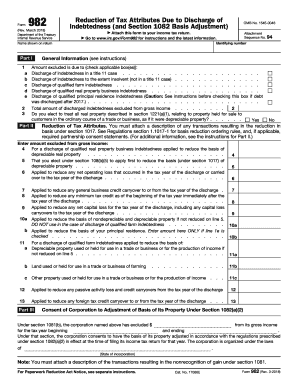

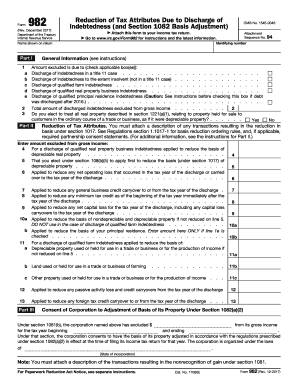

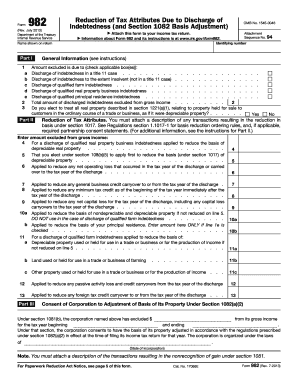

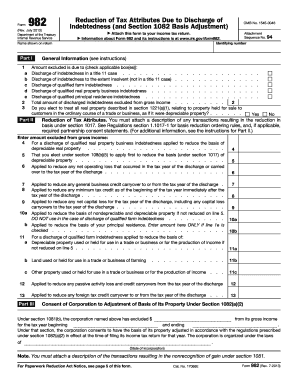

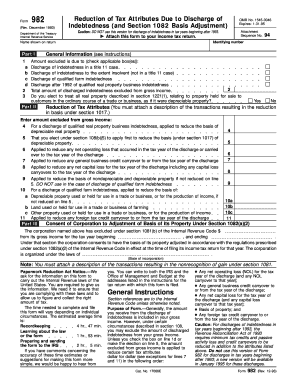

The form is utilized to determine the amount of discharged debt that can be excluded from gross income, subject to specific circumstances outlined in section 108 of the Internal Revenue Code.

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.