Definition and Purpose of Editable Form 56 2011

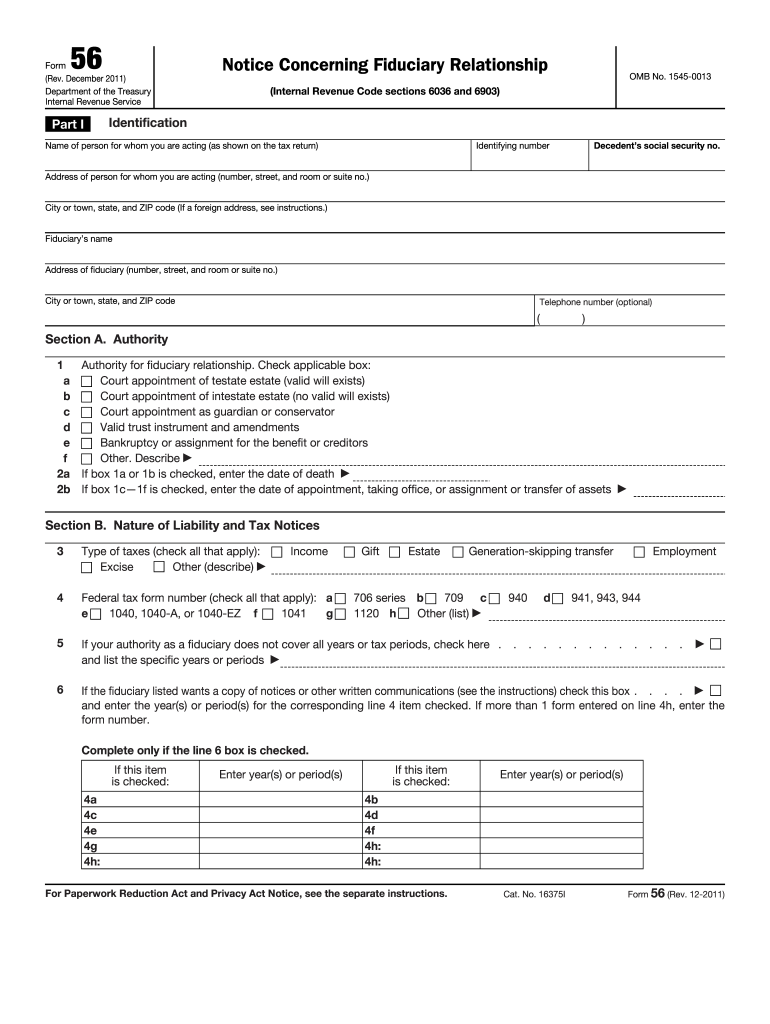

Editable Form 56 2011 is a notice used primarily for fiduciary relationships, as issued by the Internal Revenue Service (IRS). It identifies the fiduciary, who acts on behalf of a taxpayer, and outlines their authority concerning the taxpayer's tax matters. The form includes critical details about the decedent or taxpayer, fiduciary details, and any relevant court or administrative proceedings. This form is essential for clarifying who is responsible for the taxpayer's obligations and ensuring all parties understand the extent of those responsibilities.

Steps to Complete Editable Form 56 2011

Completing Editable Form 56 2011 involves several specific steps to ensure accuracy and compliance:

-

Gather Information: Collect all necessary information, including the taxpayer's name, Social Security Number, and the fiduciary’s details.

-

Complete Required Sections: Fill out sections identifying the fiduciary's authority and the tax matters involved. It is crucial to accurately specify the relationship context and the type of tax forms relevant to the fiduciary duties.

-

Review Legal Documentation: Ensure any required court documents or powers of attorney are complete and attached, as these support the fiduciary’s authority.

-

Double-Check for Accuracy: Verify all entries for accuracy, particularly identification numbers and addresses. Consistency with legal documentation is critical.

-

Sign and Date: Ensure the form is signed by the fiduciary or authorized representative and dated appropriately.

Obtaining Editable Form 56 2011

To obtain the editable version of Form 56 for the year 2011, you can access it through several methods:

- IRS Website: The official IRS website provides access to downloadable forms, including older versions for specific years.

- Document Management Platforms: Services like DocHub offer editable and fillable versions, making it easy to complete the form online with additional features like digital signatures.

Legal Use of Editable Form 56 2011

Using Form 56 ensures legal clarity regarding fiduciary roles concerning tax matters. Key legal aspects include:

-

Notification of Fiduciary Relationship: The form serves as an official notice to the IRS, ensuring they are aware of the fiduciary's legal authority.

-

Tax Liability Clarification: It clarifies who is responsible for handling and resolving the taxpayer's financial obligations to the IRS.

-

Compliance with IRS Regulations: Utilizing this form as required by the IRS helps avoid potential legal and financial penalties associated with non-compliance.

Key Elements of Editable Form 56 2011

The form comprises several critical elements:

-

Identification Information: This includes the taxpayer’s name and Social Security Number.

-

Fiduciary Details: Information about the fiduciary, including their name, address, and relationship to the taxpayer.

-

Type of Tax Matters: A detailed description of the tax issues or liabilities managed by the fiduciary.

-

Relevant Proceedings: Any court or administrative proceedings related to the fiduciary duties should be noted.

Who Typically Uses Editable Form 56 2011

The primary users of Form 56 2011 are fiduciaries managing tax affairs for:

-

Estates and Trusts: Executors of estates or trustees dealing with tax obligations on behalf of a deceased individual or trust.

-

Legal Representatives: Lawyers or other legal representatives appointed to handle specific fiduciary duties.

-

Corporations and Partnerships: Sometimes used by business entities where a fiduciary relationship needs formal acknowledgment.

IRS Guidelines for Editable Form 56 2011

Following IRS guidelines when dealing with Form 56 is crucial:

-

Submission Timing: The form should be submitted as soon as the fiduciary relationship is established to prevent delays in processing tax matters.

-

Document Retention: Maintain copies of submitted forms and any supporting documentation in case of future inquiries or audits by the IRS.

Penalties for Non-Compliance with Editable Form 56 2011

Failure to submit Form 56 as required can result in legal and financial consequences:

-

Delayed Tax Processing: Non-submission can lead to delays in processing tax returns or refunds related to the fiduciary’s activities.

-

Potential Legal Action: Missing or incorrect submissions might lead the IRS to take legal action against the fiduciary for unresolved tax matters or misrepresenting authority.

Each of these sections is designed to ensure comprehensive coverage and in-depth understanding of Editable Form 56 2011, ensuring readers can navigate its complexities effectively.