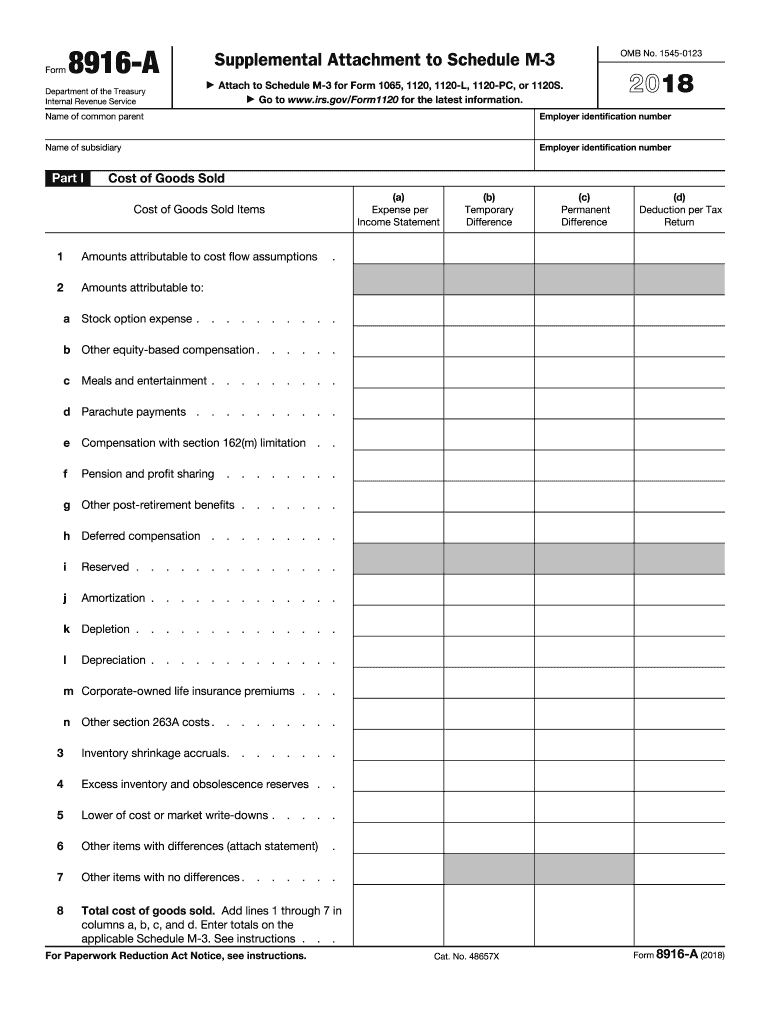

Definition and Purpose of Form 8916-A

Form 8916-A is a supplementary document required by the IRS for entities filing Schedule M-3, particularly concerning corporate tax returns. This form facilitates detailed reporting by laying out a comprehensive schedule of items such as the cost of goods sold, interest income, and other deductions. The primary goal of Form 8916-A is to bridge the financial accounting records and tax reporting, ensuring transparency and accurate reflection of financial activities.

Key Features of Form 8916-A

- Cost of Goods Sold: Entities must provide a breakdown of all costs involved in producing goods or services sold, including raw materials, labor, and overhead expenses.

- Interest Income and Expenses: The form requires detailed input on interest received and paid, which is crucial for organizations with significant borrowing or lending activities.

- Financial to Tax Reconciliation: It necessitates a reconciliation between financial statement accounts and their tax return counterparts, facilitating consistency and accuracy in reporting.

How to Obtain Form 8916-A

Form 8916-A can be accessed through multiple channels. It is available on the official IRS website, where it can be downloaded as a PDF file for offline usage. Additionally, tax preparation software often includes this form as part of their standard package, allowing for electronic filing options. For those seeking physical copies, IRS offices offer paper forms, though this may require a formal request or visit.

Alternative Methods to Access the Form

- Tax Software Platforms: Using services like TurboTax or QuickBooks provides automated access to Form 8916-A, streamlining the preparation and submission process.

- Professional Tax Consultants: Engaging a tax professional ensures that the form is obtained and completed accurately, leveraging their expertise in navigating IRS requirements.

Steps to Complete Form 8916-A

The process of filling Form 8916-A involves several structured steps, focused on ensuring the information aligns with IRS guidelines and organizational financial records.

- Gather Financial Documents: Collect all relevant financial statements, including income statements and balance sheets, to ensure accuracy.

- Fill Out General Information: Enter basic entity information such as name, address, and Employer Identification Number (EIN).

- Detail Cost of Goods Sold: Use the worksheet provided in the form to detail material costs, labor expenses, and manufacturing overheads.

- Report Interest Income and Expenses: Complete the relevant sections that segregate interest received from that paid out, ensuring clear demarcation.

- Reconcile Financial Differences: This involves comparing ledger entries with tax return entries to report any discrepancies.

- Review and Sign: Ensure all entries are correct before signing off. Review against the IRS instructions to validate all data.

Important Considerations

- Accuracy: Ensuring all figures are precise greatly reduces the risk of audits or penalties.

- Understanding Adjustments: Familiarity with accounting principles and tax regulations is crucial for correctly interpreting and entering adjustments.

Importance and Uses of the 2016 Federal 8916 Form

The utilization of Form 8916-A is crucial for maintaining compliance with federal tax regulations and providing clarity in tax reporting. It facilitates a deeper understanding of the financial transactions that impact taxable income, especially for corporations.

Advantages of Using Form 8916-A

- Transparency: Offers a detailed view of a corporation's financial health and operational expenses to the IRS.

- Compliance: Ensures adherence to federal guidelines, minimizing risk of penalties or discrepancies.

- Informed Decision-Making: Provides a clear financial picture, aiding in future financial planning and decision processes.

User Demographics of Form 8916-A

Form 8916-A is primarily used by entities required to file Schedule M-3, which encompasses certain large corporations and partnerships. These typically include publicly traded companies and those with consolidated assets exceeding $10 million.

Typical Users

- Large Corporations: Especially those involved in complex financial operations and multinational transactions.

- Tax Professionals: They often aid such corporations in preparing and submitting tax returns using Form 8916-A.

- Accountants and Financial Officers: Responsible for ensuring that financial reconciliations align with IRS requirements.

Guidance from IRS on Form 8916-A

The IRS provides specific guidelines for the completion and submission of Form 8916-A, emphasizing the importance of accuracy and thoroughness.

Submission Guidelines

- Filing Channels: The form can be submitted electronically as part of the entity's corporate tax return. Mailed submissions are also accepted if using paper filing methods.

- Deadline: Typically coincides with the corporation's tax filing due date. Extensions may apply under specific circumstances.

- Instructions: The IRS website provides detailed instructions, offering step-by-step guidance on completing the form correctly.

Common Errors to Avoid

- Mismatch of Figures: Failing to reconcile figures between financial records and the form.

- Incorrect EIN Entries: Ensure the Employer Identification Number is entered accurately.

Filing Deadlines and Key Dates

The form should be filed along with the corporate tax return, usually due on the 15th day of the fourth month following the end of the tax year (typically April 15 for calendar-year taxpayers).

Key Dates to Remember

- Tax Year Deadline: Coincides with the corporate tax filing deadline.

- Extension Filing: If additional time is needed, filing for an extension is crucial to avoid penalties.

By understanding the comprehensive requirements of Form 8916-A, entities can ensure compliance and accuracy in their tax reporting, leveraging this document as a critical tool in their financial documentation practices.