Definition & Meaning

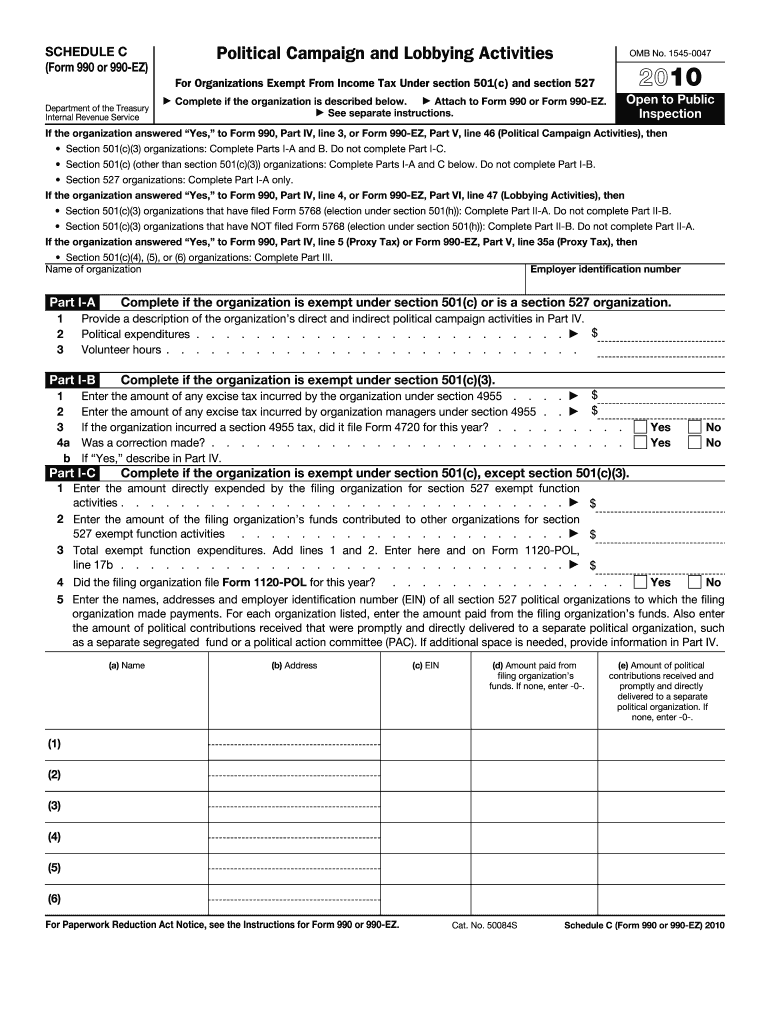

Schedule C of Form 990 or 990-EZ is used by tax-exempt organizations in the U.S. to report political campaign and lobbying activities. Specifically, it is intended for organizations exempt from income tax under sections 501(c) and 527 of the Internal Revenue Code. This form provides a detailed outline of the political expenditures made by these organizations, as well as volunteer hours dedicated to political activities. It includes specific instructions for different types of organizations based on their tax-exempt status. The primary purpose of this schedule is to ensure transparency in the political and lobbying activities of tax-exempt organizations.

How to Use the 2010 Form 990 Schedule C

To use the 2010 Form 990 Schedule C appropriately, it is vital to first identify the type of organization completing the form, as different sections apply to different entities. Users should:

- Identify the Organization Type: Determine if you are a section 501(c) or 527 organization as this dictates which parts of the form you will need to complete.

- Gather Necessary Information: Collect detailed records of political expenditures, lobbying activities, and volunteer hours related to campaign work.

- Complete Relevant Sections: Fill out sections that are pertinent to your organization type. Ensure that all questions are answered as accurately and completely as possible.

- Double-Check for Accuracy: Before submission, review all the information for accuracy and compliance with IRS guidelines.

Steps to Complete the 2010 Form 990 Schedule C

Completing the form involves several steps:

- Collect Financial Data: Ensure you have all necessary financial records related to political activities.

- Fill Out Part I: Provide detailed information about your organization’s political contributions.

- Complete Part II if Applicable: If engaged in lobbying activities, enter the relevant details in this section.

- Use Part III for 527 Organizations: If your organization is a 527, ensure this part is filled out accurately.

- Review Additional Guidance: Use IRS instructions for specific guidelines associated with each part of the form.

- Verify Entries: Ensure all data entries and calculations are correct before submission.

Key Elements of the 2010 Form 990 Schedule C

Essential components of the form include:

- Part I: Details on financial involvement in political campaigns.

- Part II: Information on lobbying activities and expenses.

- Part III: Data specific to 527 organizations.

- Attribution of Expenses: Clearly attribute all expenses to specific activities for transparency.

- Certification and Signature: A certification by an authorized person is mandatory for form validity.

Filing Deadlines / Important Dates

The 2010 Form 990 Schedule C must be filed by the 15th day of the 5th month after the end of an organization’s accounting period. For organizations with a calendar year accounting period, this would typically mean a filing date of May 15th. Late filing can result in financial penalties, emphasizing the importance of timely submission.

Who Issues the Form

The Internal Revenue Service (IRS) is responsible for issuing the Form 990 Schedule C. Organizations can access this form and additional instructions through the IRS website or their local IRS office. The IRS provides these resources to ensure that tax-exempt organizations comply with federal requirements regarding political and lobbying activities.

Required Documents

To complete the Form 990 Schedule C, organizations should compile:

- Detailed Financial Statements: Records reflecting all political and lobbying finances.

- Volunteer Records: Documentation of volunteer hours dedicated to political campaigning.

- Expenditure Reports: Clear breakdowns of funds used in support of or opposition to political candidates.

- Organizational Bylaws: These may be necessary to determine applicable parts of the form.

Penalties for Non-Compliance

Failing to file the 2010 Form 990 Schedule C, or providing inaccurate information, can lead to significant penalties. These may include fines and the potential revocation of tax-exempt status for the organization. The penalties underscore the importance of meticulous record-keeping and adherence to IRS requirements when engaging in political and lobbying activities.

Examples of Using the 2010 Form 990 Schedule C

Consider a 501(c)(3) charity that organizes a campaign to lobby for educational reforms. This organization must report the expenses related to these activities on Schedule C, Part II. Another example involves a 527 political organization making direct financial contributions to a candidate, which must be tracked and reported in Part III, ensuring compliance and transparency in political financing.