Definition & Meaning

Form 8916-A for 2010 is designed as a supplemental attachment to Schedule M-3, which is part of the U.S. Internal Revenue Service (IRS) tax reporting requirements. This form is specifically used to provide detailed schedules of cost of goods sold, interest income, and interest expense. Entities required to file Schedule M-3 utilize Form 8916-A to ensure compliance with the Internal Revenue Code's stipulations by reporting the differences between book and tax amounts. This level of detail is essential for meeting the IRS's transparency and reporting standards.

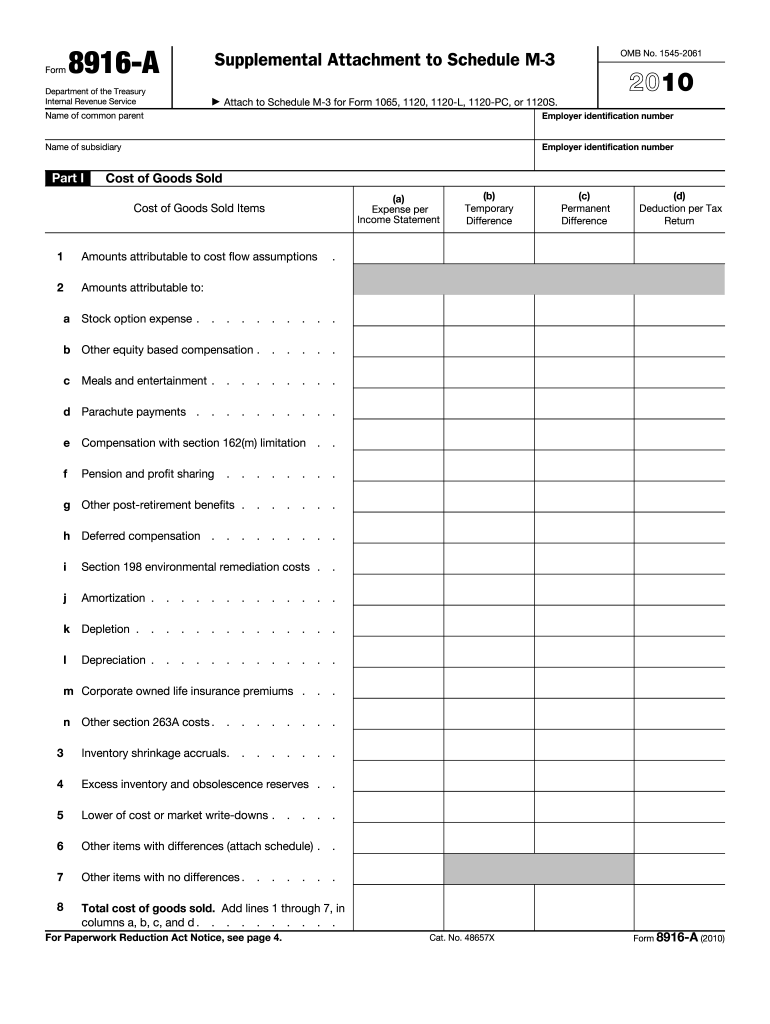

How to Use Form 8916-A 2010

When preparing Form 8916-A, it is crucial to accurately detail all relevant financial information that supports submissions on Schedule M-3. The form requires entities to:

- Itemize the components of cost of goods sold.

- Enumerate interest income and expenses.

- Reconcile differences between the amounts reported on a taxpayer's books and on their tax return.

Preparation of this form often requires collaboration between accountants and financial officers to gather and verify the necessary data, ensuring all corporate financial dealings are transparently reported to the IRS.

Steps to Complete Form 8916-A 2010

Completing Form 8916-A involves several detailed steps:

- Gather Financial Information: Compile detailed records of all inventory costs, interest income, and expenses.

- Identify Book vs. Tax Differences: Determine discrepancies between book-keeping records and tax reports for the necessary categories.

- Calculate Values: Accurately calculate total amounts for cost of goods sold, interest income, and interest expense.

- Complete Each Section: Enter all calculated figures in the appropriate sections of Form 8916-A.

- Review and Submit: Double-check figures for accuracy and consistency before attaching to Schedule M-3 and submitting with your tax return.

Important Terms Related to Form 8916-A 2010

Understanding key terms related to Form 8916-A can enhance the accuracy of its completion:

- Cost of Goods Sold (COGS): The direct costs attributed to the production of the goods sold by a company.

- Interest Income: Income earned from investments or loans provided to other parties.

- Interest Expense: Costs incurred from borrowing funds.

- Book vs. Tax Differences: Disparities between how expenses and incomes are accounted for in financial books versus tax documents.

Familiarity with these terms is essential for completing the form accurately.

IRS Guidelines

The IRS provides explicit guidelines for completing Form 8916-A, emphasizing transparency and consistency. These guidelines ensure that all financial figures reported on the tax forms match the corporation's accounting records. Taxpayers are advised to refer to the IRS instructions when completing the form to avoid discrepancies that could lead to audits or penalties.

Filing Deadlines / Important Dates

For the tax year 2010, Form 8916-A should be filed alongside Schedule M-3 and other related tax documentation by the corporate tax filing deadline. Typically, this deadline falls on March 15 for calendar-year corporations. Extensions can be requested, but the basic form must be submitted by the conventional deadline to avoid any potential late filing penalties.

Required Documents

Completing Form 8916-A necessitates various supporting documents:

- Detailed schedules of inventory changes and costs for the year.

- Documentation of interest income and expenses.

- Records substantiating book vs. tax differences, such as accounting records and reconciliation schedules.

Having these documents organized and available will streamline the completion of Form 8916-A and verify the accuracy of the reported amounts.

Penalties for Non-Compliance

Non-compliance with the requirements associated with Form 8916-A can result in significant penalties. These may include:

- Fines: Monetary fines for incomplete or late submission of required forms.

- Audits: Increased likelihood of an IRS audit, which can uncover further compliance issues.

- Legal Actions: Potential legal consequences for failing to meet IRS requirements.

Being diligent and timely in filing this form helps in avoiding these penalties.

Who Typically Uses Form 8916-A 2010

Form 8916-A is predominantly used by corporations that are required to file Schedule M-3 with their tax return. This includes large corporations, typically those with total assets greater than $10 million, ensuring transparency in financial reporting. These organizations fill out the form to provide a detailed reconciliation of financial reports and tax submissions, helping maintain compliance with the IRS.

Form Submission Methods (Online / Mail / In-Person)

There are several ways to submit Form 8916-A:

- Online: Many corporations file their forms electronically through authorized IRS e-file providers, which streamlines the process and ensures immediate submission.

- Mail: Alternatively, corporations can send physical copies of the form, alongside their tax returns, directly to IRS processing centers.

- In-Person: For direct communication, taxpayers may choose to submit forms in person at IRS locations.

Choosing the submission method that complements existing workflows is crucial for efficient tax filing.