Definition & Meaning

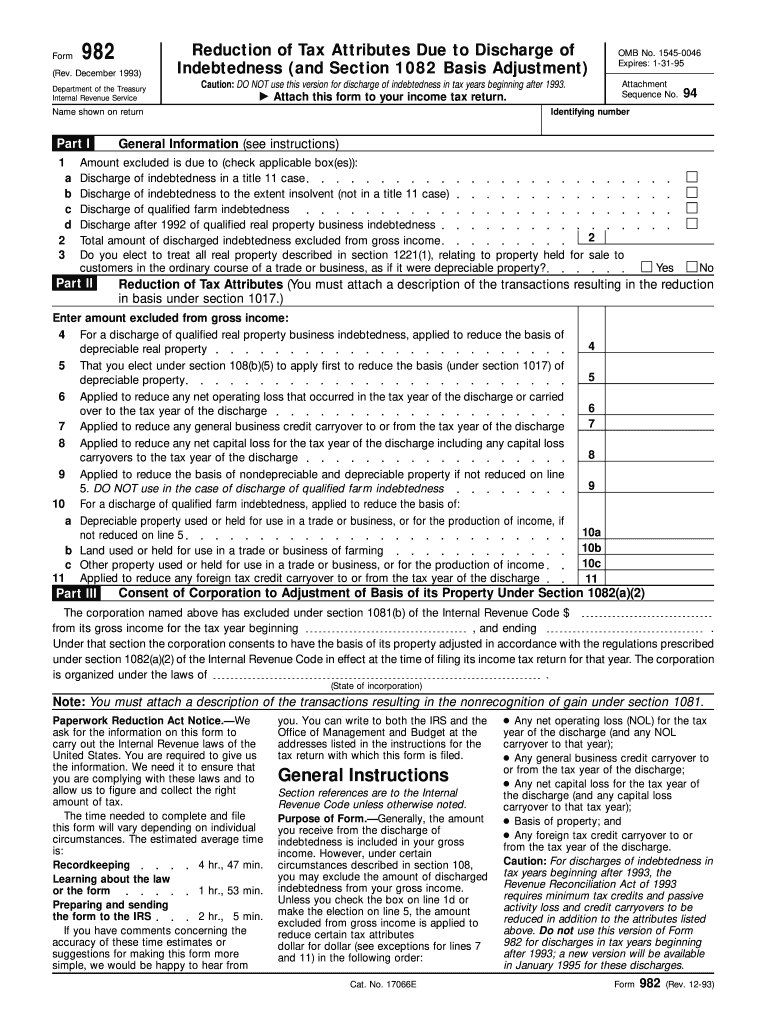

The form "Caution: DO NOT use this version for discharge of indebtedness in tax years beginning after 1993" refers to a document that was once utilized by taxpayers to report the reduction of tax attributes related to indebtedness discharge. This form plays a role in the adjustment of tax obligations under specific conditions outlined in the Internal Revenue Code. The essential detail of this form is the warning against its use for tax years starting after 1993, indicating that changes in tax laws or regulations have rendered it obsolete for those years.

Historical Context

- Pre-1994 Usage: Prior to 1994, this form was valid for reporting reductions in tax attributes due to discharged debts.

- Post-1993 Caution: Amendments in tax legislation prompted the warning against its use after 1993, to ensure compliance with updated tax regulations.

How to Use the Form Pre-1994

Although the form should not be used for tax years beginning after 1993, understanding its previous uses can offer insights into discharge of indebtedness processes.

Steps for Pre-1994 Use

- Identify Debt Discharge: Determine if your debt qualifies for exclusion from gross income.

- Complete Appropriate Sections: Fill out sections specifying reduced tax attributes, such as net operating losses or basis reductions.

- Review IRS Codes: Ensure compliance with applicable sections of the Internal Revenue Code to justify exclusions.

- Exceptions and Conditions: Taxpayer must check conditions under tax laws existing before 1994 to ensure proper application of reductions.

IRS Guidelines

The Internal Revenue Service (IRS) provides specific guidelines for handling indebtedness discharge, primarily via other forms and procedures for post-1993 tax years.

Key IRS References

- Form 982: Current form for managing discharge of indebtedness, directly replacing older forms for post-1993 scenarios.

- Publication 4681: IRS publication explaining cancellation of debt income, exclusions, and reductions.

Key Elements of the Form

Components of the Obsolete Version

-

Debt Details: Information about the discharged debt that is to be excluded from income.

-

Tax Attribute Reductions: Sections to report reductions such as basis in property or net operating losses.

-

Legal Compliance: Elements to ensure the taxpayer was adhering to the tax laws relevant before 1994.

Filing Deadlines / Important Dates

For forms related to discharge of indebtedness, including Form 982 which replaced the obsolete version, it is critical to adhere to IRS filing deadlines.

Deadlines for Related Forms

- Annual Tax Deadline: Typically April 15, the deadline for filing personal income tax returns, including any forms reporting attribute reductions.

- Extensions: Taxpayers can apply for extensions but must still comply with deadlines for documentation submission.

Required Documents

When dealing with discharge of indebtedness, specific documentation supports claims of income exclusion and attribute reduction.

Typical Supporting Documents

- Discharge Agreements: Official letters from creditors forgiving debt.

- Financial Statements: Documentation of financial status before and after debt forgiveness.

- Tax Documents: Previous returns that highlight relevant attributes like net operating losses.

Penalties for Non-Compliance

Failure to adhere to the IRS guidelines for forms related to debt discharge can result in significant penalties.

Potential Penalties

-

Monetary Fines: IRS may impose fines for failing to report or incorrectly applying attribute reductions.

-

Legal Consequences: Incorrect filing or reliance on outdated forms may lead to audits or legal action.

-

Accuracy-related Penalty: Taxpayers providing incorrect information on modern forms parallel to the obsolete versions face penalties for inaccuracies.

Who Typically Used This Form

Before its obsolescence, specific categories of taxpayers frequently utilized the form for debt-related tax adjustments.

Typical Users

- Individuals with Significant Debt Relief: Those who gained from large debt forgiveness prior to 1994.

- Businesses Under Restructuring: Companies reducing liabilities experiencing debt cancellations impacting their taxable income.

Legal Use of the Form

Historically, utilizing the form required strict adherence to legal guidelines to ensure the justified discharge of indebtedness and corresponding tax adjustments.

Legal Considerations

- Section Compliance: Adhering to Internal Revenue Code sections concerning discharge of indebtedness.

- Pre-1994 Laws: Use was governed by the tax law in place before 1994 changes rendered this version obsolete.

Versions or Alternatives to the Form

Taxpayers now use different documentation to report discharge of indebtedness, in alignment with changes in tax law.

Current Alternatives

- Form 982: Officially replaces the older form for debt discharge reporting.

- Digital Filing: Modern IRS systems facilitate online submission of related forms, increasing accuracy and convenience.

Digital vs. Paper Version

With technological progress, filing processes for related forms have shifted predominantly towards digital platforms, supported by IRS and tax preparation software.

Digital Advantages

-

Efficiency: Easier document management and submission.

-

Accuracy: Software reduces errors and ensures compliance with latest IRS guidelines.

-

Accessibility: Allows taxpayers across the United States to file from any location with internet access.

Business Types that Benefit Most

Certain businesses are more likely to encounter scenarios necessitating report of indebtedness discharge.

Business Beneficiaries

- Startups: Early-stage companies that undergo extensive debt restructuring.

- Large Corporations: Companies engaging in significant debt restructuring tend to use available modern forms to manage tax implications.

These evolutionary changes in filing practices highlight the importance of staying informed about tax regulatory updates and adhering to the most current procedures and documentation such as Form 982 in lieu of the obsolete form discussed.