Definition and Purpose of Form 4952

Form 4952, officially known as the "Investment Interest Expense Deduction," is a critical tax document used by individuals, estates, or trusts in the United States to determine the amount of deductible investment interest expenses for a tax year. The form is necessary to ensure that those with investment expenses can account for these with the IRS and potentially reduce their taxable income. Investment interest expense is the interest paid on loans that were used to purchase investment property which may include stocks, bonds, or real estate. By filing Form 4952, taxpayers determine how much of that interest can be deducted, based on their net investment income.

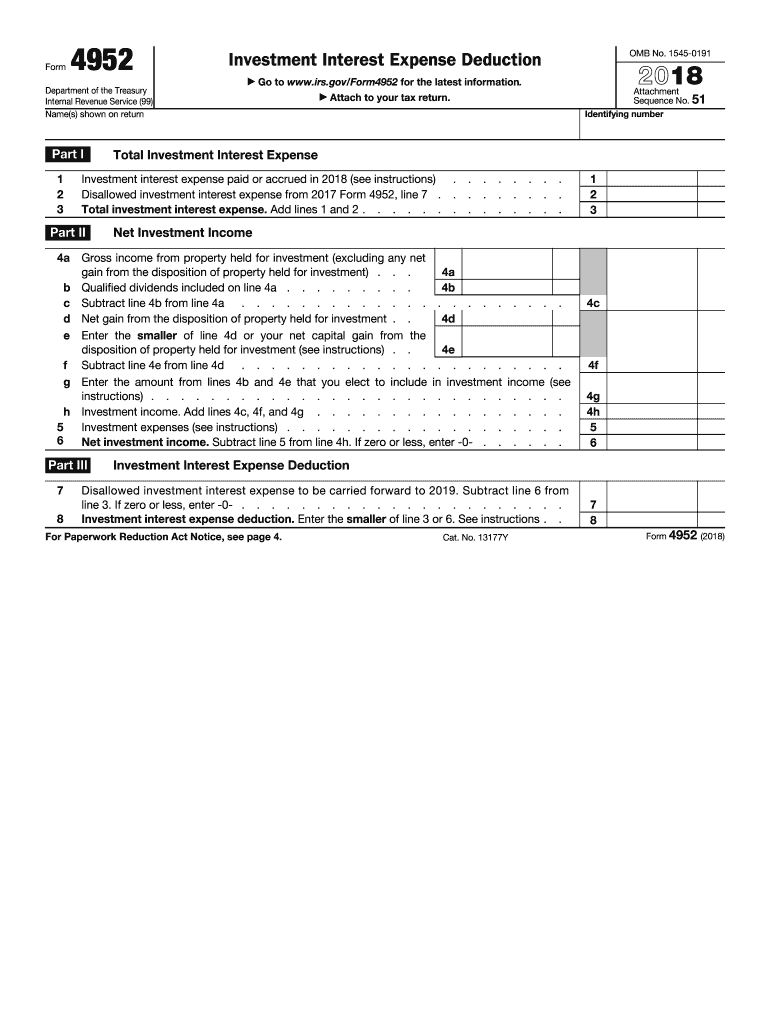

Key Elements of Form 4952

- Investment Interest Expense: Total amount of interest paid on borrowed money to acquire investment assets.

- Net Investment Income: Income generated from investment activities, including dividends, interest, and short-term capital gains.

- Deductible Amount: The portion of the investment interest expense that can be deducted, computed by comparing the total expenses against the net income.

- Carryover: Any disallowed portion of the interest expense that can be carried forward to subsequent tax years.

Steps to Complete Form 4952

Filling out Form 4952 can be detailed, requiring several steps to ensure accuracy. Here's a streamlined approach:

-

Data Collection:

- Gather your financial records showing the total amounts of your investment property loans and any income generated from these investments.

-

Calculate Total Investment Interest Expense:

- Utilize your records to input the total interest paid on investment loans. This goes in Part I of the form.

-

Determine Net Investment Income:

- In Part II, calculate your net investment income by tallying revenues from investments, minus any related expenses.

-

Deductible Calculation:

- Use Part III to compare and compute the deductible investment interest. This requires inputs from the first two parts to determine excess amounts or carryover opportunities.

-

Complete Filing:

- After calculating the correct figures, the total deductible amount is noted, and any disallowed interest is prepared for carryover if applicable.

How to Obtain Form 4952

Form 4952 can be acquired through several straightforward methods:

- IRS Website: Directly download the form as a PDF from the official IRS website. This gives access to the latest version and instructions.

- Tax Software: Platforms such as TurboTax and QuickBooks often incorporate the latest tax forms, including Form 4952.

- Professional Accountants: Tax professionals typically have copies of all necessary tax forms and can provide accurate filing assistance.

Important Terms Related to Form 4952

To fully grasp the intricacies of Form 4952, it's crucial to understand these terms:

- Investment Property: Refers to any type of property acquired to generate income, including stocks, rental properties, and interest-bearing accounts.

- Interest Expense: The cost incurred from borrowing money to finance investment property purchases.

- Disallowance: This may occur when the total investment interest expense exceeds net investment income, limiting the deductible amount for that year.

- Net Investment Income Tax (NIIT): A 3.8% tax applied to some or all of an individual's income if it surpasses certain thresholds, potentially increasing the importance of calculating deductible expenses precisely.

IRS Guidelines on Form 4952

Adherence to IRS guidelines ensures compliance and prevents errors:

- Instruction Review: The IRS provides detailed instructions alongside the form, which should be carefully reviewed to understand eligibility and calculation methods.

- Record Keeping: Maintain comprehensive records of all expenses and incomes related to investments as documentation for the IRS.

- Filing Requirements: Ensure timely submission of Form 4952 with your annual tax return to avoid penalties or audits.

Penalties for Non-Compliance with Form 4952

Non-compliance or incorrect filing of Form 4952 can result in serious repercussions:

- IRS Penalties: Errors or failures to file can lead to fines or penalties assessed by the IRS.

- Disallowed Deductions: Failing to file correctly may result in disqualification from deducting investment interest in the current or future years.

- Audits: Incorrect or incomplete forms increase the likelihood of IRS audits, which can further complicate tax matters and result in additional fines.

Taxpayer Scenarios Involving Form 4952

Form 4952 is applicable to various taxpayer scenarios:

- Individual Investors: Those using personal loans to fund stock purchases can deduct the interest when calculating investment income taxes.

- Real Estate Investors: Landlords with mortgages on rental properties may qualify to deduct these expenses, enhancing profitability.

- LLC Members: Members of limited liability companies with investment interests can leverage Form 4952 to manage personal tax liabilities.

Software Compatibility for Form 4952

Streamlining the completion of Form 4952 is often best achieved with reliable tax software:

- TurboTax and QuickBooks: These platforms offer direct support for Form 4952, handling the calculations and entry of data through their interfaces.

- Integration Capabilities: Many tax softwares allow importation of investment and financial data, reducing manual entry and error rates.

- Updates and Support: Software programs are regularly updated with IRS guidelines, ensuring compliance without having to individually track tax law changes.