Definition and Meaning

Understanding the "Individual Income Tax Estimated Payments - Filing Requirements - Illinois" helps individuals comply with state tax obligations. This guideline outlines who is required to make estimated tax payments, which is essential for those whose income is not subject to withholding tax, such as self-employed individuals or those with substantial investment income. By estimating taxes owed throughout the year, taxpayers can avoid underpayment penalties and manage their tax liabilities more effectively.

Required Documents

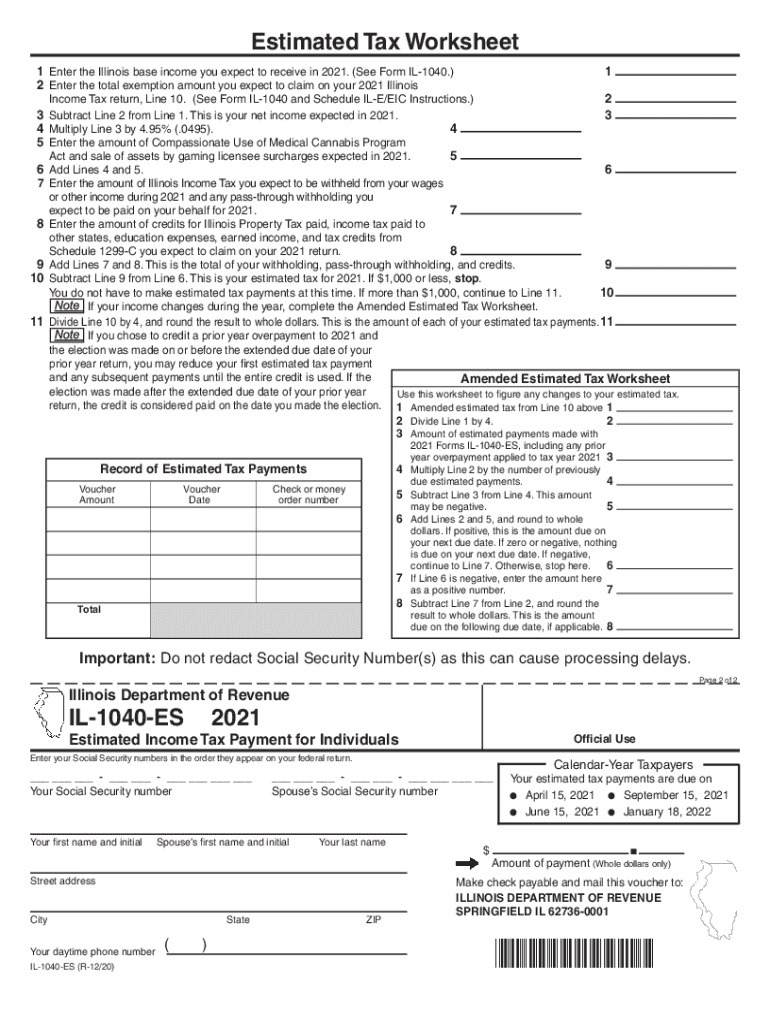

To comply with the "Individual Income Tax Estimated Payments - Filing Requirements - Illinois," gather pertinent financial documents, including your previous year’s tax return, records of other income sources, and any documentation of eligible deductions or credits. These materials help in accurately estimating your current tax liability, ensuring that the quarterly payments reflect your financial situation. Access to these documents facilitates completing the Estimated Tax Worksheet, critical for determining payment amounts.

Important Documents Include

- Previous year’s tax return

- Records of all income sources

- Documentation for deductions and credits

- Estimated Tax Worksheet

How to Obtain the Form

The form for tax estimated payments is accessible through the Illinois Department of Revenue's website. You can download it or request a paper version via mail. Some taxpayers prefer electronic submission, which can streamline the process through platforms compatible with the state’s systems. Ensure you access the most recent version of the form for compliance with current tax laws.

Steps to Complete the Form

-

Calculate Estimated Taxable Income: Begin with your total expected income for the tax year, incorporating all sources such as wages, self-employment income, and dividends.

-

Determine Applicable Deductions: Subtract allowable deductions to ascertain your taxable income. Reference prior tax documents and updated deductions rules for accuracy.

-

Apply Current Tax Rates: Use the state's current tax rate for your income bracket to calculate your estimated tax liability.

-

Account for Tax Credits: Deduct applicable tax credits from your estimated liability to determine your net tax amount due.

-

Divide into Quarterly Payments: Split your net amount into four equal payments, noting due dates to avoid penalties for late submissions.

Filing Deadlines / Important Dates

Timely submission of estimated tax payments prevents penalties. The Illinois Department of Revenue specifies quarterly deadlines: April 15, June 15, September 15, and January 15 of the subsequent year. Acknowledge changes in deadlines that may arise from weekends or holidays by submitting payments on the next business day. Stay informed through public announcements from the department, especially in cases of adjustments due to special circumstances.

Penalties for Non-Compliance

Failure to submit the Individual Income Tax Estimated Payments can result in penalties. The penalty generally applies to underpayments exceeding $1,000. Interest accumulates on underpaid amounts starting from the due date. First-time offenders may receive leniency if reasonable cause is demonstrated. Understanding the penalty structure can motivate timely compliance, ensuring alignment with legal requirements.

Who Typically Uses the Form

This form primarily supports individuals with income not subject to Illinois withholding, including freelancers and business owners. Additionally, retirees with significant non-pension income or investors with notable capital gains must also comply. Recognizing the relevant taxpayer categories ensures the correct application of estimated payment requirements.

State-Specific Rules

Illinois has specific rules governing estimated tax payments. Unlike some states, Illinois includes a flat tax rate across all income levels, simplifying calculations. However, taxpayers must still carefully evaluate all income against this fixed rate. Certain credits, like the Earned Income Credit, directly affect state tax liabilities and must be considered. Adhering to these specific rules facilitates accurate and lawful tax handling.

Software Compatibility

For those utilizing tax preparation software such as TurboTax or QuickBooks, compatibility with Illinois tax forms ensures a smoother filing experience. These software solutions automate calculations and often include specific state templates, minimizing errors and expediting the process. Ensure your software is up-to-date to incorporate recent tax changes and maintain compliance with evolving Illinois tax laws.

Supported Software Features

- Automated calculations

- State-specific form templates

- Regular updates to reflect tax law changes