Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send it via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out ak carryovers with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open the ak carryovers document in the editor.

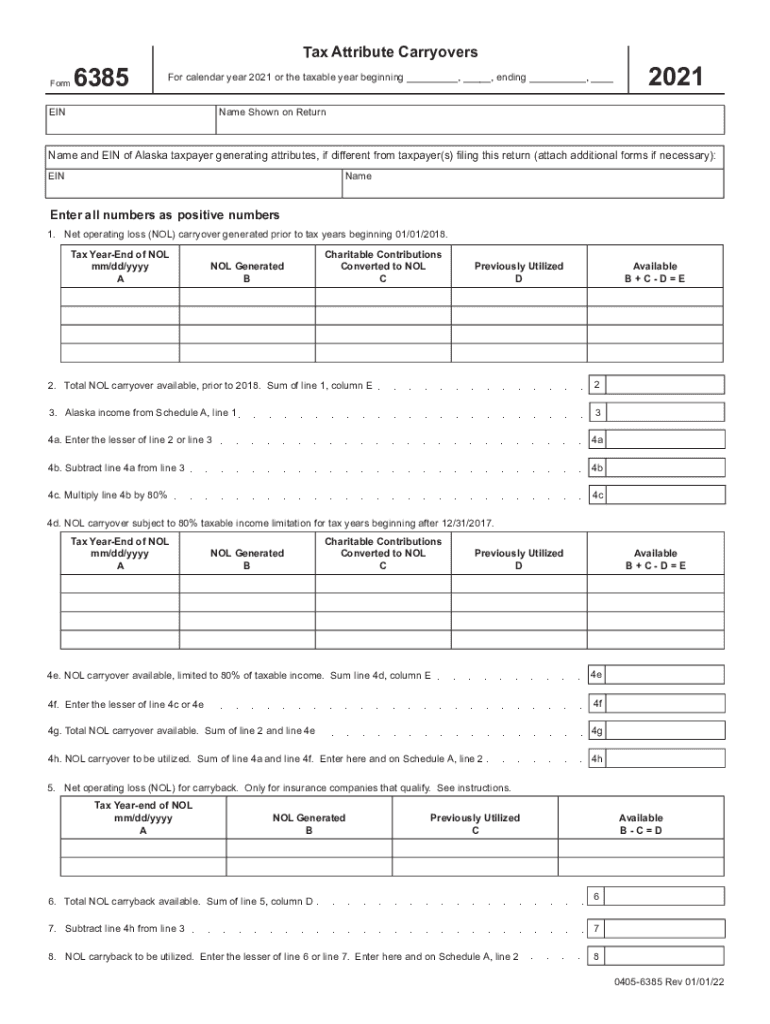

Begin by entering your EIN and the name shown on your return at the top of the form. Ensure accuracy as this information is crucial for identification.

For section 1, input your net operating loss (NOL) carryover details. Fill in the tax year-end date, and provide values for columns A through D to calculate available NOL.

Continue to section 2, where you will sum up line 1, column E to determine total NOL carryover available prior to 2018.

In sections 4a through 4h, follow the prompts carefully. Enter values from previous calculations and ensure you multiply correctly as instructed for taxable income limitations.

Complete sections regarding capital losses and charitable contributions by following similar steps—inputting dates and values accurately.

Start using our platform today for free to streamline your ak carryovers process!

AlaskaCare Employee Health Plan - State of Alaska DRB

The carryover is limited to the maximum deductible of their selected AlaskaCare plan. Employees are responsible for securing documentation from their formerRead more

Alaska INBRE is seeking proposals for one-time biomedical research-related expenses. A man in a white lab, safety glasses and rubber gloves places a glassRead more

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.