952

Completing Form 4952 involves a series of steps aimed at ensuring precision:

-

Gather Documentation: Collect all financial records related to investment activities. This includes interest statements, investment account statements, and records of any other related expenses.

-

Calculate Total Investment Interest: Sum the interests paid for the tax year explicitly tied to investments.

-

Determine Net Investment Income: This involves calculating the income from all investments (dividends, interests, annuities) minus any related deductions and expenses.

-

Complete Part I to III: Fill out the form's sections by starting with total interest, then net investment income, and finally calculate the deduction allowed.

-

Review Entries: Double-check all calculations and consultations, particularly if filing under complex tax situations.

IRS Guidelines

The IRS issues specific guidelines detailing the criteria for investment-related expenses to be deductible. According to these, investors must ensure:

- The investments are taxable, and the corresponding expenses relate directly.

- Documentation supporting all claims must be maintained for record-keeping and audit purposes.

- Taxpayers must adhere to limits on interest deductions, which cannot exceed net investment income.

Familiarizing oneself with these IRS guidelines can significantly aid in the proper and accurate submission of Form 4952, ensuring compliance and potentially reducing tax burdens effectively.

Taxpayer Scenarios

Form 4952 can apply to a variety of taxpayer scenarios:

- Self-Employed Individuals: If a self-employed individual borrows money to invest in their business or other income-generating ventures, this form is crucial to delineate deductible from non-deductible expenses.

- Retirees: Retired individuals with income from dividends or interest who have taken out loans to optimize their investment portfolio can use Form 4952 to accrue deductions.

- Landlords and Property Investors: Those using loans to purchase properties that yield rental income might fall under this form's purview if they seek to deduct their loan interest.

Each scenario can have varied implications on how Form 4952 is utilized, making specific inquiries crucial for detailed guidance.

Penalties for Non-Compliance

Failing to comply with IRS requirements when filing Form 4952 can lead to significant penalties. These can range from monetary fines to audits where further discrepancies might be uncovered, increasing the financial burden on non-compliant taxpayers. Ensuring accurate entries and adherence to IRS rules is imperative for avoiding such repercussions.

Non-compliance results in more than financial penalties, as it can prompt a review of all financial affairs, demanding detailed documentation. Hence, a proper understanding of Form 4952’s requirements and diligent record management are beneficial practices for maintaining tax compliance.

Filing Deadlines / Important Dates

Form 4952 must be filed alongside your regular annual tax return, which is generally due by April 15 of the following year. Taxpayers should keep abreast of any specific dates or extensions, particularly in circumstances of financial hardship or those caused by extraordinary events, such as natural disasters, which might impact the general state of tax filings.

Timeliness is essential, as missing the deadline could invalidate deductions altogether for the reporting period, aligning with IRS regulations that underscore timely compliance for availing tax benefits.